- India

- /

- Real Estate

- /

- NSEI:RAYMOND

There Are Reasons To Feel Uneasy About Raymond's (NSE:RAYMOND) Returns On Capital

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Although, when we looked at Raymond (NSE:RAYMOND), it didn't seem to tick all of these boxes.

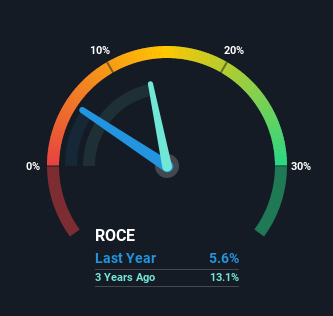

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Raymond:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.056 = ₹2.0b ÷ (₹68b - ₹32b) (Based on the trailing twelve months to September 2021).

So, Raymond has an ROCE of 5.6%. Ultimately, that's a low return and it under-performs the Luxury industry average of 13%.

See our latest analysis for Raymond

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Raymond's past further, check out this free graph of past earnings, revenue and cash flow.

The Trend Of ROCE

We weren't thrilled with the trend because Raymond's ROCE has reduced by 50% over the last five years, while the business employed 44% more capital. Usually this isn't ideal, but given Raymond conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. The funds raised likely haven't been put to work yet so it's worth watching what happens in the future with Raymond's earnings and if they change as a result from the capital raise.

Another thing to note, Raymond has a high ratio of current liabilities to total assets of 47%. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

What We Can Learn From Raymond's ROCE

In summary, despite lower returns in the short term, we're encouraged to see that Raymond is reinvesting for growth and has higher sales as a result. These trends are starting to be recognized by investors since the stock has delivered a 25% gain to shareholders who've held over the last five years. So this stock may still be an appealing investment opportunity, if other fundamentals prove to be sound.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for Raymond (of which 2 are concerning!) that you should know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you're looking to trade Raymond, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RAYMOND

Flawless balance sheet, undervalued and pays a dividend.