Advertisement

We Think Shareholders May Want To Consider A Review Of Relaxo Footwears Limited's (NSE:RELAXO) CEO Compensation Package

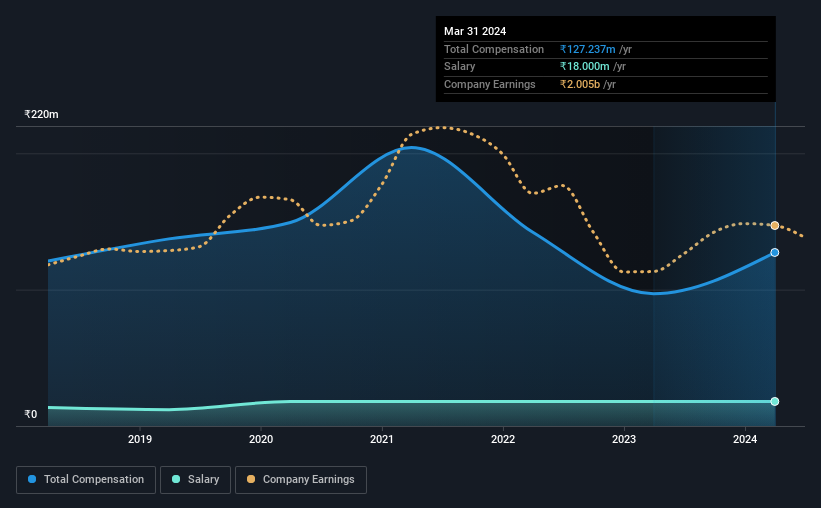

Key Insights

- Relaxo Footwears' Annual General Meeting to take place on 29th of August

- Salary of ₹18.0m is part of CEO Ramesh Dua's total remuneration

- The total compensation is 179% higher than the average for the industry

- Relaxo Footwears' three-year loss to shareholders was 29% while its EPS was down 14% over the past three years

Relaxo Footwears Limited (NSE:RELAXO) has not performed well recently and CEO Ramesh Dua will probably need to up their game. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 29th of August. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. We present the case why we think CEO compensation is out of sync with company performance.

Check out our latest analysis for Relaxo Footwears

Comparing Relaxo Footwears Limited's CEO Compensation With The Industry

According to our data, Relaxo Footwears Limited has a market capitalization of ₹204b, and paid its CEO total annual compensation worth ₹127m over the year to March 2024. Notably, that's an increase of 31% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at ₹18m.

On comparing similar companies from the Indian Luxury industry with market caps ranging from ₹168b to ₹537b, we found that the median CEO total compensation was ₹46m. Hence, we can conclude that Ramesh Dua is remunerated higher than the industry median. Furthermore, Ramesh Dua directly owns ₹57b worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | ₹18m | ₹18m | 14% |

| Other | ₹109m | ₹79m | 86% |

| Total Compensation | ₹127m | ₹97m | 100% |

Speaking on an industry level, nearly 99% of total compensation represents salary, while the remainder of 0.92341277% is other remuneration. In Relaxo Footwears' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Relaxo Footwears Limited's Growth

Over the last three years, Relaxo Footwears Limited has shrunk its earnings per share by 14% per year. Its revenue is up 2.4% over the last year.

The decline in EPS is a bit concerning. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Relaxo Footwears Limited Been A Good Investment?

With a three year total loss of 29% for the shareholders, Relaxo Footwears Limited would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 1 warning sign for Relaxo Footwears that you should be aware of before investing.

Switching gears from Relaxo Footwears, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RELAXO

Relaxo Footwears

Engages in the manufacture and sale of footwear for men, women, and kids in India and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.7% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor