Advertisement

Renaissance Global's (NSE:RGL) Profits May Not Reveal Underlying Issues

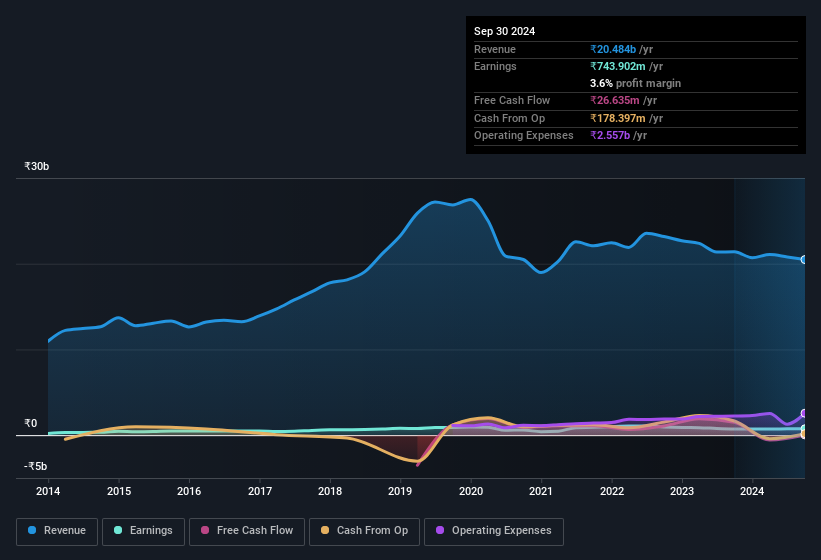

The stock price didn't jump after Renaissance Global Limited (NSE:RGL) posted decent earnings last week. We did some digging and believe investors may be worried about some underlying factors in the report.

View our latest analysis for Renaissance Global

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, Renaissance Global increased the number of shares on issue by 12% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Renaissance Global's EPS by clicking here.

A Look At The Impact Of Renaissance Global's Dilution On Its Earnings Per Share (EPS)

Unfortunately, Renaissance Global's profit is down 19% per year over three years. The good news is that profit was up 2.5% in the last twelve months. But EPS was less impressive, and was pretty much flat over that time. And so, you can see quite clearly that dilution is influencing shareholder earnings.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So Renaissance Global shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Renaissance Global.

Our Take On Renaissance Global's Profit Performance

Each Renaissance Global share now gets a meaningfully smaller slice of its overall profit, due to dilution of existing shareholders. Therefore, it seems possible to us that Renaissance Global's true underlying earnings power is actually less than its statutory profit. The good news is that its earnings per share increased slightly in the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. To help with this, we've discovered 3 warning signs (1 shouldn't be ignored!) that you ought to be aware of before buying any shares in Renaissance Global.

Today we've zoomed in on a single data point to better understand the nature of Renaissance Global's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RGL

Renaissance Global

Manufactures, retails, and trades in jewelry, gems, and diamonds in India and internationally.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor