- Hong Kong

- /

- Specialty Stores

- /

- SEHK:393

We Wouldn't Be Too Quick To Buy Glorious Sun Enterprises Limited (HKG:393) Before It Goes Ex-Dividend

Readers hoping to buy Glorious Sun Enterprises Limited (HKG:393) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is two business days before a company's record date in most cases, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company's books on the record date. Therefore, if you purchase Glorious Sun Enterprises' shares on or after the 21st of May, you won't be eligible to receive the dividend, when it is paid on the 10th of June.

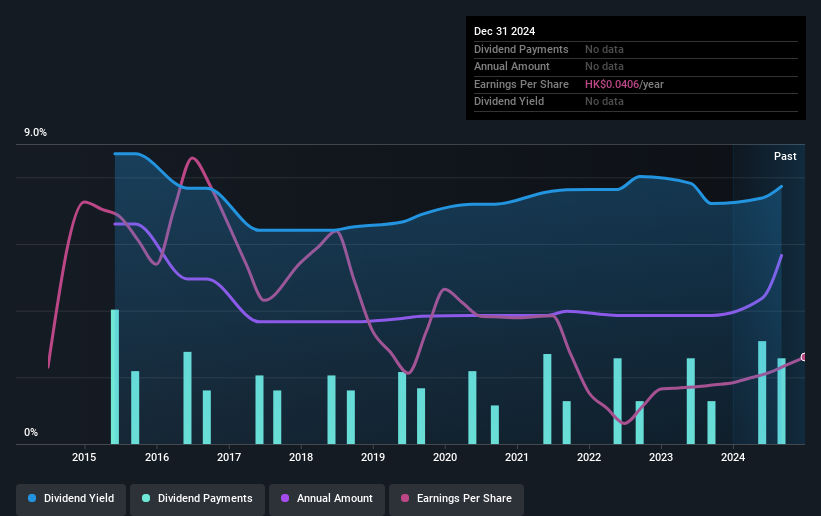

The company's upcoming dividend is HK$0.058 a share, following on from the last 12 months, when the company distributed a total of HK$0.098 per share to shareholders. Calculating the last year's worth of payments shows that Glorious Sun Enterprises has a trailing yield of 7.7% on the current share price of HK$1.28. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

Our free stock report includes 3 warning signs investors should be aware of before investing in Glorious Sun Enterprises. Read for free now.Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Glorious Sun Enterprises paid out a disturbingly high 241% of its profit as dividends last year, which makes us concerned there's something we don't fully understand in the business. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Thankfully its dividend payments took up just 47% of the free cash flow it generated, which is a comfortable payout ratio.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Glorious Sun Enterprises fortunately did generate enough cash to fund its dividend. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Very few companies are able to sustainably pay dividends larger than their reported earnings.

See our latest analysis for Glorious Sun Enterprises

Click here to see how much of its profit Glorious Sun Enterprises paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. With that in mind, we're discomforted by Glorious Sun Enterprises's 11% per annum decline in earnings in the past five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Glorious Sun Enterprises has seen its dividend decline 2.1% per annum on average over the past 10 years, which is not great to see. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

To Sum It Up

From a dividend perspective, should investors buy or avoid Glorious Sun Enterprises? It's never great to see earnings per share declining, especially when a company is paying out 241% of its profit as dividends, which we feel is uncomfortably high. However, the cash payout ratio was much lower - good news from a dividend perspective - which makes us wonder why there is such a mis-match between income and cashflow. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

So if you're still interested in Glorious Sun Enterprises despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. To help with this, we've discovered 3 warning signs for Glorious Sun Enterprises (1 can't be ignored!) that you ought to be aware of before buying the shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:393

Glorious Sun Enterprises

An investment holding company, engages in interior decoration and renovation business in Mainland China, Hong Kong, Australia, New Zealand, Canada, the United States, and internationally.

Flawless balance sheet with acceptable track record.

Market Insights

Community Narratives