Advertisement

- Hong Kong

- /

- Communications

- /

- SEHK:8245

We Think On Real International Holdings (HKG:8245) Has A Fair Chunk Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, On Real International Holdings Limited (HKG:8245) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for On Real International Holdings

What Is On Real International Holdings's Debt?

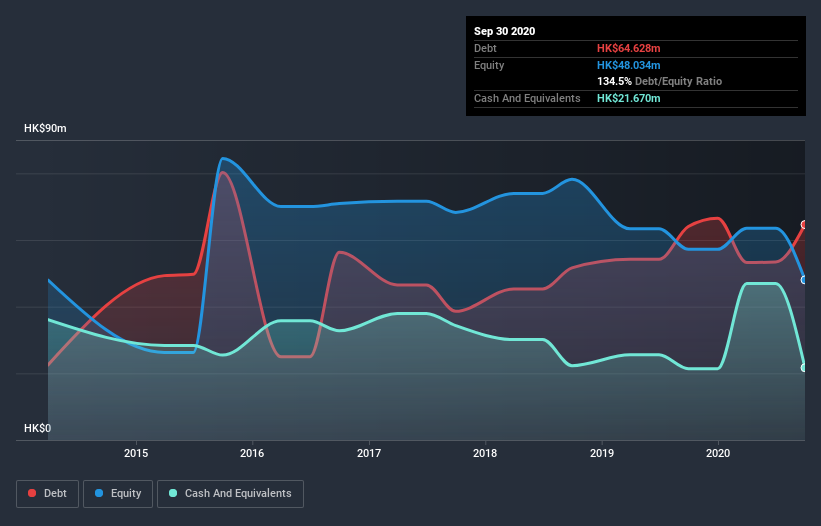

As you can see below, On Real International Holdings had HK$64.6m of debt, at September 2020, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has HK$21.7m in cash leading to net debt of about HK$43.0m.

How Strong Is On Real International Holdings' Balance Sheet?

According to the balance sheet data, On Real International Holdings had liabilities of HK$146.2m due within 12 months, but no longer term liabilities. On the other hand, it had cash of HK$21.7m and HK$136.2m worth of receivables due within a year. So it actually has HK$11.7m more liquid assets than total liabilities.

This excess liquidity suggests that On Real International Holdings is taking a careful approach to debt. Because it has plenty of assets, it is unlikely to have trouble with its lenders. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since On Real International Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year On Real International Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 8.3%, to HK$353m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Over the last twelve months On Real International Holdings produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable HK$25m at the EBIT level. On a more positive note, the company does have liquid assets, so it has a bit of time to improve its operations before the debt becomes an acute problem. But we'd want to see some positive free cashflow before spending much time on trying to understand the stock. So it seems too risky for our taste. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 5 warning signs for On Real International Holdings (3 make us uncomfortable) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade On Real International Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:8245

Shanyu Group Holdings

An investment holding company, designs, trades, and manufactures two-way radios, baby monitors, and plastic products in Europe, the People’s Republic of China, the United States, Taiwan, Hong Kong, and Australia.

Moderate risk with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor