Advertisement

Escorts Kubota (NSE:ESCORTS) Has A Pretty Healthy Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Escorts Kubota Limited (NSE:ESCORTS) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Escorts Kubota

What Is Escorts Kubota's Net Debt?

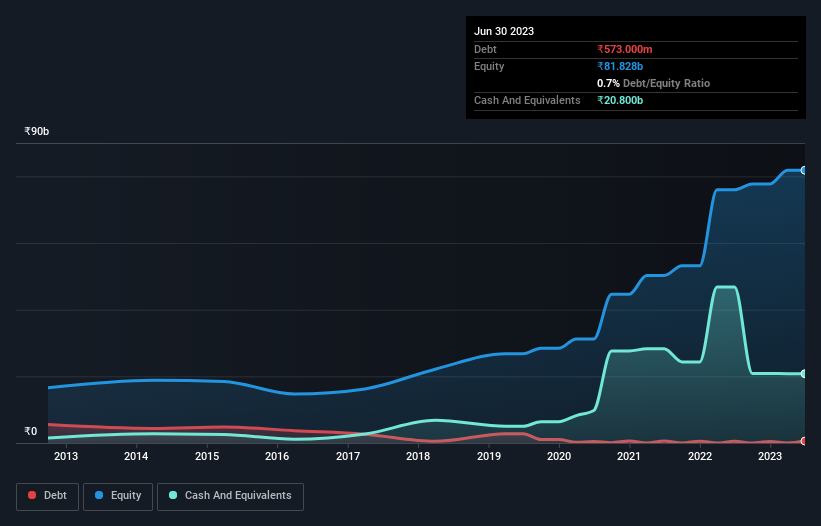

You can click the graphic below for the historical numbers, but it shows that as of March 2023 Escorts Kubota had ₹573.0m of debt, an increase on ₹519.5m, over one year. However, its balance sheet shows it holds ₹20.8b in cash, so it actually has ₹20.2b net cash.

A Look At Escorts Kubota's Liabilities

We can see from the most recent balance sheet that Escorts Kubota had liabilities of ₹17.2b falling due within a year, and liabilities of ₹1.87b due beyond that. On the other hand, it had cash of ₹20.8b and ₹11.9b worth of receivables due within a year. So it actually has ₹13.7b more liquid assets than total liabilities.

This surplus suggests that Escorts Kubota has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Escorts Kubota has more cash than debt is arguably a good indication that it can manage its debt safely.

But the other side of the story is that Escorts Kubota saw its EBIT decline by 3.1% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Escorts Kubota can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Escorts Kubota has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Escorts Kubota reported free cash flow worth 12% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing Up

While it is always sensible to investigate a company's debt, in this case Escorts Kubota has ₹20.2b in net cash and a decent-looking balance sheet. So we are not troubled with Escorts Kubota's debt use. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 1 warning sign for Escorts Kubota that you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Escorts Kubota might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ESCORTS

Escorts Kubota

Manufactures and sells agri machinery, construction equipment, and railway equipment in India and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor