Advertisement

- Japan

- /

- Personal Products

- /

- TSE:4922

Three Stocks That May Be Priced Below Their Estimated Value In December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate through a period of cautious optimism and uncertainty, marked by recent rate cuts from the Federal Reserve and political tensions, investors are keenly observing how these developments impact stock valuations. With U.S. stocks experiencing broad-based declines amid concerns over interest rates and economic policies, identifying potentially undervalued stocks becomes crucial for those looking to capitalize on market inefficiencies. In such an environment, a good stock is often characterized by strong fundamentals that may not be fully reflected in its current market price, offering potential opportunities for value-oriented investors.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Alltop Technology (TPEX:3526) | NT$266.00 | NT$530.76 | 49.9% |

| Clear Secure (NYSE:YOU) | US$26.66 | US$53.14 | 49.8% |

| Wasion Holdings (SEHK:3393) | HK$7.03 | HK$14.00 | 49.8% |

| Management SolutionsLtd (TSE:7033) | ¥1710.00 | ¥3411.87 | 49.9% |

| Hanza (OM:HANZA) | SEK76.20 | SEK151.92 | 49.8% |

| HealthEquity (NasdaqGS:HQY) | US$94.95 | US$189.22 | 49.8% |

| Medley (TSE:4480) | ¥3840.00 | ¥7644.63 | 49.8% |

| GRCS (TSE:9250) | ¥1415.00 | ¥2827.70 | 50% |

| South Atlantic Bancshares (OTCPK:SABK) | US$15.02 | US$29.98 | 49.9% |

| KebNi (OM:KEBNI B) | SEK1.09 | SEK2.17 | 49.8% |

Let's explore several standout options from the results in the screener.

NagaCorp (SEHK:3918)

Overview: NagaCorp Ltd. is an investment holding company that manages and operates a hotel and casino complex in the Kingdom of Cambodia, with a market cap of HK$12.96 billion.

Operations: The company generates revenue primarily from casino operations, amounting to $545.61 million, and hotel and entertainment operations, which contribute $23.22 million.

Estimated Discount To Fair Value: 18.5%

NagaCorp is trading at HK$2.92, below its estimated fair value of HK$3.58, indicating potential undervaluation based on cash flows. Despite a decline in profit margins from 30% to 17.7%, earnings are forecast to grow significantly at 42.4% annually, outpacing the Hong Kong market's expected growth of 11.6%. However, revenue growth is modest at 10.5% annually and return on equity is projected to be low at 10.7%. Recent board changes include Ms. Monica Lam's transition to a non-executive director role.

- Our comprehensive growth report raises the possibility that NagaCorp is poised for substantial financial growth.

- Dive into the specifics of NagaCorp here with our thorough financial health report.

FIT Hon Teng (SEHK:6088)

Overview: FIT Hon Teng Limited manufactures and sells mobile and wireless devices and connectors in Taiwan and internationally, with a market cap of HK$22.25 billion.

Operations: The company's revenue is derived from Consumer Products, contributing $690.95 million, and Intermediate Products, generating $3.94 billion.

Estimated Discount To Fair Value: 22%

FIT Hon Teng, trading at HK$3.26, is valued below its estimated fair value of HK$4.18, highlighting potential undervaluation based on cash flows. Earnings are projected to grow significantly at 31.7% annually, surpassing the Hong Kong market's 11.6%, although revenue growth is slower at 17.5%. Despite recent share price volatility and a forecasted low return on equity of 11%, FIT's innovations in AI data center technologies emphasize its strategic focus and industry leadership potential.

- Our growth report here indicates FIT Hon Teng may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of FIT Hon Teng.

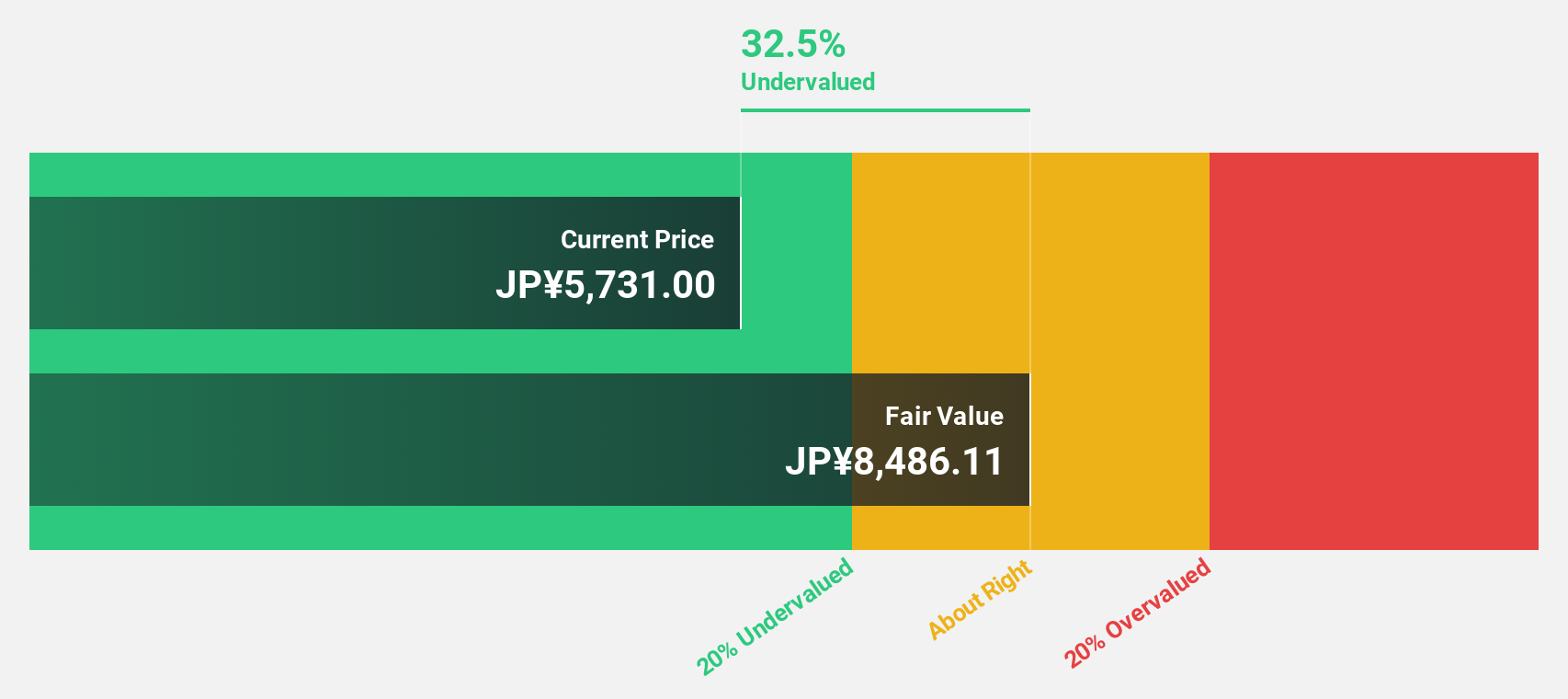

KOSÉ (TSE:4922)

Overview: KOSÉ Corporation manufactures and sells cosmetics and cosmetology products primarily in Japan and internationally, with a market cap of ¥393.29 billion.

Operations: The company's revenue is primarily derived from its Cosmetics Business segment, which accounts for ¥253.43 billion, followed by the Cosmetaries segment at ¥64.22 billion.

Estimated Discount To Fair Value: 19.8%

KOSÉ, trading at ¥6,884, is priced below its fair value estimate of ¥8,585.27 by 19.8%, suggesting potential undervaluation based on cash flows. Earnings are expected to grow significantly at 22.3% annually, outpacing the Japanese market's 7.9%. However, profit margins have decreased from last year and the dividend yield of 2.03% isn't well covered by earnings or free cash flows. Recent organizational changes aim to enhance operations in Europe and America.

- The analysis detailed in our KOSÉ growth report hints at robust future financial performance.

- Take a closer look at KOSÉ's balance sheet health here in our report.

Key Takeaways

- Delve into our full catalog of 876 Undervalued Stocks Based On Cash Flows here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KOSÉ might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4922

KOSÉ

Manufactures and sells cosmetics and cosmetology products primarily in Japan and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|60.9% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.7% undervalued

ZW

Community Contributor