Advertisement

- Israel

- /

- Consumer Durables

- /

- TASE:ECP

Should Shareholders Reconsider Electra Consumer Products (1970) Ltd's (TLV:ECP) CEO Compensation Package?

Key Insights

- Electra Consumer Products (1970) will host its Annual General Meeting on 2nd of January

- Total pay for CEO Zvika Schwimmer includes ₪2.05m salary

- The overall pay is 662% above the industry average

- Electra Consumer Products (1970)'s EPS declined by 30% over the past three years while total shareholder loss over the past three years was 28%

Shareholders will probably not be too impressed with the underwhelming results at Electra Consumer Products (1970) Ltd (TLV:ECP) recently. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 2nd of January. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. The data we present below explains why we think CEO compensation is not consistent with recent performance.

View our latest analysis for Electra Consumer Products (1970)

Comparing Electra Consumer Products (1970) Ltd's CEO Compensation With The Industry

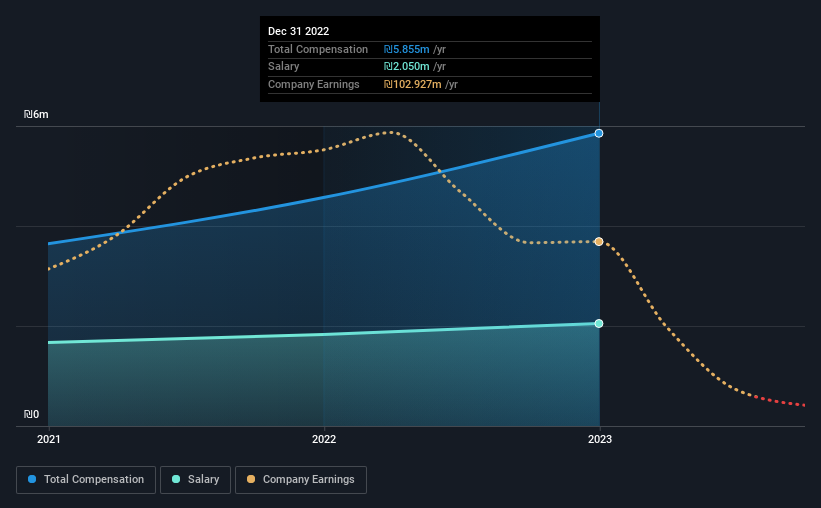

At the time of writing, our data shows that Electra Consumer Products (1970) Ltd has a market capitalization of ₪1.6b, and reported total annual CEO compensation of ₪5.9m for the year to December 2022. That's a notable increase of 28% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at ₪2.1m.

On comparing similar companies from the Israel Consumer Durables industry with market caps ranging from ₪725m to ₪2.9b, we found that the median CEO total compensation was ₪769k. This suggests that Zvika Schwimmer is paid more than the median for the industry.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | ₪2.1m | ₪1.8m | 35% |

| Other | ₪3.8m | ₪2.7m | 65% |

| Total Compensation | ₪5.9m | ₪4.6m | 100% |

Talking in terms of the industry, salary represented approximately 35% of total compensation out of all the companies we analyzed, while other remuneration made up 65% of the pie. Although there is a difference in how total compensation is set, Electra Consumer Products (1970) more or less reflects the market in terms of setting the salary. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Electra Consumer Products (1970) Ltd's Growth

Electra Consumer Products (1970) Ltd has reduced its earnings per share by 30% a year over the last three years. It achieved revenue growth of 5.2% over the last year.

The decline in EPS is a bit concerning. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Electra Consumer Products (1970) Ltd Been A Good Investment?

Since shareholders would have lost about 28% over three years, some Electra Consumer Products (1970) Ltd investors would surely be feeling negative emotions. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We identified 3 warning signs for Electra Consumer Products (1970) (2 don't sit too well with us!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Electra Consumer Products (1970) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:ECP

Electra Consumer Products (1970)

Manufactures, imports, exports, distributes, sells, and services for various consumer electrical products in Israel.

Acceptable track record with low risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor