Advertisement

Returns On Capital At Kriti Industries (India) (NSE:KRITI) Paint A Concerning Picture

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. However, after investigating Kriti Industries (India) (NSE:KRITI), we don't think it's current trends fit the mold of a multi-bagger.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Kriti Industries (India) is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.037 = ₹61m ÷ (₹4.1b - ₹2.5b) (Based on the trailing twelve months to June 2023).

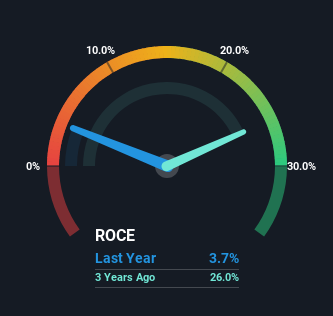

Thus, Kriti Industries (India) has an ROCE of 3.7%. In absolute terms, that's a low return and it also under-performs the Building industry average of 16%.

See our latest analysis for Kriti Industries (India)

Historical performance is a great place to start when researching a stock so above you can see the gauge for Kriti Industries (India)'s ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Kriti Industries (India), check out these free graphs here.

What Does the ROCE Trend For Kriti Industries (India) Tell Us?

On the surface, the trend of ROCE at Kriti Industries (India) doesn't inspire confidence. Around five years ago the returns on capital were 25%, but since then they've fallen to 3.7%. Although, given both revenue and the amount of assets employed in the business have increased, it could suggest the company is investing in growth, and the extra capital has led to a short-term reduction in ROCE. And if the increased capital generates additional returns, the business, and thus shareholders, will benefit in the long run.

On a side note, Kriti Industries (India)'s current liabilities are still rather high at 60% of total assets. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

In Conclusion...

Even though returns on capital have fallen in the short term, we find it promising that revenue and capital employed have both increased for Kriti Industries (India). Furthermore the stock has climbed 31% over the last year, it would appear that investors are upbeat about the future. So should these growth trends continue, we'd be optimistic on the stock going forward.

One more thing: We've identified 3 warning signs with Kriti Industries (India) (at least 2 which are significant) , and understanding them would certainly be useful.

While Kriti Industries (India) may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Kriti Industries (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KRITI

Kriti Industries (India)

Manufactures and sells plastic products and pipes in India and internationally.

Excellent balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor