Advertisement

- India

- /

- Electrical

- /

- NSEI:HPL

What You Can Learn From HPL Electric & Power Limited's (NSE:HPL) P/E After Its 29% Share Price Crash

HPL Electric & Power Limited (NSE:HPL) shareholders that were waiting for something to happen have been dealt a blow with a 29% share price drop in the last month. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

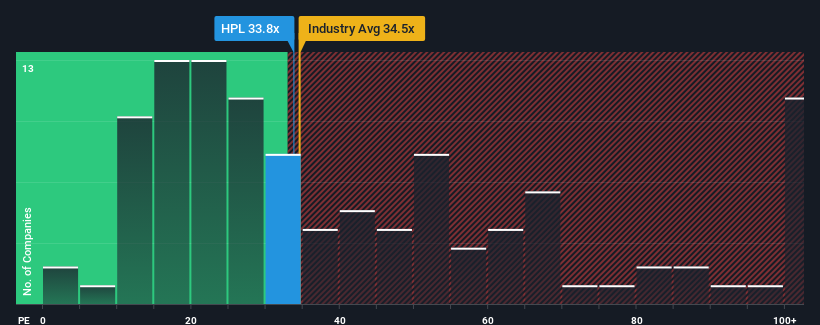

Even after such a large drop in price, HPL Electric & Power's price-to-earnings (or "P/E") ratio of 33.8x might still make it look like a sell right now compared to the market in India, where around half of the companies have P/E ratios below 26x and even P/E's below 15x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for HPL Electric & Power as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for HPL Electric & Power

How Is HPL Electric & Power's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as HPL Electric & Power's is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 71% gain to the company's bottom line. The latest three year period has also seen an excellent 746% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the lone analyst covering the company suggest earnings should grow by 45% over the next year. Meanwhile, the rest of the market is forecast to only expand by 26%, which is noticeably less attractive.

With this information, we can see why HPL Electric & Power is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

There's still some solid strength behind HPL Electric & Power's P/E, if not its share price lately. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that HPL Electric & Power maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with HPL Electric & Power (at least 1 which is potentially serious), and understanding these should be part of your investment process.

If you're unsure about the strength of HPL Electric & Power's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if HPL Electric & Power might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HPL

HPL Electric & Power

Manufactures and sells electric equipment under the HPL brand in India.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor