Advertisement

- Hong Kong

- /

- Telecom Services and Carriers

- /

- SEHK:762

China Unicom (Hong Kong) (SEHK:762) Reports Strong Q3 Earnings Growth with 5G Subscriber Expansion

Simply Wall St

Reviewed by Simply Wall St

China Unicom (Hong Kong) (SEHK:762) has reported strong financial results for the nine months ending September 2024, with revenue climbing to CNY 290.12 billion and net income reaching CNY 19.03 billion, underscoring its strong market position and effective strategic initiatives. However, the company faces challenges such as a low return on equity and management team experience concerns, which may impact its ability to navigate evolving market dynamics. Readers should anticipate a discussion on how China Unicom plans to leverage its 5G and IoT advancements to enhance growth prospects amidst these challenges.

Get an in-depth perspective on China Unicom (Hong Kong)'s performance by reading our analysis here.

Competitive Advantages That Elevate China Unicom (Hong Kong)

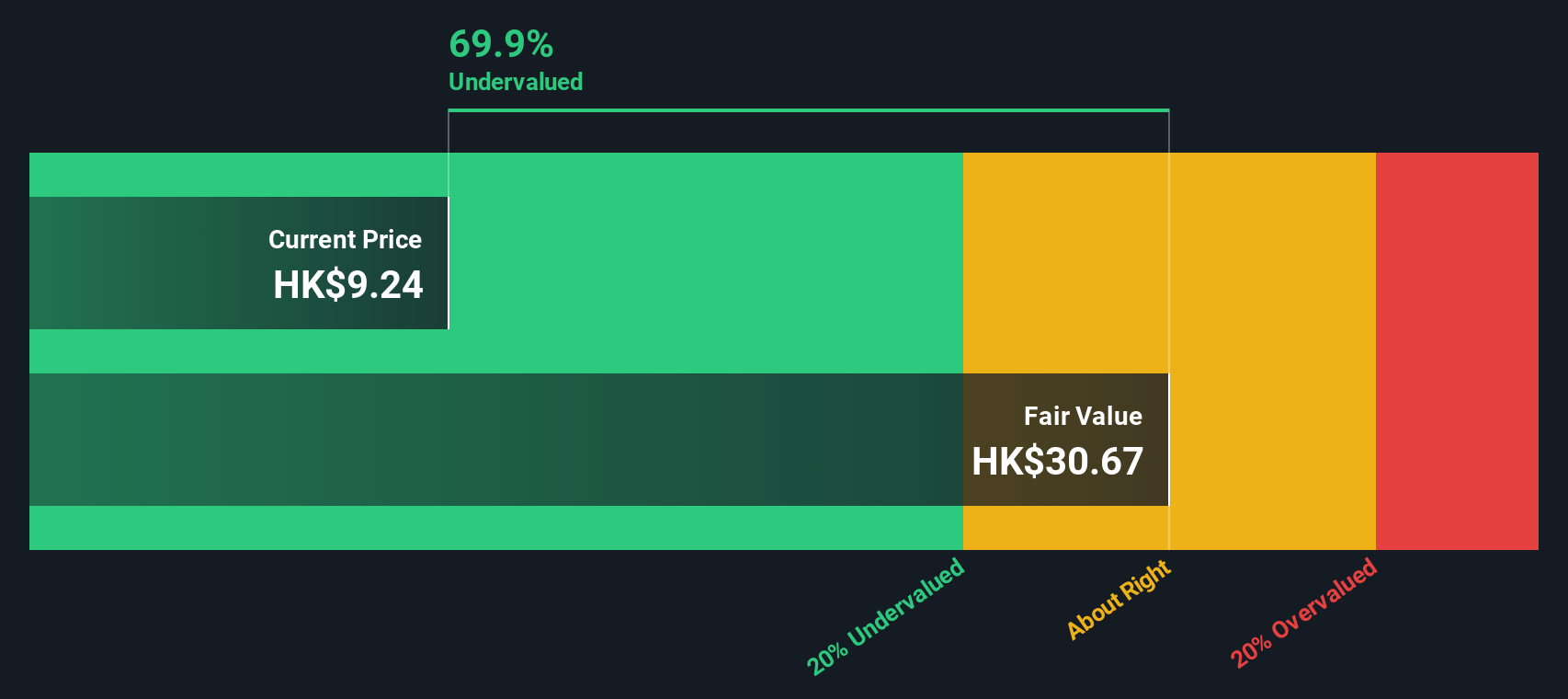

China Unicom (Hong Kong) has demonstrated impressive financial health, with earnings growing at 12.8% annually over the past five years. This growth outpaces the telecom industry average, highlighting the company's strong market position. The recent earnings report for the nine months ending September 2024 shows a revenue increase to CNY 290.12 billion, up from CNY 281.69 billion the previous year, and net income rising to CNY 19.03 billion, reflecting strong operational performance. The company's strategic initiatives, such as product innovation and customer retention strategies, have bolstered its market share and profitability. With a reasonable payout ratio of 56.9%, dividend payments are well-covered, contributing to investor confidence. Furthermore, the company trades at a significant discount to its estimated fair value, indicating potential upside for investors.

Vulnerabilities Impacting China Unicom (Hong Kong)

Despite its strong financial performance, the company faces challenges, including a low return on equity of 5.7%, which is below the industry benchmark. The management team, with an average tenure of only 0.9 years, may lack the experience needed to navigate complex market dynamics effectively. Additionally, the company's dividend payments have been volatile over the past decade, potentially deterring some investors. Forecasted earnings and revenue growth rates of 5.4% and 2.6% per year, respectively, lag behind market averages, suggesting a need for strategic adjustments to enhance growth prospects.

Future Prospects for China Unicom (Hong Kong) in the Market

Opportunities abound for China Unicom, particularly in expanding its 5G and Internet-of-Things (IoT) offerings. The company reported a substantial number of 5G package subscribers, reaching 285.60 million as of September 2024. Strategic alliances and product-related announcements could further strengthen its market position and capitalize on emerging technologies. Trading at a 45.1% discount to its estimated fair value, the company is well-positioned to attract investors seeking growth potential.

External Factors Threatening China Unicom (Hong Kong)

External threats include economic headwinds that could impact consumer spending, as well as intensifying market competition from new entrants with aggressive pricing strategies. Regulatory changes in key markets pose additional challenges, requiring the company to adapt its business practices accordingly. The history of unstable dividend payments may also deter potential investors, emphasizing the need for consistent financial strategies to maintain investor confidence.

To learn about how China Unicom (Hong Kong)'s valuation metrics are shaping its market position, check out our detailed analysis of China Unicom (Hong Kong)'s Valuation.

Conclusion

China Unicom (Hong Kong) showcases strong financial health with a 12.8% annual earnings growth over the past five years, surpassing the telecom industry average and reinforcing its market position. However, challenges such as a low return on equity, inexperienced management, and volatile dividends highlight areas needing strategic focus. The company's significant discount to its estimated fair value, with a target price exceeding the current share price by over 20%, presents a compelling opportunity for investors seeking growth, especially as it expands its 5G and IoT offerings. Despite external threats like economic headwinds and regulatory changes, China Unicom's strategic initiatives and market positioning suggest potential for sustained performance and investor confidence in the future.

Where To Now?

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About SEHK:762

China Unicom (Hong Kong)

An investment holding company, provides telecommunications and related value-added services in the People’s Republic of China.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor