The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Inox Wind Energy Limited (NSE:IWEL) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Inox Wind Energy

How Much Debt Does Inox Wind Energy Carry?

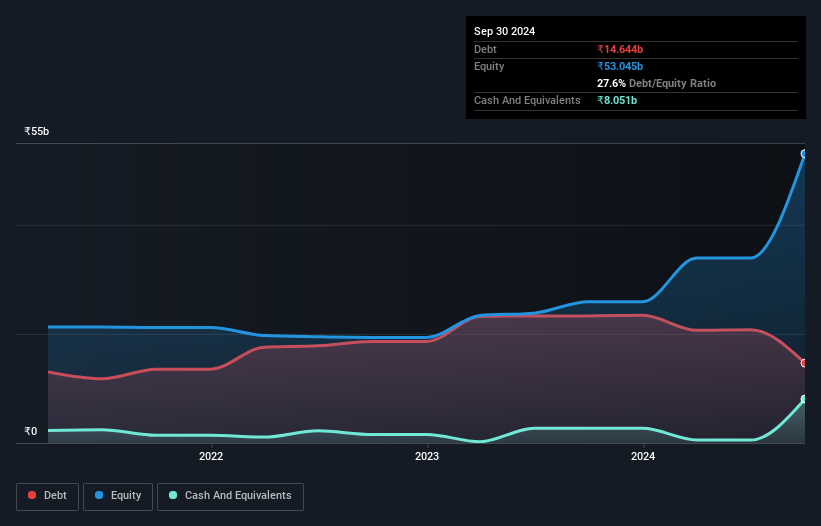

As you can see below, Inox Wind Energy had ₹14.6b of debt at September 2024, down from ₹23.3b a year prior. However, because it has a cash reserve of ₹8.05b, its net debt is less, at about ₹6.59b.

How Strong Is Inox Wind Energy's Balance Sheet?

We can see from the most recent balance sheet that Inox Wind Energy had liabilities of ₹30.3b falling due within a year, and liabilities of ₹1.19b due beyond that. On the other hand, it had cash of ₹8.05b and ₹14.9b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹8.52b.

Since publicly traded Inox Wind Energy shares are worth a total of ₹131.6b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Inox Wind Energy's low debt to EBITDA ratio of 1.3 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 2.7 times last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. We also note that Inox Wind Energy improved its EBIT from a last year's loss to a positive ₹3.8b. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Inox Wind Energy will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. During the last year, Inox Wind Energy burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Inox Wind Energy's conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to handle its debt, based on its EBITDA, isn't too shabby at all. When we consider all the factors discussed, it seems to us that Inox Wind Energy is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. Over time, share prices tend to follow earnings per share, so if you're interested in Inox Wind Energy, you may well want to click here to check an interactive graph of its earnings per share history.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:IWEL

Inox Wind Energy

Engages in the manufacture and sale of wind turbine generators (WTGs) in India.

Adequate balance sheet with acceptable track record.

Market Insights

Community Narratives