Advertisement

- India

- /

- Trade Distributors

- /

- NSEI:ESSENTIA

Integra Essentia's (NSE:ESSENTIA) Earnings Are Of Questionable Quality

Integra Essentia Limited's (NSE:ESSENTIA) stock was strong after they recently reported robust earnings. However, we think that shareholders may be missing some concerning details in the numbers.

See our latest analysis for Integra Essentia

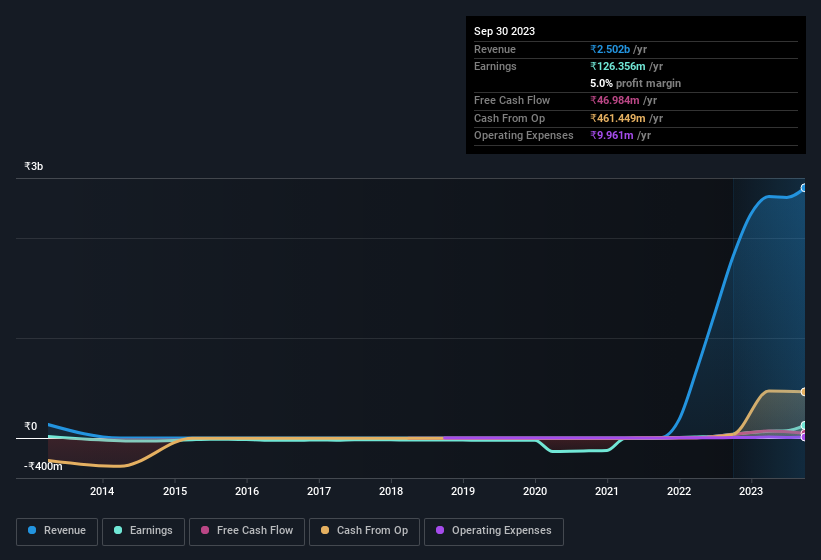

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, Integra Essentia increased the number of shares on issue by 19% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Integra Essentia's historical EPS growth by clicking on this link.

A Look At The Impact Of Integra Essentia's Dilution On Its Earnings Per Share (EPS)

Three years ago, Integra Essentia lost money. On the bright side, in the last twelve months it grew profit by 231%. On the other hand, earnings per share are only up 72% over the same period. So you can see that the dilution has had a bit of an impact on shareholders.

In the long term, earnings per share growth should beget share price growth. So Integra Essentia shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Integra Essentia.

Our Take On Integra Essentia's Profit Performance

Integra Essentia shareholders should keep in mind how many new shares it is issuing, because, dilution clearly has the power to severely impact shareholder returns. Because of this, we think that it may be that Integra Essentia's statutory profits are better than its underlying earnings power. The good news is that, its earnings per share increased by 72% in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Case in point: We've spotted 2 warning signs for Integra Essentia you should be aware of.

This note has only looked at a single factor that sheds light on the nature of Integra Essentia's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ESSENTIA

Integra Essentia

Trades in agricultural commodities, life necessities, items of basic human needs, organic and natural products, processed food, and infrastructural products in India.

Excellent balance sheet low.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor