Advertisement

- India

- /

- Construction

- /

- NSEI:INOXGREEN

We Think That There Are Some Issues For Inox Green Energy Services (NSE:INOXGREEN) Beyond Its Promising Earnings

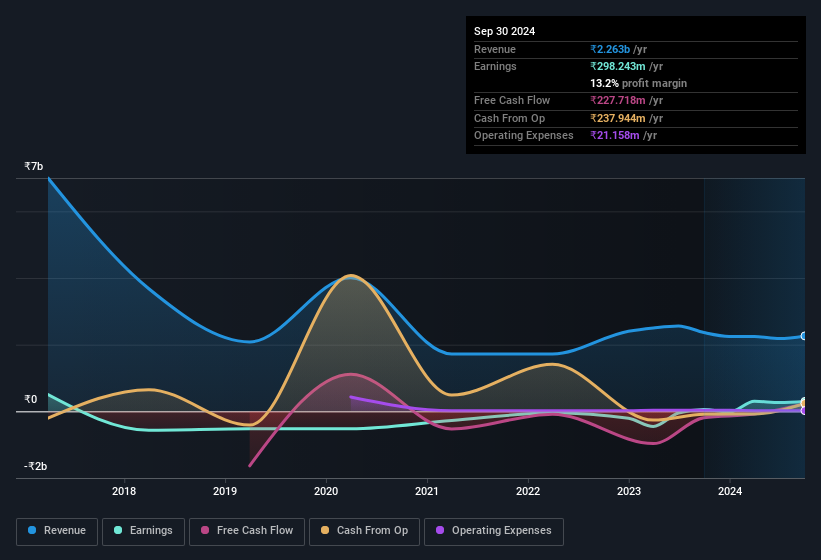

Inox Green Energy Services Limited's (NSE:INOXGREEN) healthy profit numbers didn't contain any surprises for investors. We believe that shareholders have noticed some concerning factors beyond the statutory profit numbers.

View our latest analysis for Inox Green Energy Services

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, Inox Green Energy Services increased the number of shares on issue by 25% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Inox Green Energy Services' historical EPS growth by clicking on this link.

How Is Dilution Impacting Inox Green Energy Services' Earnings Per Share (EPS)?

Three years ago, Inox Green Energy Services lost money. On the bright side, in the last twelve months it grew profit by 440%. But EPS was less impressive, up only 371% in that time. Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So Inox Green Energy Services shareholders will want to see that EPS figure continue to increase. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Inox Green Energy Services.

The Impact Of Unusual Items On Profit

Alongside that dilution, it's also important to note that Inox Green Energy Services' profit was boosted by unusual items worth ₹35m in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. If Inox Green Energy Services doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Inox Green Energy Services' Profit Performance

In its last report Inox Green Energy Services benefitted from unusual items which boosted its profit, which could make the profit seem better than it really is on a sustainable basis. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. Considering all this we'd argue Inox Green Energy Services' profits probably give an overly generous impression of its sustainable level of profitability. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. You'd be interested to know, that we found 2 warning signs for Inox Green Energy Services and you'll want to know about these bad boys.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INOXGREEN

Inox Green Energy Services

Provides operation and maintenance services, and common infrastructure facilities for wind turbine generators in India.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor