- Hong Kong

- /

- Other Utilities

- /

- SEHK:882

Tianjin Development Holdings' (HKG:882) Upcoming Dividend Will Be Larger Than Last Year's

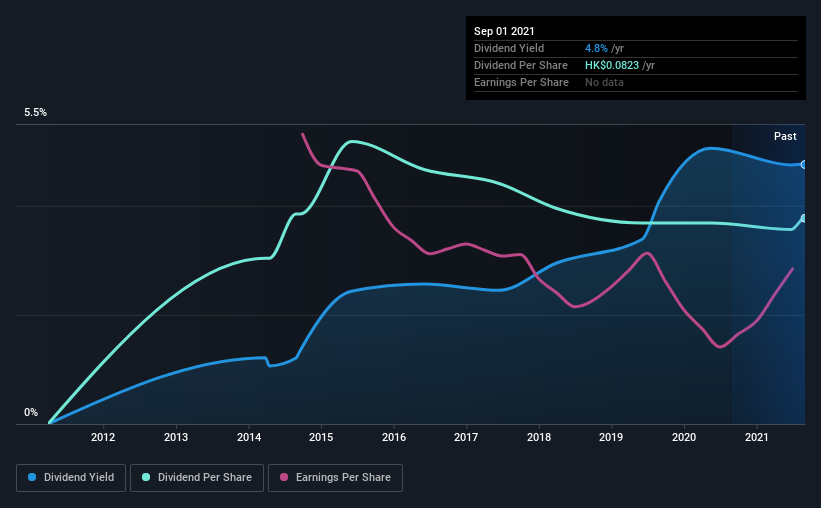

Tianjin Development Holdings Limited's (HKG:882) dividend will be increasing on the 29th of October to HK$0.035, with investors receiving 15% more than last year. This makes the dividend yield 4.8%, which is above the industry average.

View our latest analysis for Tianjin Development Holdings

Tianjin Development Holdings' Earnings Easily Cover the Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Before making this announcement, Tianjin Development Holdings was easily earning enough to cover the dividend. This means that most of what the business earns is being used to help it grow.

EPS is set to fall by 1.8% over the next 12 months if recent trends continue. If the dividend continues along recent trends, we estimate the payout ratio could be 19%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

Tianjin Development Holdings Is Still Building Its Track Record

Tianjin Development Holdings' dividend has been pretty stable for a little while now, but we will continue to be cautious until it has been demonstrated for a few more years. The dividend has gone from HK$0.066 in 2014 to the most recent annual payment of HK$0.082. This means that it has been growing its distributions at 3.1% per annum over that time. Tianjin Development Holdings hasn't been paying a dividend for very long, so we wouldn't get to excited about its record of growth just yet.

Dividend Growth May Be Hard To Achieve

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Unfortunately things aren't as good as they seem. Although it's important to note that Tianjin Development Holdings' earnings per share has basically not grown from where it was five years ago, which could erode the purchasing power of the dividend over time.

Our Thoughts On Tianjin Development Holdings' Dividend

In summary, while it's always good to see the dividend being raised, we don't think Tianjin Development Holdings' payments are rock solid. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. Overall, we don't think this company has the makings of a good income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Just as an example, we've come across 2 warning signs for Tianjin Development Holdings you should be aware of, and 1 of them is concerning. We have also put together a list of global stocks with a solid dividend.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tianjin Development Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:882

Tianjin Development Holdings

Through its subsidiaries, supplies water, heat, thermal power, and electricity to industrial, commercial, and residential customers in the People’s Republic of China.

Good value with adequate balance sheet and pays a dividend.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)