Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:488

How Should Investors Feel About Lai Sun Development's (HKG:488) CEO Remuneration?

Julius Lau became the CEO of Lai Sun Development Company Limited (HKG:488) in 2005, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Lai Sun Development.

Check out our latest analysis for Lai Sun Development

Comparing Lai Sun Development Company Limited's CEO Compensation With the industry

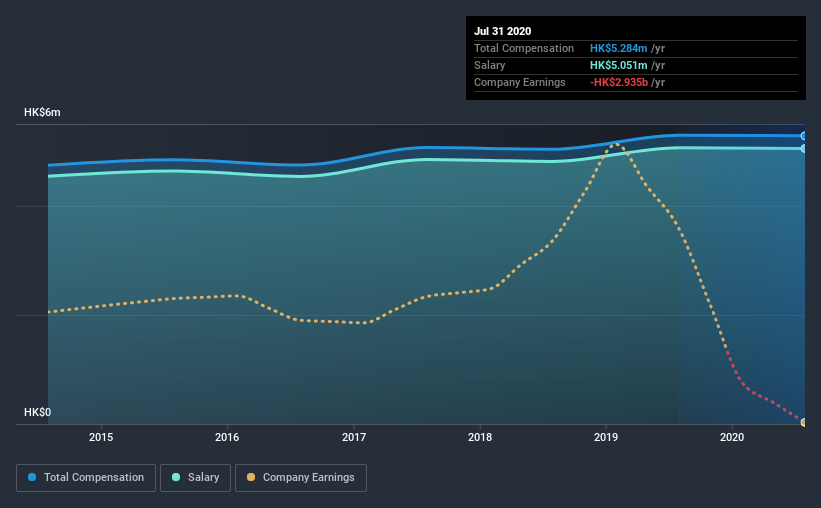

At the time of writing, our data shows that Lai Sun Development Company Limited has a market capitalization of HK$4.3b, and reported total annual CEO compensation of HK$5.3m for the year to July 2020. This means that the compensation hasn't changed much from last year. We note that the salary portion, which stands at HK$5.05m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations ranging from HK$1.6b to HK$6.2b, the reported median CEO total compensation was HK$3.8m. Accordingly, our analysis reveals that Lai Sun Development Company Limited pays Julius Lau north of the industry median. Furthermore, Julius Lau directly owns HK$1.8m worth of shares in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | HK$5.1m | HK$5.1m | 96% |

| Other | HK$233k | HK$230k | 4% |

| Total Compensation | HK$5.3m | HK$5.3m | 100% |

On an industry level, around 70% of total compensation represents salary and 30% is other remuneration. Lai Sun Development is focused on going down a more traditional approach and is paying a higher portion of compensation through salary, as compared to non-salary benefits. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Lai Sun Development Company Limited's Growth

Lai Sun Development Company Limited has reduced its earnings per share by 42% a year over the last three years. Its revenue is down 20% over the previous year.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Lai Sun Development Company Limited Been A Good Investment?

Since shareholders would have lost about 47% over three years, some Lai Sun Development Company Limited investors would surely be feeling negative emotions. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Julius receives almost all of their compensation through a salary. As previously discussed, Julius is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. Disappointingly, share price gains over the last three years have failed to materialize. What's equally worrying is that the company isn't growing by our analysis. Understandably, the company's shareholders might have some questions about the CEO's remuneration, given the disappointing performance.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 1 warning sign for Lai Sun Development that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you’re looking to trade Lai Sun Development, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:488

Lai Sun Development

Invests in, develops, leases, and sells real estate properties in Hong Kong, Mainland China, Macau, the United Kingdom, Vietnam, and internationally.

Good value with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.7% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.11k18.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

lexdrew1 on Corning ·

Corning's Revenue Will Climb by 12.73% in Just Five Years

Fair Value:US$108.6313.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

lexdrew1 on GE Vernova ·

GE Vernova revenue will grow by 13% with a future PE of 64.7x

Fair Value:US$824.5712.3% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.7% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8684.3% undervalued

76 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative