Advertisement

- Hong Kong

- /

- Renewable Energy

- /

- SEHK:1071

Huadian Power International Corporation Limited Just Missed EPS By 6.9%: Here's What Analysts Think Will Happen Next

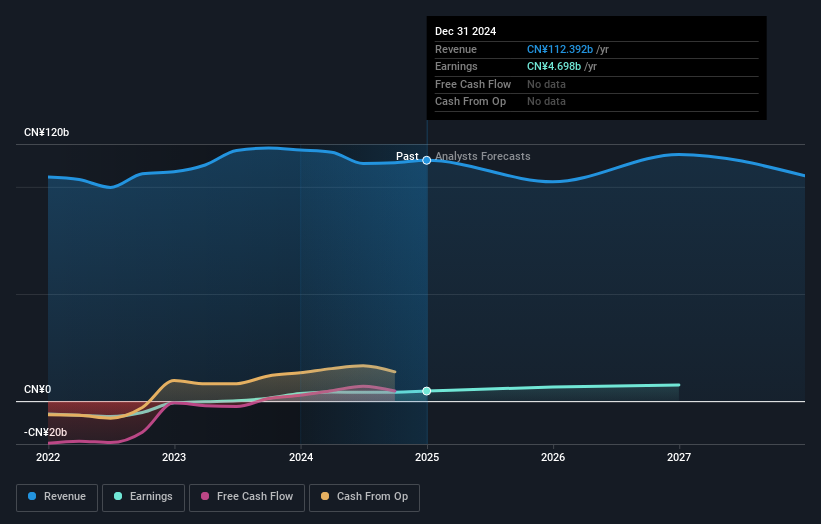

As you might know, Huadian Power International Corporation Limited (HKG:1071) recently reported its yearly numbers. It looks like the results were a bit of a negative overall. While revenues of CN¥112b were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 6.9% to hit CN¥0.46 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Following the recent earnings report, the consensus from five analysts covering Huadian Power International is for revenues of CN¥102.4b in 2025. This implies a chunky 8.9% decline in revenue compared to the last 12 months. Statutory earnings per share are predicted to bounce 30% to CN¥0.60. In the lead-up to this report, the analysts had been modelling revenues of CN¥115.7b and earnings per share (EPS) of CN¥0.61 in 2025. It looks like sentiment has fallen somewhat in the aftermath of these results, with a real cut to revenue estimates and a minor downgrade to earnings per share numbers as well.

See our latest analysis for Huadian Power International

Despite the cuts to forecast earnings, there was no real change to the HK$5.04 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Huadian Power International at HK$5.49 per share, while the most bearish prices it at HK$4.61. Still, with such a tight range of estimates, it suggeststhe analysts have a pretty good idea of what they think the company is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Huadian Power International's past performance and to peers in the same industry. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 8.9% by the end of 2025. This indicates a significant reduction from annual growth of 4.9% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.1% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Huadian Power International is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target held steady at HK$5.04, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Huadian Power International. Long-term earnings power is much more important than next year's profits. We have forecasts for Huadian Power International going out to 2027, and you can see them free on our platform here.

Even so, be aware that Huadian Power International is showing 2 warning signs in our investment analysis , and 1 of those can't be ignored...

Valuation is complex, but we're here to simplify it.

Discover if Huadian Power International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1071

Huadian Power International

Engages in the generation and sale of electricity, heat, and coal to power grid companies in the People’s Republic of China.

Solid track record average dividend payer.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor