Golden Eagle Retail Group's (HKG:3308) Returns Have Hit A Wall

If you're looking for a multi-bagger, there's a few things to keep an eye out for. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, the ROCE of Golden Eagle Retail Group (HKG:3308) looks decent, right now, so lets see what the trend of returns can tell us.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Golden Eagle Retail Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

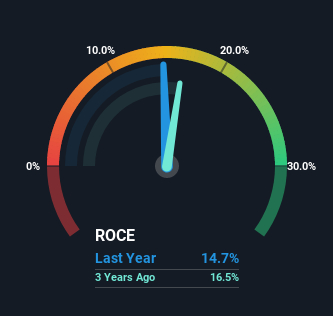

0.15 = CN¥2.1b ÷ (CN¥25b - CN¥11b) (Based on the trailing twelve months to June 2022).

Thus, Golden Eagle Retail Group has an ROCE of 15%. In absolute terms, that's a satisfactory return, but compared to the Multiline Retail industry average of 2.8% it's much better.

View our latest analysis for Golden Eagle Retail Group

In the above chart we have measured Golden Eagle Retail Group's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Golden Eagle Retail Group here for free.

What Can We Tell From Golden Eagle Retail Group's ROCE Trend?

While the returns on capital are good, they haven't moved much. The company has consistently earned 15% for the last five years, and the capital employed within the business has risen 43% in that time. 15% is a pretty standard return, and it provides some comfort knowing that Golden Eagle Retail Group has consistently earned this amount. Over long periods of time, returns like these might not be too exciting, but with consistency they can pay off in terms of share price returns.

On a side note, Golden Eagle Retail Group has done well to reduce current liabilities to 42% of total assets over the last five years. Effectively suppliers now fund less of the business, which can lower some elements of risk. We'd like to see this trend continue though because as it stands today, thats still a pretty high level.

The Key Takeaway

The main thing to remember is that Golden Eagle Retail Group has proven its ability to continually reinvest at respectable rates of return. Yet over the last five years the stock has declined 43%, so the decline might provide an opening. That's why we think it'd be worthwhile to look further into this stock given the fundamentals are appealing.

On a final note, we've found 1 warning sign for Golden Eagle Retail Group that we think you should be aware of.

While Golden Eagle Retail Group isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you're looking to trade Golden Eagle Retail Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3308

Golden Eagle Retail Group

Golden Eagle Retail Group Limited, an investment holding company, engages in development and operation of lifestyle center and department stores in the People’s Republic of China.

Undervalued with excellent balance sheet.

Market Insights

Community Narratives