Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Sadbhav Engineering Limited (NSE:SADBHAV) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Sadbhav Engineering

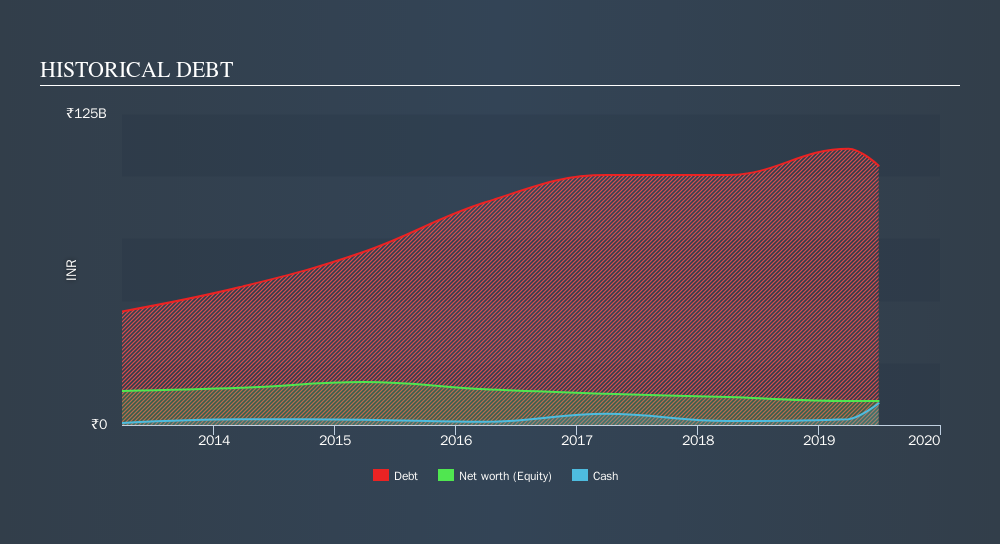

How Much Debt Does Sadbhav Engineering Carry?

As you can see below, Sadbhav Engineering had ₹104.2b of debt, at March 2019, which is about the same the year before. You can click the chart for greater detail. However, because it has a cash reserve of ₹8.74b, its net debt is less, at about ₹95.5b.

How Strong Is Sadbhav Engineering's Balance Sheet?

According to the last reported balance sheet, Sadbhav Engineering had liabilities of ₹34.4b due within 12 months, and liabilities of ₹116.9b due beyond 12 months. Offsetting these obligations, it had cash of ₹8.74b as well as receivables valued at ₹22.0b due within 12 months. So it has liabilities totalling ₹120.5b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the ₹22.5b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Sadbhav Engineering would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 0.75 times and a disturbingly high net debt to EBITDA ratio of 6.8 hit our confidence in Sadbhav Engineering like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. More concerning, Sadbhav Engineering saw its EBIT drop by 6.7% in the last twelve months. If it keeps going like that paying off its debt will be like running on a treadmill -- a lot of effort for not much advancement. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Sadbhav Engineering can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Sadbhav Engineering's free cash flow amounted to 41% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

To be frank both Sadbhav Engineering's interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. Having said that, its ability to convert EBIT to free cash flow isn't such a worry. Taking into account all the aforementioned factors, it looks like Sadbhav Engineering has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. Given the risks around Sadbhav Engineering's use of debt, the sensible thing to do is to check if insiders have been unloading the stock.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:SADBHAV

Sadbhav Engineering

Engages in engineering, construction, and infrastructure development projects business in India.

Good value low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor