Here's Why Kanani Industries (NSE:KANANIIND) Can Manage Its Debt Responsibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Kanani Industries Limited (NSE:KANANIIND) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Kanani Industries

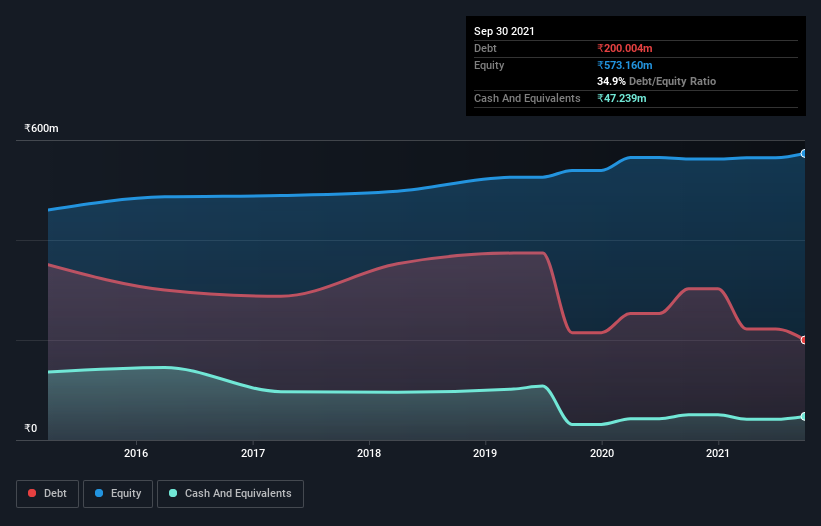

What Is Kanani Industries's Debt?

You can click the graphic below for the historical numbers, but it shows that Kanani Industries had ₹200.0m of debt in September 2021, down from ₹302.6m, one year before. On the flip side, it has ₹47.2m in cash leading to net debt of about ₹152.8m.

A Look At Kanani Industries' Liabilities

According to the balance sheet data, Kanani Industries had liabilities of ₹757.5m due within 12 months, but no longer term liabilities. Offsetting this, it had ₹47.2m in cash and ₹1.13b in receivables that were due within 12 months. So it actually has ₹420.3m more liquid assets than total liabilities.

This surplus suggests that Kanani Industries is using debt in a way that is appears to be both safe and conservative. Because it has plenty of assets, it is unlikely to have trouble with its lenders.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Kanani Industries shareholders face the double whammy of a high net debt to EBITDA ratio (16.2), and fairly weak interest coverage, since EBIT is just 0.98 times the interest expense. The debt burden here is substantial. Even worse, Kanani Industries saw its EBIT tank 48% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Kanani Industries will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Kanani Industries actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

We weren't impressed with Kanani Industries's interest cover, and its EBIT growth rate made us cautious. But like a ballerina ending on a perfect pirouette, it has not trouble converting EBIT to free cash flow. Looking at all this data makes us feel a little cautious about Kanani Industries's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example - Kanani Industries has 3 warning signs we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Kanani Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KANANIIND

Kanani Industries

Engages in the manufacture and export of diamond studded jewellery in India.

Flawless balance sheet and good value.