Advertisement

- India

- /

- Construction

- /

- NSEI:NBCC

NBCC (India) Limited (NSE:NBCC) Stocks Pounded By 26% But Not Lagging Market On Growth Or Pricing

NBCC (India) Limited (NSE:NBCC) shareholders that were waiting for something to happen have been dealt a blow with a 26% share price drop in the last month. The good news is that in the last year, the stock has shone bright like a diamond, gaining 105%.

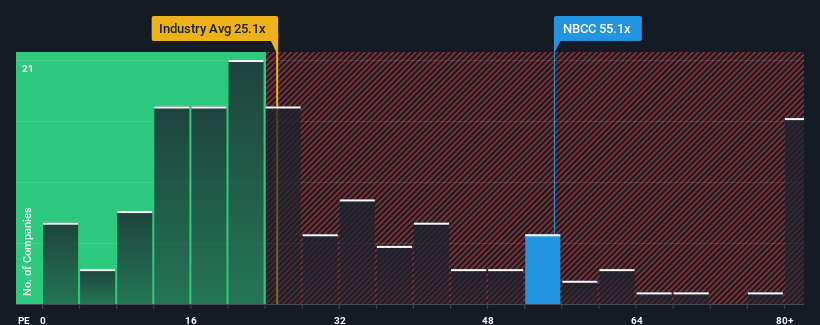

In spite of the heavy fall in price, NBCC (India)'s price-to-earnings (or "P/E") ratio of 55.1x might still make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 31x and even P/E's below 18x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

With earnings growth that's inferior to most other companies of late, NBCC (India) has been relatively sluggish. It might be that many expect the uninspiring earnings performance to recover significantly, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

See our latest analysis for NBCC (India)

How Is NBCC (India)'s Growth Trending?

There's an inherent assumption that a company should far outperform the market for P/E ratios like NBCC (India)'s to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 18% last year. The strong recent performance means it was also able to grow EPS by 67% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 34% over the next year. That's shaping up to be materially higher than the 26% growth forecast for the broader market.

In light of this, it's understandable that NBCC (India)'s P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On NBCC (India)'s P/E

Even after such a strong price drop, NBCC (India)'s P/E still exceeds the rest of the market significantly. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of NBCC (India)'s analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

Having said that, be aware NBCC (India) is showing 2 warning signs in our investment analysis, you should know about.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if NBCC (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NBCC

NBCC (India)

Engages in project management consultancy, engineering procurement and construction, and real estate development businesses in India and internationally.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor