Advertisement

The Bull Case For Inspur Digital Enterprise Technology (SEHK:596) Could Change Following Its HK$494m Follow-on Equity Offering

Simply Wall St

Reviewed by Sasha Jovanovic

- Inspur Digital Enterprise Technology Limited has completed a follow-on equity offering of HK$493,728,200, issuing 67,634,000 new ordinary shares at HK$7.30 per share with a HK$0.0511 discount per share via a subsequent direct listing.

- This capital raise expands the company’s funding flexibility while modestly increasing the free float, factors that can reshape how investors view its balance between growth ambitions and ownership dilution.

- We’ll now examine how this follow-on equity offering, and the associated increase in outstanding shares, influences Inspur Digital Enterprise Technology’s investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

What Is Inspur Digital Enterprise Technology's Investment Narrative?

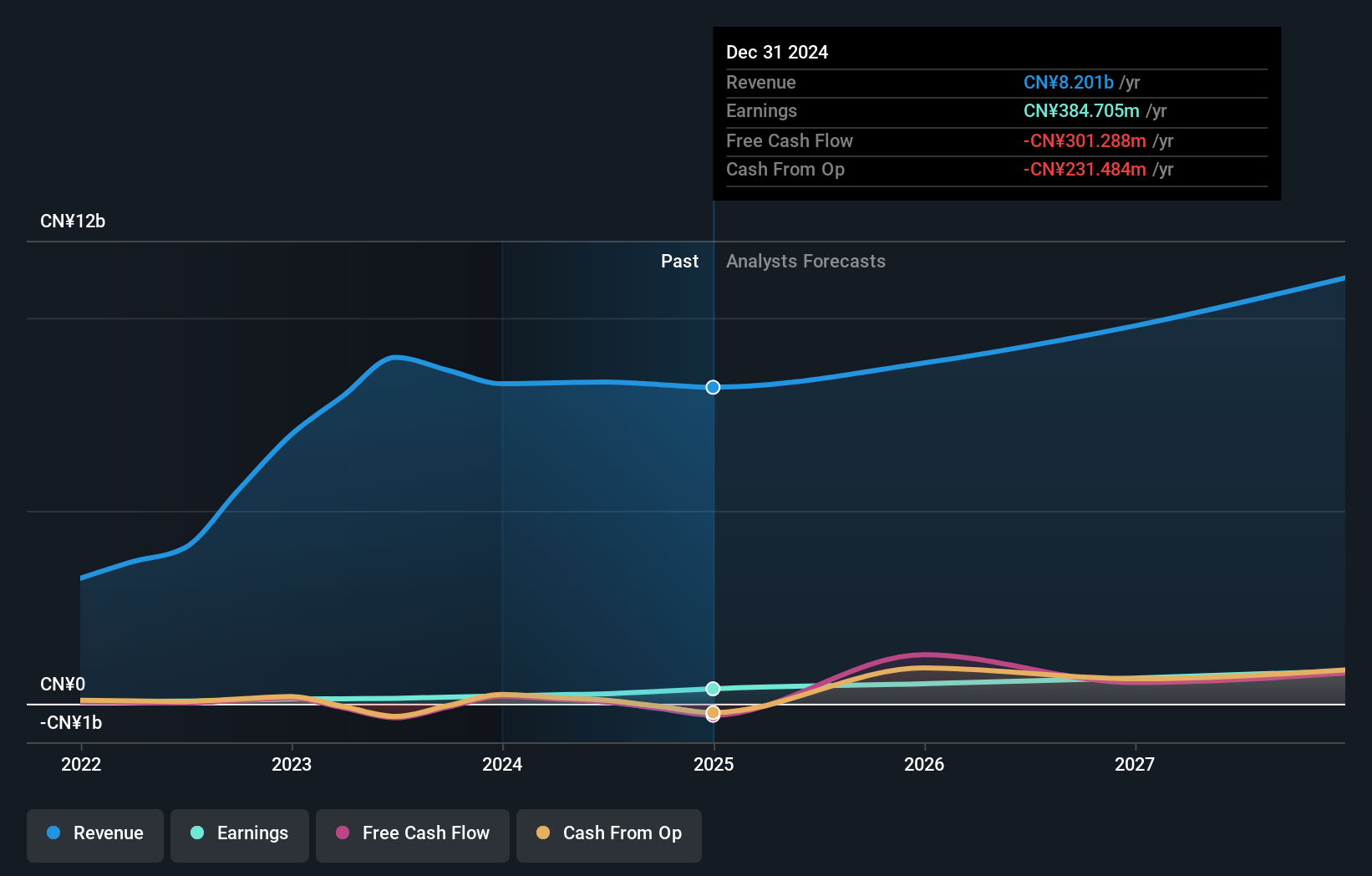

To own Inspur Digital Enterprise Technology, you really need to believe its cloud and software transition can keep translating into steady revenue and earnings growth, even if that trajectory is uneven at times. Recent results have shown improving profitability and margins, and the board has been willing to return some cash via dividends, which helps anchor the story. The new HK$493,728,200 follow-on equity offering fits into this narrative as fresh funding that can support further cloud build‑out or product investment without stretching the balance sheet, but it also slightly dilutes existing holders and raises the execution bar for management. In the near term, the key catalysts still sit around sustaining profit growth and integrating new capital efficiently, while governance quality and non‑cash earnings remain important watchpoints.

However, investors should be aware of how dilution and governance could interact with those earnings headlines. Despite retreating, Inspur Digital Enterprise Technology's shares might still be trading above their fair value and there could be some more downside. Discover how much.Exploring Other Perspectives

Explore 4 other fair value estimates on Inspur Digital Enterprise Technology - why the stock might be worth over 2x more than the current price!

Build Your Own Inspur Digital Enterprise Technology Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Inspur Digital Enterprise Technology research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Inspur Digital Enterprise Technology research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Inspur Digital Enterprise Technology's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Find companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:596

Inspur Digital Enterprise Technology

An investment holding company, engages in management software development, cloud services, and sale of Internet of Things (IoT) solutions in the People’s Republic of China.

Very undervalued with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

46 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative