Advertisement

- Hong Kong

- /

- Renewable Energy

- /

- SEHK:2380

China Power International Development (SEHK:2380): Valuation Check After Weaker Electricity Sales Data

Simply Wall St

Reviewed by Simply Wall St

China Power International Development (SEHK:2380) has just reported lower unaudited electricity sales, with October volumes down about 5% and year-to-date sales slipping roughly 3% versus last year, raising fresh questions about demand momentum.

See our latest analysis for China Power International Development.

Even with October’s softer sales, the share price has quietly ground higher, with a roughly mid-teens year to date share price return and a notably stronger multi year total shareholder return, suggesting underlying confidence rather than fading momentum.

If this shift in sentiment has you reconsidering your watchlist, it could be worth broadening the lens and exploring fast growing stocks with high insider ownership.

Against that backdrop of softer demand but solid multi year returns, are investors still underestimating China Power’s earnings power, or has the recent re rating already captured the next leg of its growth story?

Price-to-Earnings of 11.5x: Is it justified?

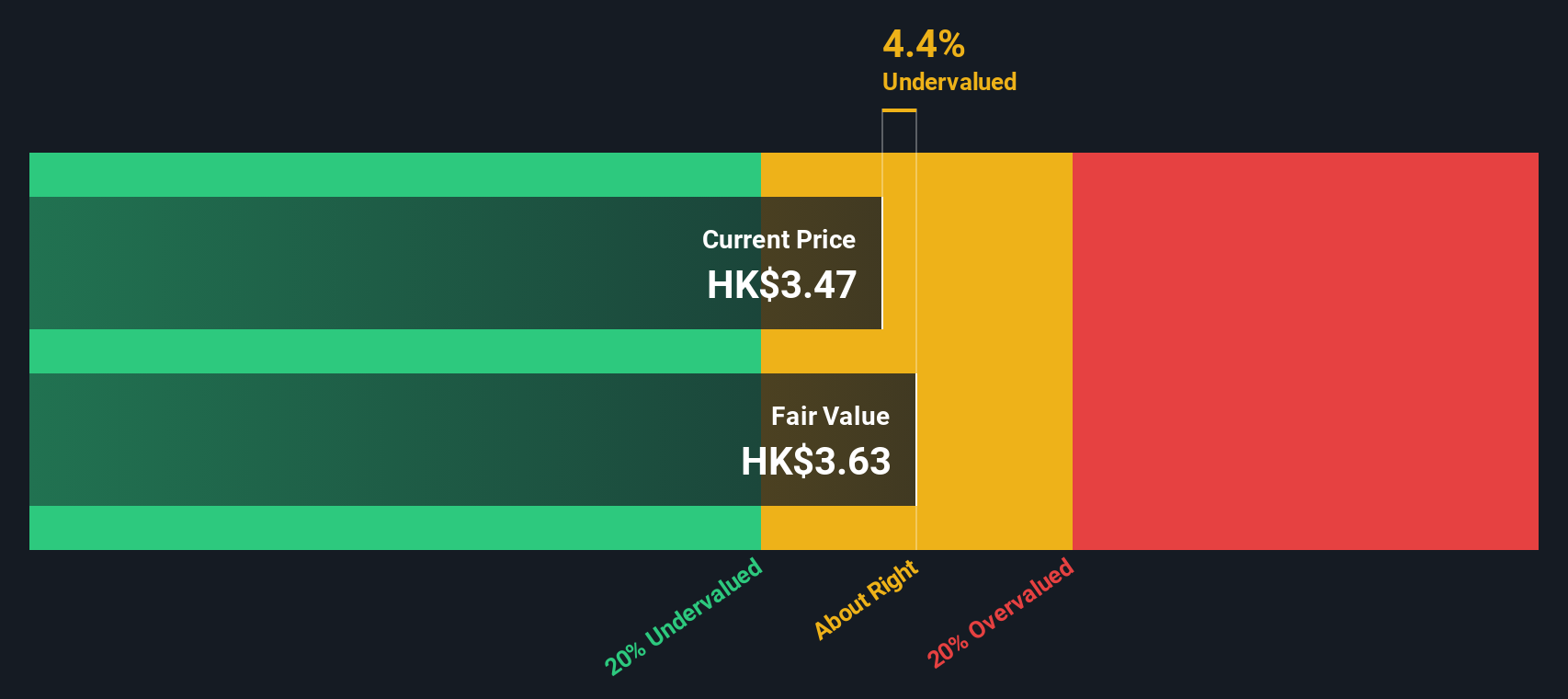

On a headline basis, China Power International Development trades on a price-to-earnings ratio of 11.5x, a level that looks slightly rich versus some benchmarks but not extreme at its last close of HK$3.47.

The price-to-earnings multiple compares the current share price with the company’s earnings per share, making it a simple way to see how much investors are paying for each unit of profit. For a diversified power producer with meaningful exposure to renewable assets, this measure helps frame how the market is pricing its profit stability and expected growth.

Relative signals are mixed, though. The stock screens as expensive versus its immediate peer group, where the average multiple is around 6.7x, and it also sits a touch above the estimated fair price-to-earnings ratio of 11.3x. This implies limited room for error if earnings disappoint. Yet when set against the broader Asian renewable energy industry average multiple of 16.8x, its 11.5x looks materially more conservative, suggesting investors are not assigning a premium in line with the sector’s higher growth names.

Explore the SWS fair ratio for China Power International Development

Result: Price-to-Earnings of 11.5x (ABOUT RIGHT)

However, softer power demand and any earnings miss at today’s valuation could quickly flip sentiment, especially if policy support or renewables execution disappoints.

Find out about the key risks to this China Power International Development narrative.

Another Lens on Value

Our SWS DCF model points to a fair value of about HK$3.63 per share, a modest 4.4% above the current HK$3.47 price. That implies only a thin margin of safety, so does this really offer upside, or just limited room for disappointment if growth stumbles?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out China Power International Development for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 925 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own China Power International Development Narrative

If you see the numbers differently or prefer to dig into the details yourself, you can build a complete narrative in just a few minutes: Do it your way.

A great starting point for your China Power International Development research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about sharpening your edge, do not stop at one stock when you can instantly scan curated opportunities tailored to your strategy with Simply Wall Street.

- Capture the upside of early stage potential by targeting these 3576 penny stocks with strong financials that already show stronger balance sheets and business quality than typical speculative names.

- Ride the structural tailwind of automation and machine learning by focusing on these 24 AI penny stocks positioned to benefit as AI spending accelerates worldwide.

- Lock in quality at a discount by zeroing in on these 925 undervalued stocks based on cash flows where cash flow strength and price still appear meaningfully misaligned.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2380

China Power International Development

An investment holding company, develops, constructs, owns, operates, and manages power plants in the People’s Republic of China and internationally.

Slightly overvalued with limited growth.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

21 followersusers have followed this narrative

6 commentsusers have commented on this narrative

5 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

949 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative