Advertisement

Top Growth Companies With High Insider Ownership On The Indian Exchange

Simply Wall St

Reviewed by Simply Wall St

In the last week, the Indian market has been flat, but it is up 44% over the past year with earnings forecast to grow by 17% annually. In this thriving environment, growth companies with high insider ownership can be particularly attractive as they often indicate strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In India

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34.2% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| Jupiter Wagons (NSEI:JWL) | 10.8% | 27.4% |

| Dixon Technologies (India) (NSEI:DIXON) | 24.6% | 31.6% |

| Happiest Minds Technologies (NSEI:HAPPSTMNDS) | 32.5% | 22.2% |

| Paisalo Digital (BSE:532900) | 16.3% | 24.8% |

| Rajratan Global Wire (BSE:517522) | 19.8% | 35.8% |

| Pricol (NSEI:PRICOLLTD) | 25.5% | 24% |

| KEI Industries (BSE:517569) | 18.7% | 22.4% |

| Aether Industries (NSEI:AETHER) | 31.1% | 45.9% |

Here's a peek at a few of the choices from the screener.

Heritage Foods (NSEI:HERITGFOOD)

Simply Wall St Growth Rating: ★★★★☆☆

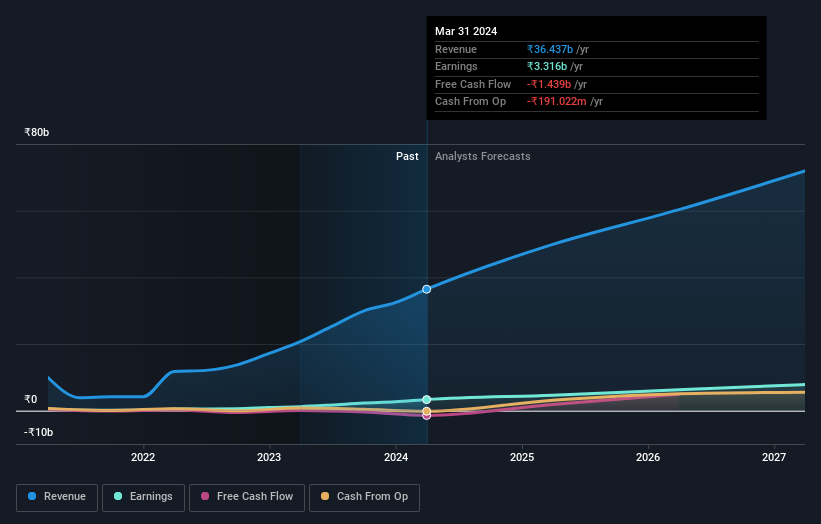

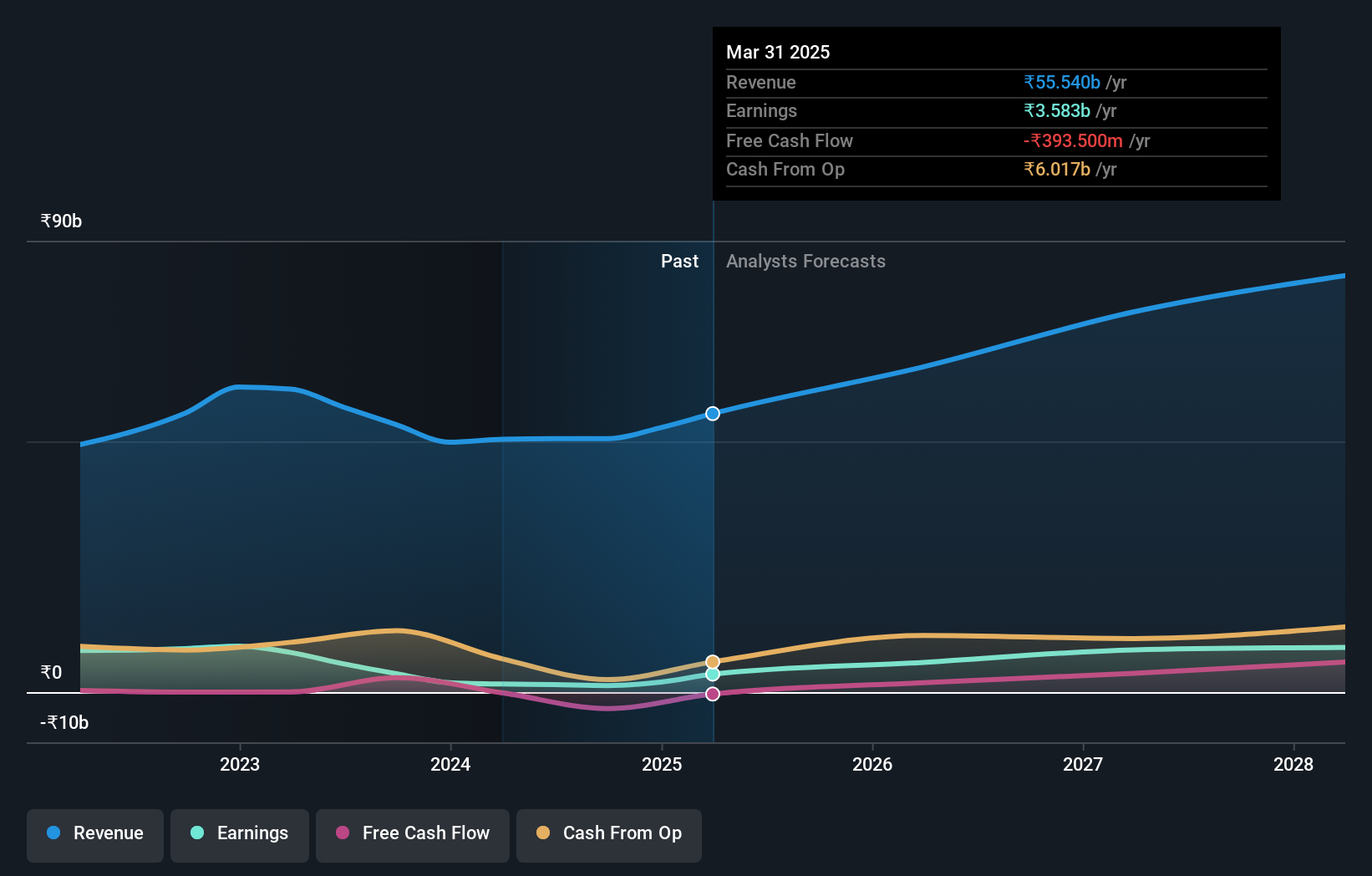

Overview: Heritage Foods Limited, with a market cap of ₹59.69 billion, procures and processes milk and milk products in India.

Operations: Heritage Foods Limited generates revenue primarily from its Dairy segment with ₹38.40 billion, followed by the Feed segment at ₹1.70 billion, and Renewable Energy contributing ₹90.04 million.

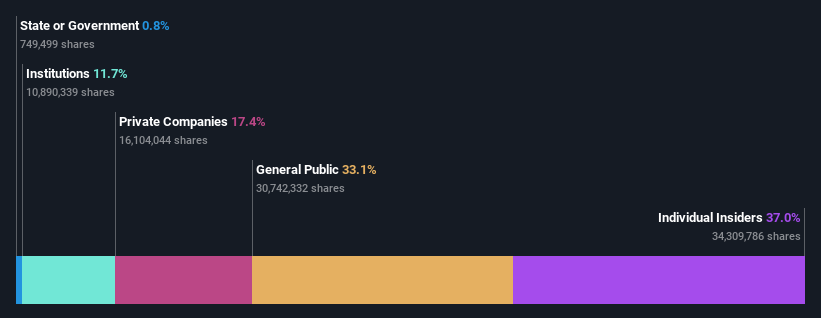

Insider Ownership: 37%

Revenue Growth Forecast: 11.3% p.a.

Heritage Foods has demonstrated significant profit growth, with earnings increasing by 119.8% over the past year. The company’s revenue and earnings are forecast to grow at 11.3% and 17.57% per year respectively, outpacing the Indian market averages. Recent strategic moves include a new ice cream manufacturing facility in Telangana with an investment of INR 2,040 million, reflecting strong insider confidence and commitment to expansion despite an unstable dividend track record.

- Unlock comprehensive insights into our analysis of Heritage Foods stock in this growth report.

- Our expertly prepared valuation report Heritage Foods implies its share price may be too high.

Jupiter Wagons (NSEI:JWL)

Simply Wall St Growth Rating: ★★★★★★

Overview: Jupiter Wagons Limited manufactures and sells railway wagons, wagon components, and railway transportation equipment in India and internationally, with a market cap of ₹218.34 billion.

Operations: The company's revenue segments include ₹37.70 billion from auto manufacturers.

Insider Ownership: 10.8%

Revenue Growth Forecast: 23.2% p.a.

Jupiter Wagons has shown robust earnings growth of 111.2% over the past year, with revenue and earnings forecast to grow at 23.2% and 27.4% per year respectively, outpacing the Indian market averages. Despite recent shareholder dilution from an INR 8 billion equity offering, insider ownership remains high. The company declared both interim and final dividends recently but these are not well covered by free cash flows, indicating potential sustainability concerns.

- Take a closer look at Jupiter Wagons' potential here in our earnings growth report.

- The analysis detailed in our Jupiter Wagons valuation report hints at an inflated share price compared to its estimated value.

Laurus Labs (NSEI:LAURUSLABS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Laurus Labs Limited, with a market cap of ₹253.03 billion, manufactures and sells medicines and active pharmaceutical ingredients (APIs) in India and internationally.

Operations: The company's revenue is primarily derived from the manufacture of active pharmaceutical ingredients, intermediates, and formulations, amounting to ₹50.54 billion.

Insider Ownership: 27.8%

Revenue Growth Forecast: 13.9% p.a.

Laurus Labs has demonstrated strong growth potential with earnings expected to grow significantly at 50.8% per year, outpacing the Indian market average. The company recently inaugurated a new R&D center with an investment of INR 2.50 billion, enhancing its innovation capabilities and supporting its CDMO business. However, profit margins have declined from last year and interest payments are not well covered by earnings, indicating some financial challenges despite high insider ownership.

- Delve into the full analysis future growth report here for a deeper understanding of Laurus Labs.

- Our valuation report unveils the possibility Laurus Labs' shares may be trading at a premium.

Next Steps

- Access the full spectrum of 93 Fast Growing Indian Companies With High Insider Ownership by clicking on this link.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Heritage Foods might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:HERITGFOOD

Heritage Foods

Heritage Foods Limited procures and processes milk and milk products in India.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor