Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1997

Does Wharf Real Estate Investment's New Hotel Services Deal Clarify or Complicate Its Core Strategy (SEHK:1997)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Wharf Real Estate Investment Company (WREIC) announced that on 28 November 2025 it entered into a new three-year Master Hotel Services Agreement with Wharf, covering management, marketing, technical, procurement, training, financial and reservation services for its hotels and serviced apartments from 1 January 2026 to 31 December 2028.

- This refreshed framework for continuing connected transactions helps formalise long-term service arrangements within the wider Wharf group, providing clearer visibility over future hotel-related service flows and governance for both parties.

- Next, we will examine how locking in long-term hotel management and related services could influence WREIC's investment narrative and earnings profile.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Wharf Real Estate Investment Investment Narrative Recap

To own Wharf Real Estate Investment, you need to believe in the resilience of its prime Hong Kong retail, office and hospitality assets despite recent earnings volatility and sector headwinds. The new Master Hotel Services Agreement mainly tidies up group hotel arrangements and does not, on its own, change the near term focus on stabilising rental income or the key risk from structurally weaker Hong Kong retail demand.

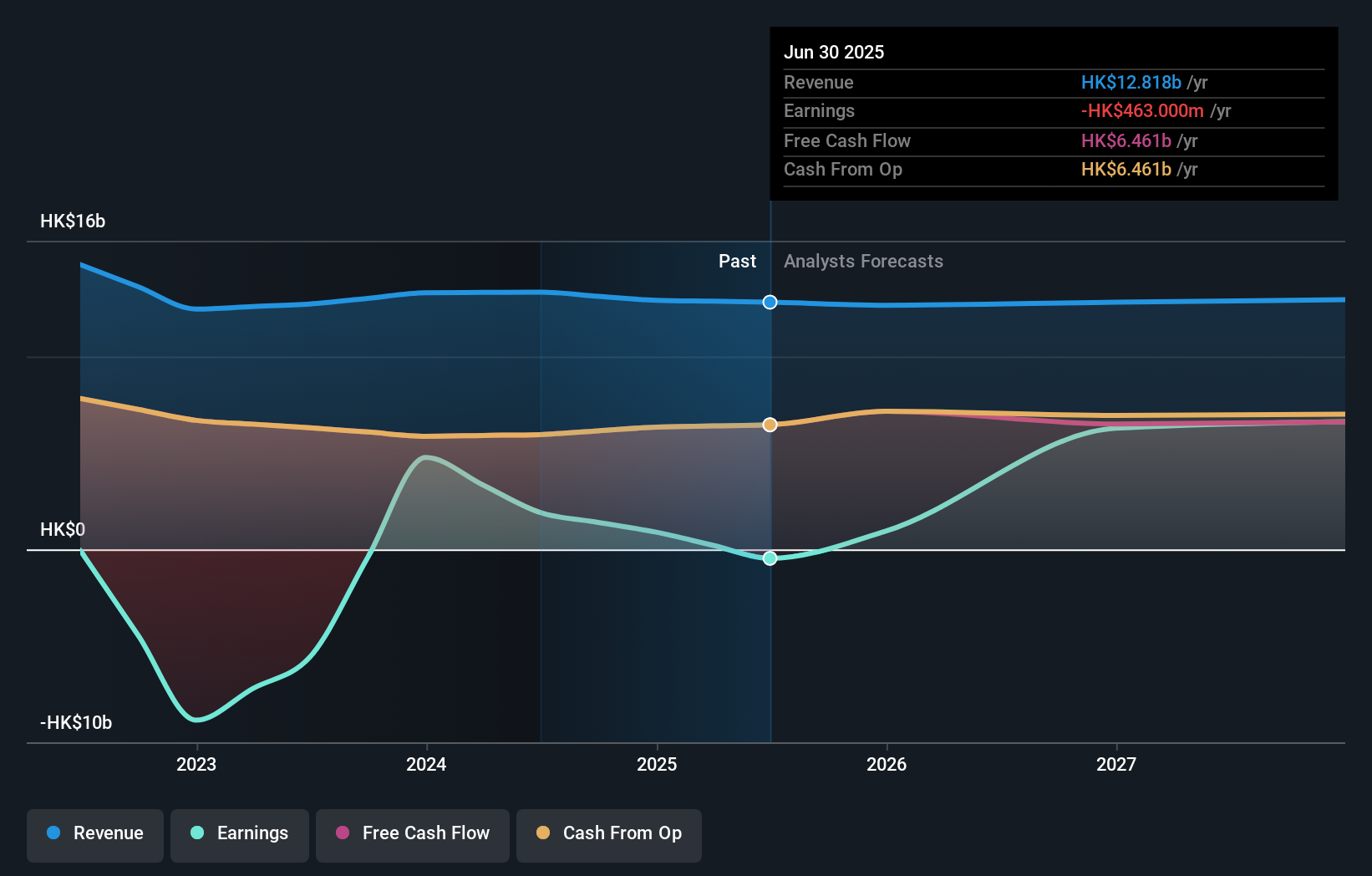

The most relevant recent announcement in this context is the H1 2025 results, where WREIC reported revenue of HK$6,407 million and a net loss of HK$2,406 million. Against this backdrop, formalising hotel services with Wharf may help operational execution, but investors are still watching how recurring rental performance and any ongoing negative rental reversions flow through to future earnings.

Yet investors should be aware that if Hong Kong retail rents settle at far lower levels for longer, then ...

Read the full narrative on Wharf Real Estate Investment (it's free!)

Wharf Real Estate Investment's narrative projects HK$13.5 billion revenue and HK$7.2 billion earnings by 2028. This requires 1.8% yearly revenue growth and about HK$7.7 billion earnings increase from HK$-463.0 million today.

Uncover how Wharf Real Estate Investment's forecasts yield a HK$25.92 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Only one Simply Wall St Community member has submitted a fair value estimate, clustering at HK$25.92 per share. You can weigh that single view against the risk of prolonged structural weakness in Hong Kong retail that could pressure WREIC’s rental income and margins over time.

Explore another fair value estimate on Wharf Real Estate Investment - why the stock might be worth just HK$25.92!

Build Your Own Wharf Real Estate Investment Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wharf Real Estate Investment research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wharf Real Estate Investment research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wharf Real Estate Investment's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wharf Real Estate Investment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1997

Wharf Real Estate Investment

An investment holding company, develops, owns, and operates properties and hotels in Hong Kong, Mainland China, and Singapore.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

15 followersusers have followed this narrative

5 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.563.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

948 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative