- India

- /

- Auto Components

- /

- NSEI:ENDURANCE

It Looks Like Shareholders Would Probably Approve Endurance Technologies Limited's (NSE:ENDURANCE) CEO Compensation Package

Key Insights

- Endurance Technologies to hold its Annual General Meeting on 13th of August

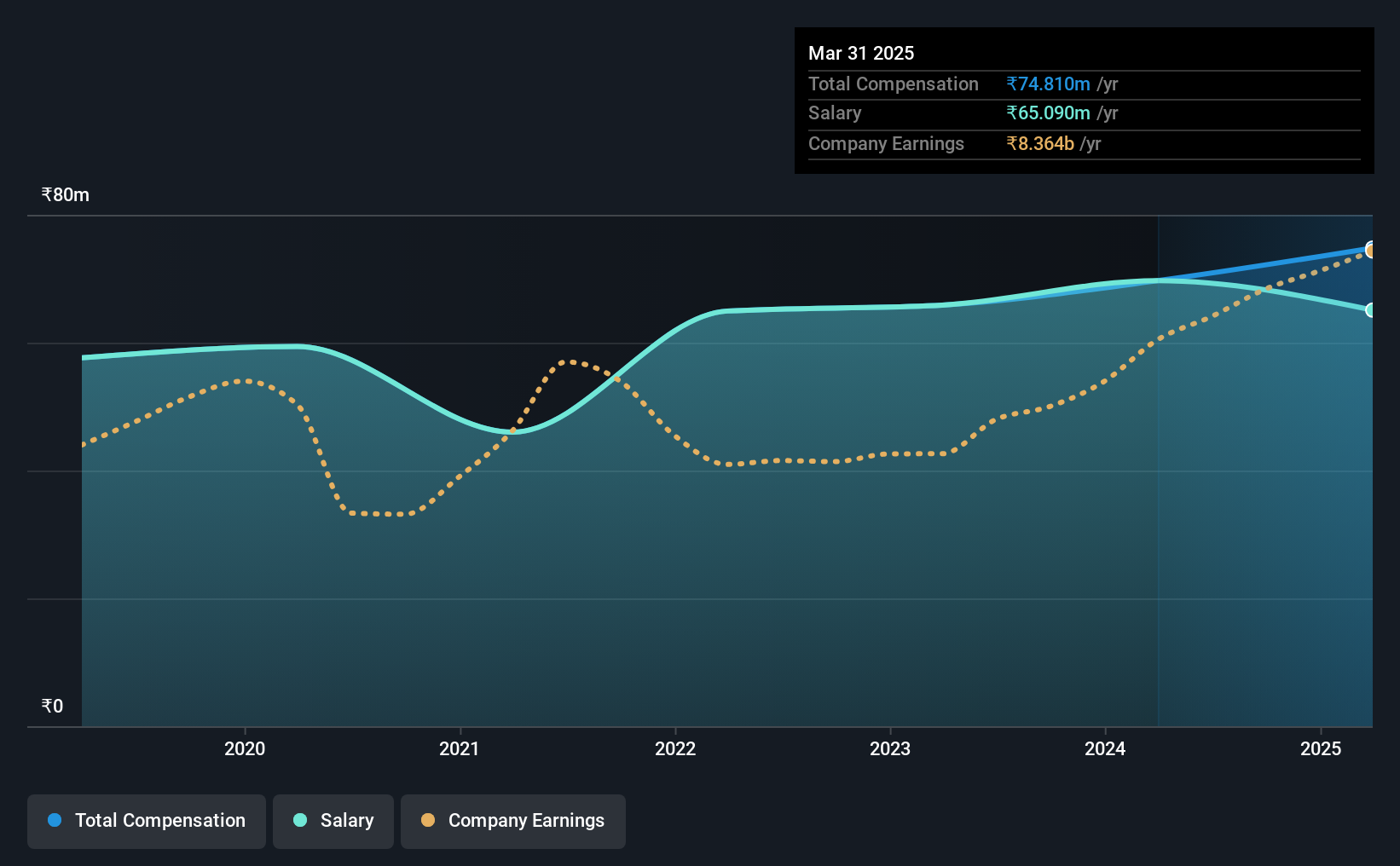

- Total pay for CEO Anurang Jain includes ₹65.1m salary

- The total compensation is similar to the average for the industry

- Endurance Technologies' total shareholder return over the past three years was 80% while its EPS grew by 22% over the past three years

It would be hard to discount the role that CEO Anurang Jain has played in delivering the impressive results at Endurance Technologies Limited (NSE:ENDURANCE) recently. Shareholders will have this at the front of their minds in the upcoming AGM on 13th of August. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. In light of the great performance, we discuss the case why we think CEO compensation is not excessive.

Check out our latest analysis for Endurance Technologies

How Does Total Compensation For Anurang Jain Compare With Other Companies In The Industry?

Our data indicates that Endurance Technologies Limited has a market capitalization of ₹358b, and total annual CEO compensation was reported as ₹75m for the year to March 2025. That's a modest increase of 7.3% on the prior year. Notably, the salary which is ₹65.1m, represents most of the total compensation being paid.

On comparing similar companies from the Indian Auto Components industry with market caps ranging from ₹175b to ₹562b, we found that the median CEO total compensation was ₹66m. From this we gather that Anurang Jain is paid around the median for CEOs in the industry. What's more, Anurang Jain holds ₹182b worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | ₹65m | ₹70m | 87% |

| Other | ₹9.7m | - | 13% |

| Total Compensation | ₹75m | ₹70m | 100% |

Talking in terms of the industry, salary represented approximately 79% of total compensation out of all the companies we analyzed, while other remuneration made up 21% of the pie. It's interesting to note that Endurance Technologies pays out a greater portion of remuneration through salary, compared to the industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Endurance Technologies Limited's Growth

Endurance Technologies Limited's earnings per share (EPS) grew 22% per year over the last three years. In the last year, its revenue is up 13%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Endurance Technologies Limited Been A Good Investment?

Boasting a total shareholder return of 80% over three years, Endurance Technologies Limited has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

Whatever your view on compensation, you might want to check if insiders are buying or selling Endurance Technologies shares (free trial).

Switching gears from Endurance Technologies, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Endurance Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ENDURANCE

Endurance Technologies

Manufactures and supplies automotive components for original equipment manufacturers in India and internationally.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)