Advertisement

Kewal Kiran Clothing Limited's (NSE:KKCL) On An Uptrend But Financial Prospects Look Pretty Weak: Is The Stock Overpriced?

Most readers would already be aware that Kewal Kiran Clothing's (NSE:KKCL) stock increased significantly by 23% over the past three months. However, we decided to pay close attention to its weak financials as we are doubtful that the current momentum will keep up, given the scenario. Specifically, we decided to study Kewal Kiran Clothing's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

See our latest analysis for Kewal Kiran Clothing

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Kewal Kiran Clothing is:

6.3% = ₹276m ÷ ₹4.4b (Based on the trailing twelve months to September 2020).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every ₹1 worth of equity, the company was able to earn ₹0.06 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

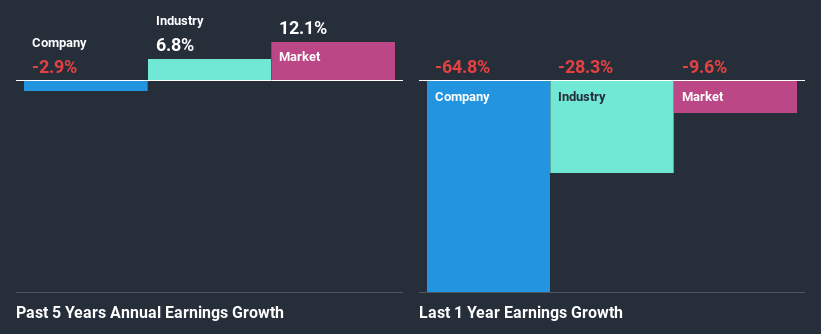

A Side By Side comparison of Kewal Kiran Clothing's Earnings Growth And 6.3% ROE

As you can see, Kewal Kiran Clothing's ROE looks pretty weak. An industry comparison shows that the company's ROE is not much different from the industry average of 5.5% either. Given the circumstances, the significant decline in net income by 2.9% seen by Kewal Kiran Clothing over the last five years is not surprising.

However, when we compared Kewal Kiran Clothing's growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 6.8% in the same period. This is quite worrisome.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Kewal Kiran Clothing is trading on a high P/E or a low P/E, relative to its industry.

Is Kewal Kiran Clothing Using Its Retained Earnings Effectively?

Kewal Kiran Clothing has a high three-year median payout ratio of 71% (that is, it is retaining 29% of its profits). This suggests that the company is paying most of its profits as dividends to its shareholders. This goes some way in explaining why its earnings have been shrinking. The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run. Our risks dashboard should have the 3 risks we have identified for Kewal Kiran Clothing.

Additionally, Kewal Kiran Clothing has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 62%. However, Kewal Kiran Clothing's ROE is predicted to rise to 15% despite there being no anticipated change in its payout ratio.

Conclusion

In total, we would have a hard think before deciding on any investment action concerning Kewal Kiran Clothing. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

When trading Kewal Kiran Clothing or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kewal Kiran Clothing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:KKCL

Kewal Kiran Clothing

Kewal Kiran Clothing Limited manufacturing, marketing, and retailing of branded readymade garments and finished accessories in India and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor