Advertisement

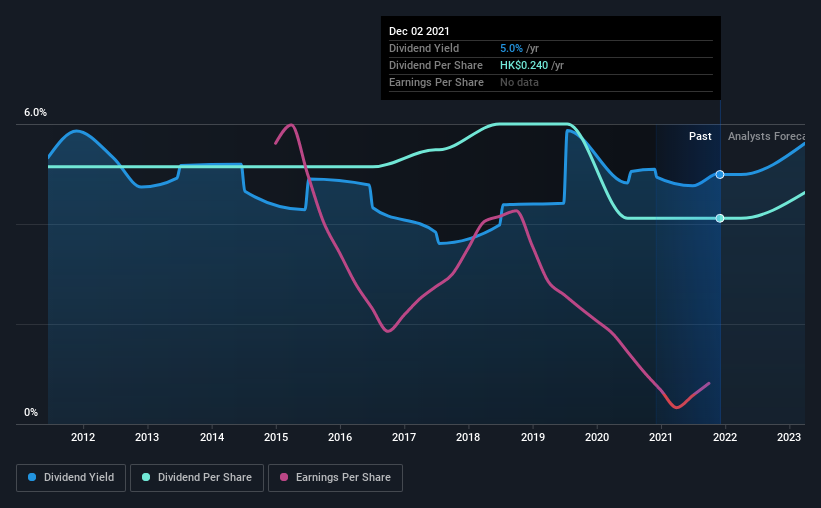

The board of Tai Cheung Holdings Limited (HKG:88) has announced that it will pay a dividend on the 4th of January, with investors receiving HK$0.12 per share. This payment means that the dividend yield will be 5.0%, which is around the industry average.

Check out our latest analysis for Tai Cheung Holdings

Tai Cheung Holdings' Payment Has Solid Earnings Coverage

Solid dividend yields are great, but they only really help us if the payment is sustainable. Based on the last payment, earnings were actually smaller than the dividend, and the company was actually spending more cash than it was making. This high of a dividend payment could start to put pressure on the balance sheet in the future.

According to analysts, EPS should be several times higher next year. Assuming the dividend continues along recent trends, we estimate that the payout ratio could reach 39%, which is in a comfortable range for us.

Dividend Volatility

The company's dividend history has been marked by instability, with at least 1 cut in the last 10 years. The dividend has gone from HK$0.30 in 2011 to the most recent annual payment of HK$0.24. This works out to be a decline of approximately 2.2% per year over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Dividend Growth Potential Is Shaky

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Tai Cheung Holdings' earnings per share has shrunk at 30% a year over the past five years. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

We're Not Big Fans Of Tai Cheung Holdings' Dividend

In summary, while it is good to see that the dividend hasn't been cut, we think that at current levels the payment isn't particularly sustainable. The company seems to be stretching itself a bit to make such big payments, but it doesn't appear they can be consistent over time. Overall, the dividend is not reliable enough to make this a good income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 2 warning signs for Tai Cheung Holdings that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our curated list of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Tai Cheung Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:88

Tai Cheung Holdings

An investment holding company, engages in property investment, development, and management businesses in Hong Kong and the United States.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor