Advertisement

- India

- /

- Trade Distributors

- /

- NSEI:PRITIKAUTO

Earnings Tell The Story For Pritika Auto Industries Limited (NSE:PRITIKAUTO) As Its Stock Soars 26%

Despite an already strong run, Pritika Auto Industries Limited (NSE:PRITIKAUTO) shares have been powering on, with a gain of 26% in the last thirty days. The annual gain comes to 142% following the latest surge, making investors sit up and take notice.

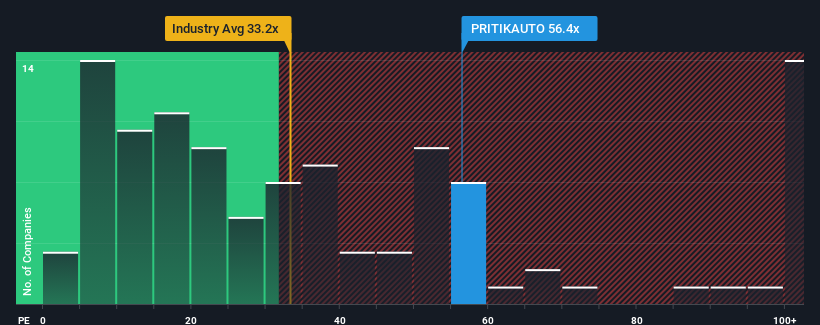

Following the firm bounce in price, Pritika Auto Industries may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 56.4x, since almost half of all companies in India have P/E ratios under 31x and even P/E's lower than 17x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

As an illustration, earnings have deteriorated at Pritika Auto Industries over the last year, which is not ideal at all. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

See our latest analysis for Pritika Auto Industries

How Is Pritika Auto Industries' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Pritika Auto Industries' is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 15% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 353% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 25% shows it's noticeably more attractive on an annualised basis.

With this information, we can see why Pritika Auto Industries is trading at such a high P/E compared to the market. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Final Word

The strong share price surge has got Pritika Auto Industries' P/E rushing to great heights as well. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Pritika Auto Industries revealed its three-year earnings trends are contributing to its high P/E, given they look better than current market expectations. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 5 warning signs with Pritika Auto Industries (at least 2 which are a bit concerning), and understanding them should be part of your investment process.

You might be able to find a better investment than Pritika Auto Industries. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PRITIKAUTO

Pritika Auto Industries

Manufactures and sells tractor and automobile components in India.

Solid track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor