Advertisement

- India

- /

- Auto Components

- /

- NSEI:SUNCLAY

Sundaram-Clayton Limited (NSE:SUNCLAY) Looks Just Right With A 25% Price Jump

The Sundaram-Clayton Limited (NSE:SUNCLAY) share price has done very well over the last month, posting an excellent gain of 25%. The last 30 days bring the annual gain to a very sharp 61%.

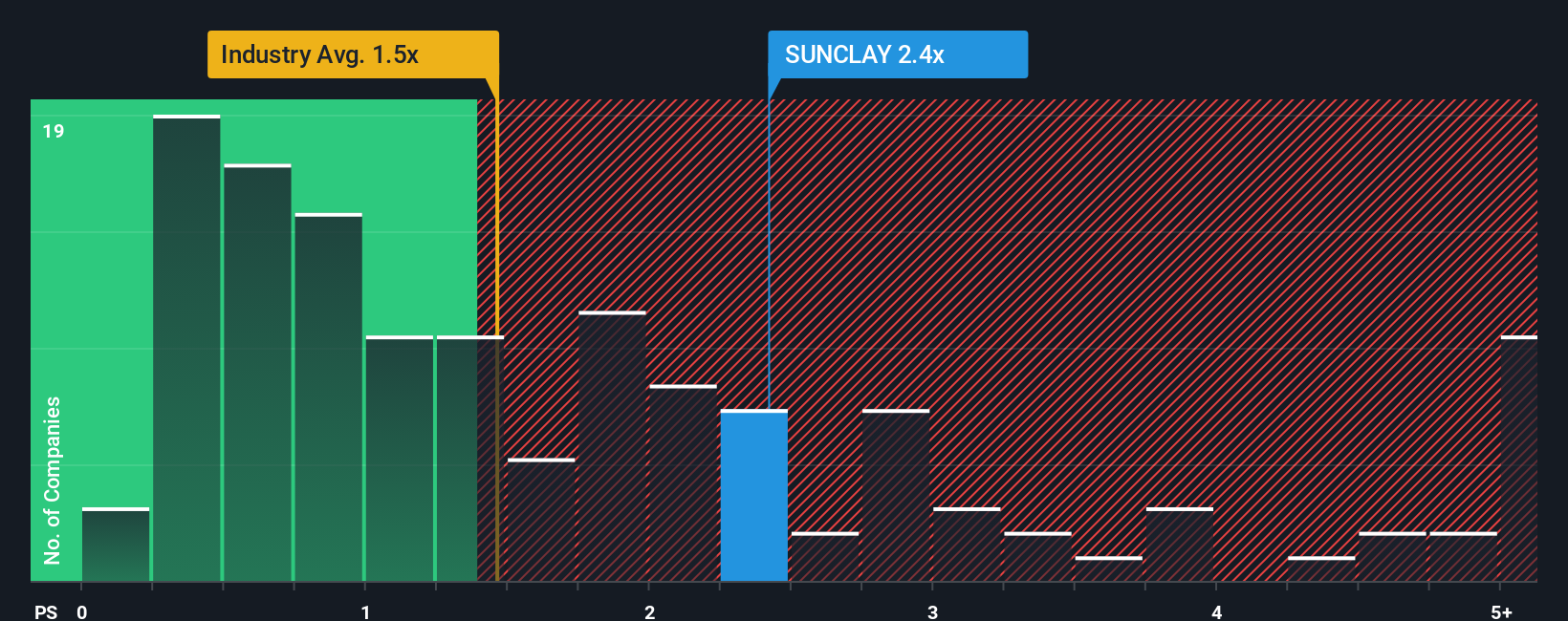

After such a large jump in price, given close to half the companies operating in India's Auto Components industry have price-to-sales ratios (or "P/S") below 1.5x, you may consider Sundaram-Clayton as a stock to potentially avoid with its 2.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Sundaram-Clayton

How Sundaram-Clayton Has Been Performing

Sundaram-Clayton certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Sundaram-Clayton will help you shine a light on its historical performance.Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as high as Sundaram-Clayton's is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company grew revenue by an impressive 57% last year. The strong recent performance means it was also able to grow revenue by 33% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

When compared to the industry's one-year growth forecast of 7.1%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's understandable that Sundaram-Clayton's P/S sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Final Word

Sundaram-Clayton shares have taken a big step in a northerly direction, but its P/S is elevated as a result. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

It's no surprise that Sundaram-Clayton can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. At this stage investors feel the potential continued revenue growth in the future is great enough to warrant an inflated P/S. If recent medium-term revenue trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 2 warning signs for Sundaram-Clayton you should be aware of.

If you're unsure about the strength of Sundaram-Clayton's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SUNCLAY

Sundaram-Clayton

Manufactures and sells non-ferrous gravity and pressure die castings in India.

Low risk and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor