Advertisement

Here's Why I Think Elgi Equipments (NSE:ELGIEQUIP) Might Deserve Your Attention Today

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But as Warren Buffett has mused, 'If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy.' When they buy such story stocks, investors are all too often the patsy.

So if you're like me, you might be more interested in profitable, growing companies, like Elgi Equipments (NSE:ELGIEQUIP). Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

Check out our latest analysis for Elgi Equipments

How Fast Is Elgi Equipments Growing?

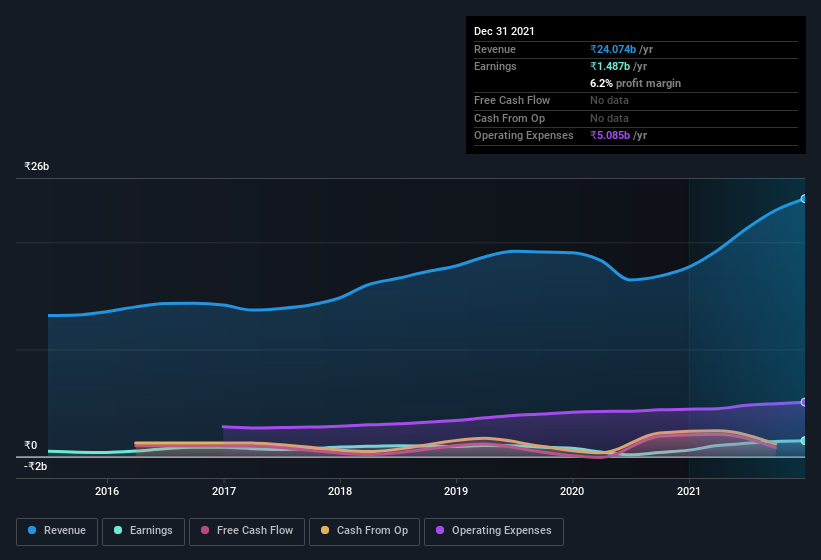

As one of my mentors once told me, share price follows earnings per share (EPS). It's no surprise, then, that I like to invest in companies with EPS growth. Over the last three years, Elgi Equipments has grown EPS by 16% per year. That growth rate is fairly good, assuming the company can keep it up.

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). The good news is that Elgi Equipments is growing revenues, and EBIT margins improved by 3.2 percentage points to 7.2%, over the last year. Ticking those two boxes is a good sign of growth, in my book.

In the chart below, you can see how the company has grown earnings, and revenue, over time. For finer detail, click on the image.

Fortunately, we've got access to analyst forecasts of Elgi Equipments's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Elgi Equipments Insiders Aligned With All Shareholders?

I like company leaders to have some skin in the game, so to speak, because it increases alignment of incentives between the people running the business, and its true owners. So it is good to see that Elgi Equipments insiders have a significant amount of capital invested in the stock. Notably, they have an enormous stake in the company, worth ₹12b. Coming in at 13% of the business, that holding gives insiders a lot of influence, and plenty of reason to generate value for shareholders. Very encouraging.

It means a lot to see insiders invested in the business, but I find myself wondering if remuneration policies are shareholder friendly. A brief analysis of the CEO compensation suggests they are. I discovered that the median total compensation for the CEOs of companies like Elgi Equipments with market caps between ₹76b and ₹243b is about ₹35m.

The Elgi Equipments CEO received total compensation of just ₹16m in the year to . That looks like modest pay to me, and may hint at a certain respect for the interests of shareholders. While the level of CEO compensation isn't a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. I'd also argue reasonable pay levels attest to good decision making more generally.

Is Elgi Equipments Worth Keeping An Eye On?

As I already mentioned, Elgi Equipments is a growing business, which is what I like to see. Earnings growth might be the main game for Elgi Equipments, but the fun does not stop there. Boasting both modest CEO pay and considerable insider ownership, I'd argue this one is worthy of the watchlist, at least. What about risks? Every company has them, and we've spotted 1 warning sign for Elgi Equipments you should know about.

You can invest in any company you want. But if you prefer to focus on stocks that have demonstrated insider buying, here is a list of companies with insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Elgi Equipments might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ELGIEQUIP

Elgi Equipments

Manufactures and sells air compressors and related parts in India, Europe, Australia, the United States, and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor