Carysil Limited (NSE:CARYSIL) Stocks Shoot Up 29% But Its P/E Still Looks Reasonable

Carysil Limited (NSE:CARYSIL) shareholders have had their patience rewarded with a 29% share price jump in the last month. The last month tops off a massive increase of 150% in the last year.

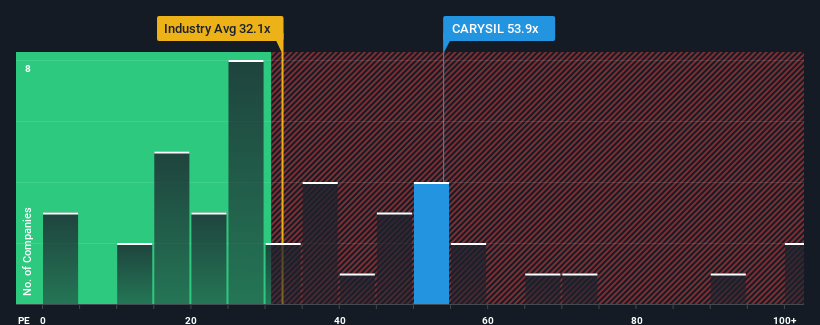

Since its price has surged higher, given close to half the companies in India have price-to-earnings ratios (or "P/E's") below 31x, you may consider Carysil as a stock to avoid entirely with its 53.9x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Carysil hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Carysil

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Carysil would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a frustrating 3.0% decrease to the company's bottom line. Even so, admirably EPS has lifted 82% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Turning to the outlook, the next year should generate growth of 65% as estimated by the four analysts watching the company. With the market only predicted to deliver 25%, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Carysil's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Carysil's P/E

Shares in Carysil have built up some good momentum lately, which has really inflated its P/E. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Carysil maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - Carysil has 2 warning signs we think you should be aware of.

If these risks are making you reconsider your opinion on Carysil, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CARYSIL

Carysil

Manufactures and trades in quartz kitchen and stainless steel kitchen sinks, bath products, tiles, kitchen appliances, and accessories in India.

Undervalued with excellent balance sheet and pays a dividend.

Market Insights

Community Narratives