Advertisement

We're Not Very Worried About Can-Fite BioPharma's (TLV:CANF) Cash Burn Rate

We can readily understand why investors are attracted to unprofitable companies. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So should Can-Fite BioPharma (TLV:CANF) shareholders be worried about its cash burn? For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for Can-Fite BioPharma

How Long Is Can-Fite BioPharma's Cash Runway?

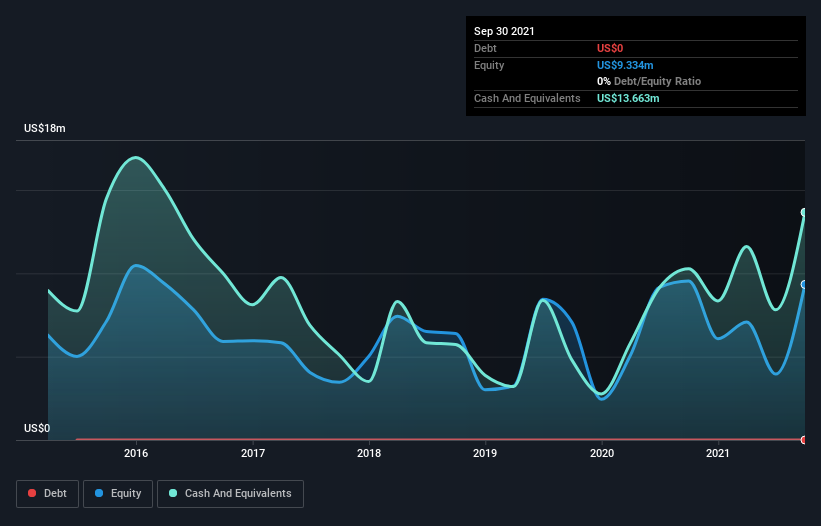

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. As at September 2021, Can-Fite BioPharma had cash of US$14m and no debt. In the last year, its cash burn was US$7.1m. So it had a cash runway of approximately 23 months from September 2021. Notably, analysts forecast that Can-Fite BioPharma will break even (at a free cash flow level) in about 3 years. Essentially, that means the company will either reduce its cash burn, or else require more cash. You can see how its cash balance has changed over time in the image below.

How Is Can-Fite BioPharma's Cash Burn Changing Over Time?

In our view, Can-Fite BioPharma doesn't yet produce significant amounts of operating revenue, since it reported just US$799k in the last twelve months. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. Even though it doesn't get us excited, the 46% reduction in cash burn year on year does suggest the company can continue operating for quite some time. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Hard Would It Be For Can-Fite BioPharma To Raise More Cash For Growth?

Even though it has reduced its cash burn recently, shareholders should still consider how easy it would be for Can-Fite BioPharma to raise more cash in the future. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Can-Fite BioPharma's cash burn of US$7.1m is about 27% of its US$27m market capitalisation. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

So, Should We Worry About Can-Fite BioPharma's Cash Burn?

On this analysis of Can-Fite BioPharma's cash burn, we think its cash burn reduction was reassuring, while its cash burn relative to its market cap has us a bit worried. One real positive is that analysts are forecasting that the company will reach breakeven. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Can-Fite BioPharma's situation. On another note, Can-Fite BioPharma has 6 warning signs (and 3 which don't sit too well with us) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:CANF

Can-Fite BioPharma

A clinical-stage biopharmaceutical company, develops orally bioavailable small molecule therapeutic products for the treatment of cancer, liver inflammatory diseases, and erectile dysfunction in Israel.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor