- India

- /

- Auto Components

- /

- NSEI:IGARASHI

Igarashi Motors India (NSE:IGARASHI) Has A Somewhat Strained Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Igarashi Motors India Limited (NSE:IGARASHI) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Igarashi Motors India

What Is Igarashi Motors India's Net Debt?

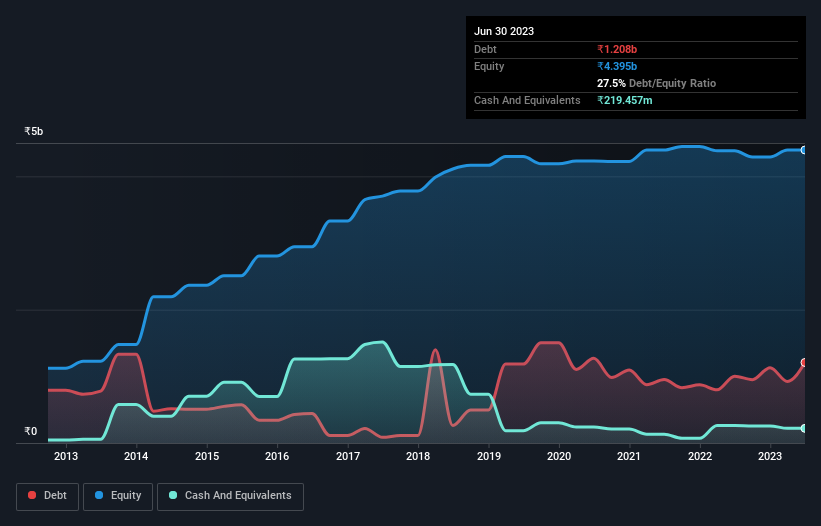

You can click the graphic below for the historical numbers, but it shows that as of March 2023 Igarashi Motors India had ₹1.21b of debt, an increase on ₹1.00b, over one year. However, it does have ₹219.5m in cash offsetting this, leading to net debt of about ₹988.4m.

How Healthy Is Igarashi Motors India's Balance Sheet?

The latest balance sheet data shows that Igarashi Motors India had liabilities of ₹2.33b due within a year, and liabilities of ₹535.7m falling due after that. Offsetting these obligations, it had cash of ₹219.5m as well as receivables valued at ₹1.78b due within 12 months. So it has liabilities totalling ₹863.2m more than its cash and near-term receivables, combined.

Of course, Igarashi Motors India has a market capitalization of ₹18.3b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Igarashi Motors India's net debt is sitting at a very reasonable 1.6 times its EBITDA, while its EBIT covered its interest expense just 3.1 times last year. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. Notably, Igarashi Motors India made a loss at the EBIT level, last year, but improved that to positive EBIT of ₹251m in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Igarashi Motors India's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Considering the last year, Igarashi Motors India actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Igarashi Motors India's struggle to convert EBIT to free cash flow had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. For example, its level of total liabilities is relatively strong. Looking at all the angles mentioned above, it does seem to us that Igarashi Motors India is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Igarashi Motors India (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:IGARASHI

Igarashi Motors India

Manufactures and sells electric micro motors and motor components in India, the United States, Japan, Germany, Hong Kong, and internationally.

Flawless balance sheet with proven track record.