Advertisement

Can Sino-i Technology Limited (HKG:250) Maintain Its Strong Returns?

One of the best investments we can make is in our own knowledge and skill set. With that in mind, this article will work through how we can use Return On Equity (ROE) to better understand a business. By way of learning-by-doing, we'll look at ROE to gain a better understanding of Sino-i Technology Limited (HKG:250).

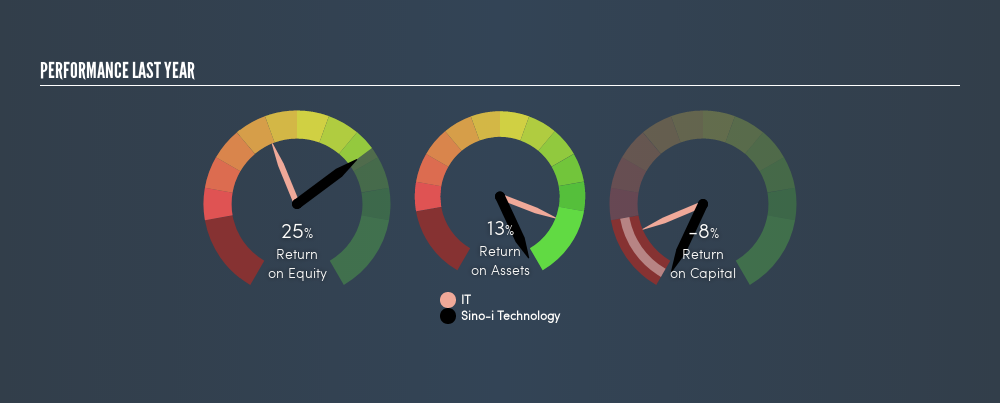

Sino-i Technology has a ROE of 25%, based on the last twelve months. That means that for every HK$1 worth of shareholders' equity, it generated HK$0.25 in profit.

Check out our latest analysis for Sino-i Technology

How Do I Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit ÷ Shareholders' Equity

Or for Sino-i Technology:

25% = HK$377m ÷ HK$1.5b (Based on the trailing twelve months to December 2018.)

Most readers would understand what net profit is, but it’s worth explaining the concept of shareholders’ equity. It is the capital paid in by shareholders, plus any retained earnings. You can calculate shareholders' equity by subtracting the company's total liabilities from its total assets.

What Does Return On Equity Mean?

Return on Equity measures a company's profitability against the profit it has kept for the business (plus any capital injections). The 'return' is the yearly profit. That means that the higher the ROE, the more profitable the company is. So, all else being equal, a high ROE is better than a low one. That means it can be interesting to compare the ROE of different companies.

Does Sino-i Technology Have A Good Return On Equity?

By comparing a company's ROE with its industry average, we can get a quick measure of how good it is. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. Pleasingly, Sino-i Technology has a superior ROE than the average (12%) company in the IT industry.

That's clearly a positive. In my book, a high ROE almost always warrants a closer look. One data point to check is if insiders have bought shares recently.

How Does Debt Impact ROE?

Most companies need money -- from somewhere -- to grow their profits. The cash for investment can come from prior year profits (retained earnings), issuing new shares, or borrowing. In the first and second cases, the ROE will reflect this use of cash for investment in the business. In the latter case, the use of debt will improve the returns, but will not change the equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

Sino-i Technology's Debt And Its 25% ROE

One positive for shareholders is that Sino-i Technology does not have any net debt! Its impressive ROE suggests it is a high quality business, but it's even better to have achieved that without leverage. After all, with cash on the balance sheet, a company has a lot more optionality in good times and bad.

But It's Just One Metric

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. Companies that can achieve high returns on equity without too much debt are generally of good quality. All else being equal, a higher ROE is better.

Having said that, while ROE is a useful indicator of business quality, you'll have to look at a whole range of factors to determine the right price to buy a stock. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So I think it may be worth checking this freethis detailed graph of past earnings, revenue and cash flow .

Of course Sino-i Technology may not be the best stock to buy. So you may wish to see this free collection of other companies that have high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:250

Sino-i Technology

Sino-i Technology Limited, an investment holding company, provides enterprise cloud services to small and medium enterprises in Mainland China and Hong Kong.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor