Advertisement

Should Income Investors Look At Wendt (India) Limited (NSE:WENDT) Before Its Ex-Dividend?

Wendt (India) Limited (NSE:WENDT) is about to trade ex-dividend in the next three days. If you purchase the stock on or after the 3rd of February, you won't be eligible to receive this dividend, when it is paid on the 18th of February.

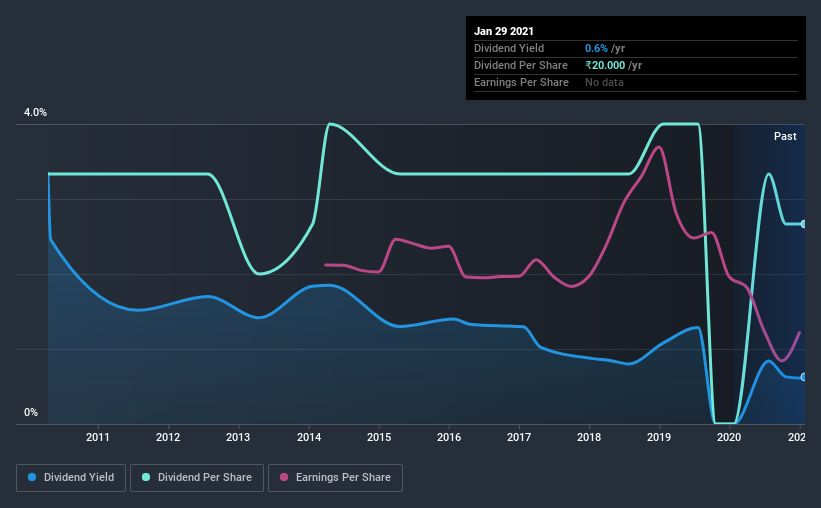

Wendt (India)'s upcoming dividend is ₹10.00 a share, following on from the last 12 months, when the company distributed a total of ₹20.00 per share to shareholders. Looking at the last 12 months of distributions, Wendt (India) has a trailing yield of approximately 0.6% on its current stock price of ₹3161.2. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

View our latest analysis for Wendt (India)

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Wendt (India) is paying out an acceptable 75% of its profit, a common payout level among most companies. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It distributed 28% of its free cash flow as dividends, a comfortable payout level for most companies.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see how much of its profit Wendt (India) paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Wendt (India)'s earnings per share have fallen at approximately 13% a year over the previous five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Wendt (India)'s dividend payments per share have declined at 2.2% per year on average over the past 10 years, which is uninspiring. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

Final Takeaway

Is Wendt (India) an attractive dividend stock, or better left on the shelf? We're not enthused by the declining earnings per share, although at least the company's payout ratio is within a reasonable range, meaning it may not be at imminent risk of a dividend cut. To summarise, Wendt (India) looks okay on this analysis, although it doesn't appear a stand-out opportunity.

With that being said, if dividends aren't your biggest concern with Wendt (India), you should know about the other risks facing this business. We've identified 4 warning signs with Wendt (India) (at least 1 which shouldn't be ignored), and understanding these should be part of your investment process.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

When trading Wendt (India) or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wendt (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:WENDT

Wendt (India)

Manufactures, sells, and services super abrasives, high precision grinding, honing, special purpose machines, and precision components in India and internationally.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.2% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor