Advertisement

- India

- /

- Professional Services

- /

- NSEI:CAMS

Computer Age Management Services' (NSE:CAMS) Dividend Will Be Increased To ₹19.00

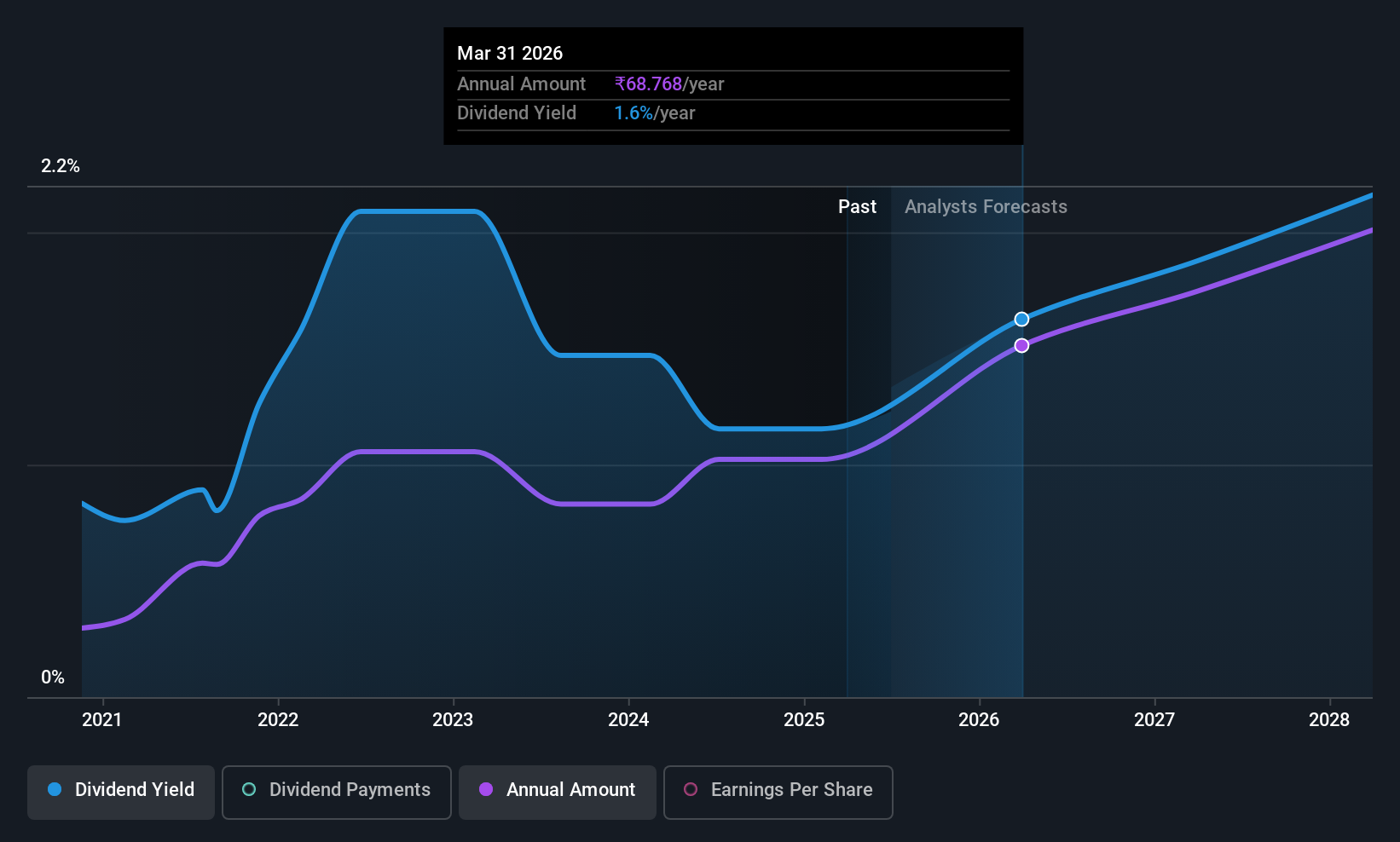

Computer Age Management Services Limited (NSE:CAMS) has announced that it will be increasing its dividend from last year's comparable payment on the 6th of August to ₹19.00. This makes the dividend yield 1.5%, which is above the industry average.

Computer Age Management Services' Future Dividend Projections Appear Well Covered By Earnings

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. The last dividend was quite comfortably covered by Computer Age Management Services' earnings, but it was a bit tighter on the cash flow front. The business is earning enough to make the dividend feasible, but the cash payout ratio of 85% indicates it is more focused on returning cash to shareholders than growing the business.

Over the next year, EPS is forecast to expand by 38.8%. Assuming the dividend continues along recent trends, we think the payout ratio could be 66% by next year, which is in a pretty sustainable range.

See our latest analysis for Computer Age Management Services

Computer Age Management Services' Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2020, the dividend has gone from ₹13.50 total annually to ₹62.00. This implies that the company grew its distributions at a yearly rate of about 36% over that duration. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Computer Age Management Services has impressed us by growing EPS at 22% per year over the past five years. The company's earnings per share has grown rapidly in recent years, and it has a good balance between reinvesting and paying dividends to shareholders, so we think that Computer Age Management Services could prove to be a strong dividend payer.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Computer Age Management Services will make a great income stock. The low payout ratio is a redeeming feature, but generally we are not too happy with the payments Computer Age Management Services has been making. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, Computer Age Management Services has 2 warning signs (and 1 which is a bit unpleasant) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CAMS

Computer Age Management Services

Provides registrar and transfer agency services, including data processing and its related activities to financial institutions in India.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor