Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1396

Guangdong - Hong Kong Greater Bay Area Holdings Limited's (HKG:1396) 29% Dip Still Leaving Some Shareholders Feeling Restless Over Its P/SRatio

The Guangdong - Hong Kong Greater Bay Area Holdings Limited (HKG:1396) share price has softened a substantial 29% over the previous 30 days, handing back much of the gains the stock has made lately. Regardless, last month's decline is barely a blip on the stock's price chart as it has gained a monstrous 338% in the last year.

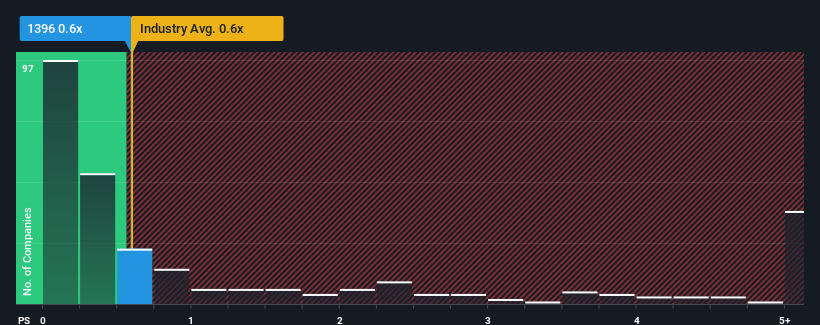

Although its price has dipped substantially, there still wouldn't be many who think Guangdong - Hong Kong Greater Bay Area Holdings' price-to-sales (or "P/S") ratio of 0.6x is worth a mention when it essentially matches the median P/S in Hong Kong's Real Estate industry. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Our free stock report includes 3 warning signs investors should be aware of before investing in Guangdong - Hong Kong Greater Bay Area Holdings. Read for free now.See our latest analysis for Guangdong - Hong Kong Greater Bay Area Holdings

What Does Guangdong - Hong Kong Greater Bay Area Holdings' P/S Mean For Shareholders?

As an illustration, revenue has deteriorated at Guangdong - Hong Kong Greater Bay Area Holdings over the last year, which is not ideal at all. It might be that many expect the company to put the disappointing revenue performance behind them over the coming period, which has kept the P/S from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Guangdong - Hong Kong Greater Bay Area Holdings' earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Guangdong - Hong Kong Greater Bay Area Holdings' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 26% decrease to the company's top line. As a result, revenue from three years ago have also fallen 53% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to grow by 4.7% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this information, we find it concerning that Guangdong - Hong Kong Greater Bay Area Holdings is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Bottom Line On Guangdong - Hong Kong Greater Bay Area Holdings' P/S

Following Guangdong - Hong Kong Greater Bay Area Holdings' share price tumble, its P/S is just clinging on to the industry median P/S. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look at Guangdong - Hong Kong Greater Bay Area Holdings revealed its shrinking revenues over the medium-term haven't impacted the P/S as much as we anticipated, given the industry is set to grow. Even though it matches the industry, we're uncomfortable with the current P/S ratio, as this dismal revenue performance is unlikely to support a more positive sentiment for long. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

Plus, you should also learn about these 3 warning signs we've spotted with Guangdong - Hong Kong Greater Bay Area Holdings.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1396

Guangdong - Hong Kong Greater Bay Area Holdings

Develops, operates, and sells residential properties, and commercial trade and logistics centers in Mainland China.

Excellent balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor