David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Uno Minda Limited (NSE:UNOMINDA) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Uno Minda

What Is Uno Minda's Net Debt?

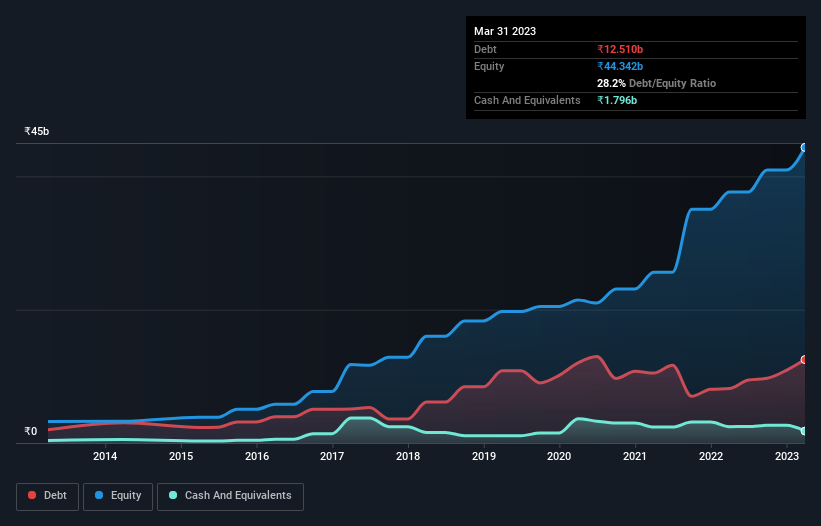

You can click the graphic below for the historical numbers, but it shows that as of March 2023 Uno Minda had ₹12.5b of debt, an increase on ₹8.16b, over one year. On the flip side, it has ₹1.80b in cash leading to net debt of about ₹10.7b.

How Healthy Is Uno Minda's Balance Sheet?

The latest balance sheet data shows that Uno Minda had liabilities of ₹29.5b due within a year, and liabilities of ₹9.22b falling due after that. Offsetting these obligations, it had cash of ₹1.80b as well as receivables valued at ₹17.2b due within 12 months. So it has liabilities totalling ₹19.7b more than its cash and near-term receivables, combined.

Given Uno Minda has a market capitalization of ₹328.4b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Uno Minda has a low net debt to EBITDA ratio of only 0.86. And its EBIT covers its interest expense a whopping 11.7 times over. So we're pretty relaxed about its super-conservative use of debt. On top of that, Uno Minda grew its EBIT by 62% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Uno Minda can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Considering the last three years, Uno Minda actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Happily, Uno Minda's impressive EBIT growth rate implies it has the upper hand on its debt. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. All these things considered, it appears that Uno Minda can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Uno Minda insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:UNOMINDA

Uno Minda

Manufactures and supplies auto components and systems in India and internationally.

Flawless balance sheet with high growth potential.