- Hong Kong

- /

- Real Estate

- /

- SEHK:3688

Shareholders in Top Spring International Holdings (HKG:3688) have lost 58%, as stock drops 13% this past week

Generally speaking long term investing is the way to go. But along the way some stocks are going to perform badly. For example, after five long years the Top Spring International Holdings Limited (HKG:3688) share price is a whole 62% lower. That is extremely sub-optimal, to say the least. And some of the more recent buyers are probably worried, too, with the stock falling 30% in the last year. Shareholders have had an even rougher run lately, with the share price down 29% in the last 90 days.

With the stock having lost 13% in the past week, it's worth taking a look at business performance and seeing if there's any red flags.

Top Spring International Holdings isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

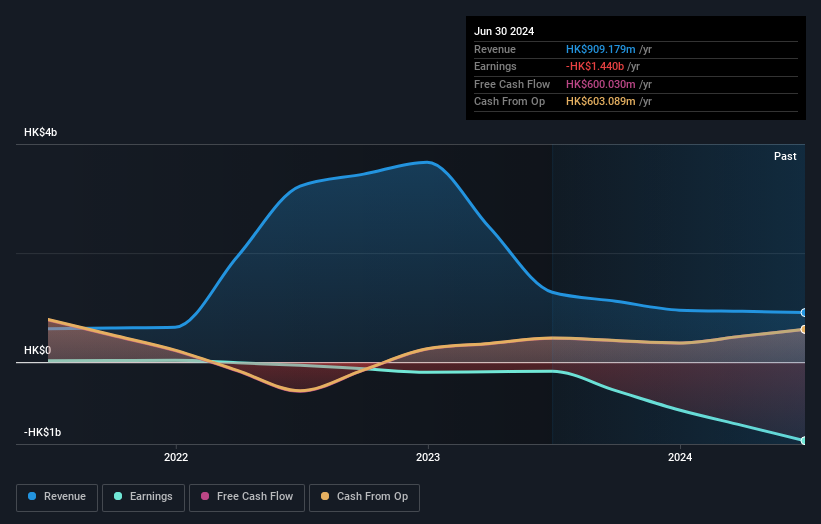

In the last half decade, Top Spring International Holdings saw its revenue increase by 20% per year. That's better than most loss-making companies. In contrast, the share price is has averaged a loss of 10% per year - that's quite disappointing. It's safe to say investor expectations are more grounded now. If you think the company can keep up its revenue growth, you'd have to consider the possibility that there's an opportunity here.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Take a more thorough look at Top Spring International Holdings' financial health with this free report on its balance sheet.

What About The Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Top Spring International Holdings' total shareholder return (TSR) and its share price return. The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Dividends have been really beneficial for Top Spring International Holdings shareholders, and that cash payout explains why its total shareholder loss of 58%, over the last 5 years, isn't as bad as the share price return.

A Different Perspective

While the broader market gained around 35% in the last year, Top Spring International Holdings shareholders lost 30%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 10% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. It's always interesting to track share price performance over the longer term. But to understand Top Spring International Holdings better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with Top Spring International Holdings (at least 2 which make us uncomfortable) , and understanding them should be part of your investment process.

Of course Top Spring International Holdings may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Top Spring International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3688

Top Spring International Holdings

An investment holding company, operates as a real estate property developer in the People's Republic of China.

Good value slight.

Similar Companies

Market Insights

Community Narratives