Advertisement

- India

- /

- Electrical

- /

- NSEI:BBL

Bharat Bijlee Limited (NSE:BBL) Stocks Pounded By 26% But Not Lagging Market On Growth Or Pricing

The Bharat Bijlee Limited (NSE:BBL) share price has fared very poorly over the last month, falling by a substantial 26%. Of course, over the longer-term many would still wish they owned shares as the stock's price has soared 101% in the last twelve months.

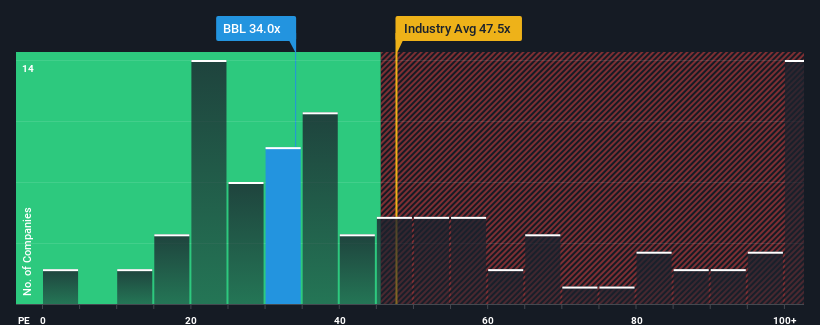

Even after such a large drop in price, it's still not a stretch to say that Bharat Bijlee's price-to-earnings (or "P/E") ratio of 34x right now seems quite "middle-of-the-road" compared to the market in India, where the median P/E ratio is around 32x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

The earnings growth achieved at Bharat Bijlee over the last year would be more than acceptable for most companies. One possibility is that the P/E is moderate because investors think this respectable earnings growth might not be enough to outperform the broader market in the near future. If that doesn't eventuate, then existing shareholders probably aren't too pessimistic about the future direction of the share price.

View our latest analysis for Bharat Bijlee

What Are Growth Metrics Telling Us About The P/E?

The only time you'd be comfortable seeing a P/E like Bharat Bijlee's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered an exceptional 17% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 113% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 26% shows it's about the same on an annualised basis.

With this information, we can see why Bharat Bijlee is trading at a fairly similar P/E to the market. Apparently shareholders are comfortable to simply hold on assuming the company will continue keeping a low profile.

What We Can Learn From Bharat Bijlee's P/E?

Following Bharat Bijlee's share price tumble, its P/E is now hanging on to the median market P/E. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Bharat Bijlee maintains its moderate P/E off the back of its recent three-year growth being in line with the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings won't throw up any surprises. If recent medium-term earnings trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

Before you take the next step, you should know about the 1 warning sign for Bharat Bijlee that we have uncovered.

If you're unsure about the strength of Bharat Bijlee's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Bharat Bijlee might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BBL

Bharat Bijlee

Operates as an electrical engineering company in India and internationally.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor