Advertisement

- Hong Kong

- /

- Gas Utilities

- /

- SEHK:384

China Gas Holdings (SEHK:384) Net Margin Declines to 3.6%, Undercutting Bullish Recovery Narratives

Simply Wall St

Reviewed by Simply Wall St

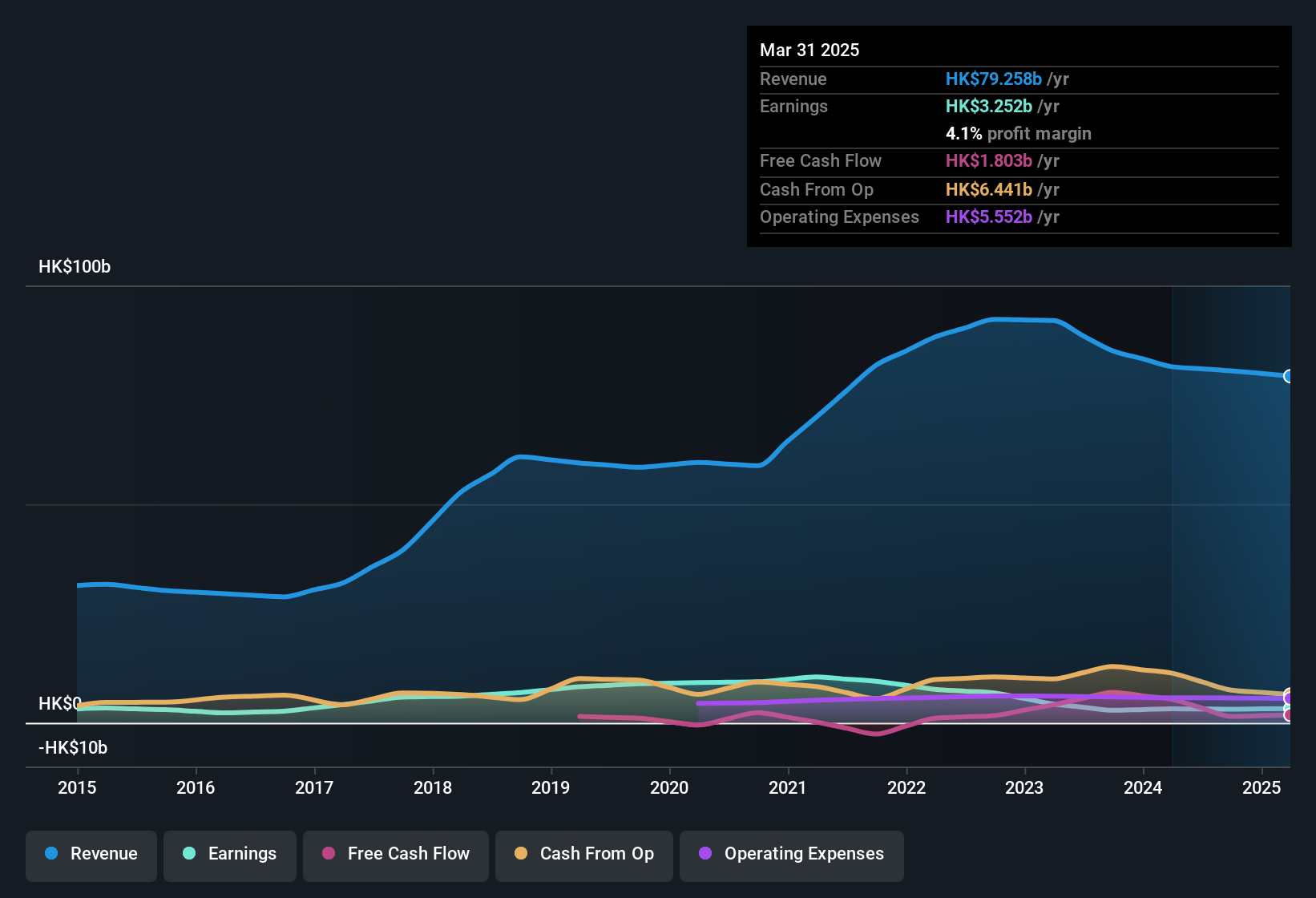

China Gas Holdings (SEHK:384) just posted its H1 2026 results, revealing revenue of $34.5 billion HKD and basic EPS of 0.25 HKD. Looking back, the company has seen revenue swing from $35.1 billion HKD in the first half of 2025, to $44.2 billion HKD in the second half, before settling at this half-year's figure. Basic EPS moved from 0.33 HKD to 0.28 HKD across the same periods. Overall, profit margins have come under pressure, setting the stage for how investors should interpret the changing earnings landscape.

See our full analysis for China Gas Holdings.With the headline numbers in, it is time to see how these results stack up against the dominant narratives investors have been following.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Profit Drops to $1.3 Billion Amid Pressure

- Net income for H1 2026 was $1.3 billion HKD, down from $1.8 billion HKD in H1 2025 and $1.5 billion HKD in H2 2025, indicating persistent year-on-year contraction.

- Notably, the discussion around moderate earnings growth contrasts with the actual profit margin, which slipped to 3.6% over the last 12 months. This is lower than last year’s 3.9%.

- This trend supports prevailing market opinion that while the company’s core energy business provides resilience, declining profitability could limit potential upside until operational improvements are realized.

- Analysts also point to the 30.6% annual average decline in earnings over five years as a key challenge, even as sector tailwinds continue.

- Expectations for earnings to grow by 10.66% per year are now less certain when compared with the recent declines in margins and profits.

Share Price Trades 44.8% Below DCF Fair Value

- At $8.6 HKD, the current share price is 44.8% below the calculated DCF fair value of $15.57 HKD, leaving a significant valuation gap for investors monitoring recovery prospects.

- The consensus perspective suggests this discount may reflect both hopes for future upside and recognition of existing risks, as the company’s 16.6x price-to-earnings ratio remains above both industry (13.6x) and peer (11.7x) averages.

- Although the discounted price may appear as an opportunity for value-seekers, investors see the elevated P/E as an indication that market concerns about profit durability and near-term growth are prevalent.

- This blend of pessimism and optimism reflects the broad market view that valuation is tied not just to share price, but to the company’s ability to deliver growth that justifies that valuation.

- Visible balance sheet improvements or margin recovery may be necessary before the market closes this valuation gap in a sustained manner.

Dividend Not Covered by Earnings or Cash Flow

- The dividend yield is 5.81%, but the payout is not covered by earnings or free cash flow, and debt coverage by operating cash flow is also weak.

- The market generally flags this as a significant risk for income-focused investors, given the combination of high yield and poor coverage, raising concerns about dividend sustainability.

- This challenge is exacerbated by ongoing declines in profitability and margin, suggesting that maintaining the current dividend could place additional strain on future cash flow.

- While the headline yield may attract interest, the risks emphasize the need for caution when considering China Gas Holdings for stable income-producing potential.

To see how shifting financials stack up against market narratives and future forecasts, jump into the full consensus storyline for China Gas Holdings. 📊 Read the full China Gas Holdings Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on China Gas Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

China Gas Holdings faces ongoing profit margin pressure, weak dividend coverage, and balance sheet concerns. These factors could challenge its long-term income and stability.

If you want stocks with stronger core finances, check out solid balance sheet and fundamentals stocks screener (1939 results) where you'll find companies built on healthier balance sheets and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:384

China Gas Holdings

An investment holding company, operates as an energy supplier and service provider in the People’s Republic of China.

Mediocre balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative