- Hong Kong

- /

- Real Estate

- /

- SEHK:1821

SEHK Growth Companies With High Insider Ownership

Reviewed by Simply Wall St

In recent weeks, the Hong Kong market has faced challenges similar to global counterparts, with economic uncertainties and mixed corporate earnings influencing investor sentiment. Despite these headwinds, growth companies with high insider ownership often present compelling opportunities due to their alignment of interests between management and shareholders. When evaluating stocks in today's volatile environment, it's crucial to consider those where insiders have substantial stakes as this can indicate confidence in the company's long-term prospects.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| Laopu Gold (SEHK:6181) | 36.4% | 34.7% |

| Akeso (SEHK:9926) | 20.5% | 55.0% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Fenbi (SEHK:2469) | 31.2% | 22.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.7% | 69.8% |

| Adicon Holdings (SEHK:9860) | 22.4% | 31.2% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 14.6% | 78.9% |

| DPC Dash (SEHK:1405) | 38.2% | 104.2% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 109.2% |

| Beijing Airdoc Technology (SEHK:2251) | 28.6% | 93.4% |

Let's take a closer look at a couple of our picks from the screened companies.

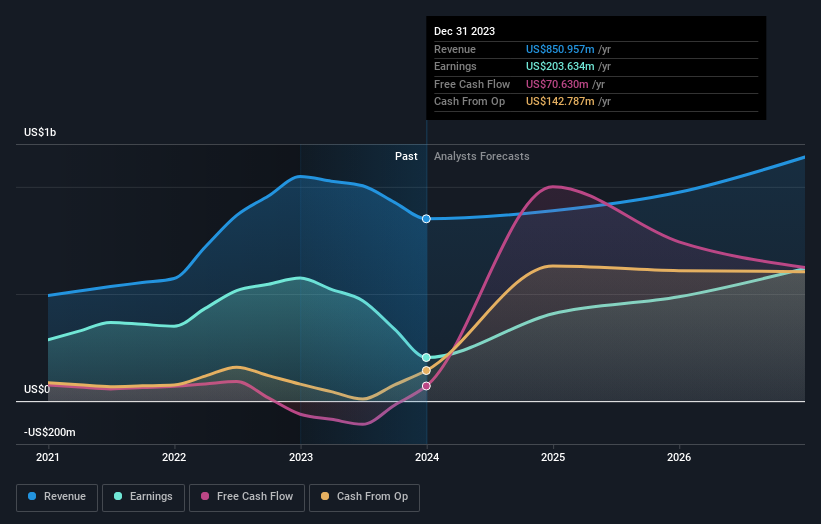

ESR Group (SEHK:1821)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ESR Group Limited, with a market cap of HK$52.64 billion, operates in logistics real estate development, leasing, and management across Hong Kong, China, Japan, South Korea, Australia, New Zealand, Southeast Asia, India, Europe and other international markets.

Operations: The company's revenue segments include Fund Management ($627.98 million) and New Economy Development ($113.33 million).

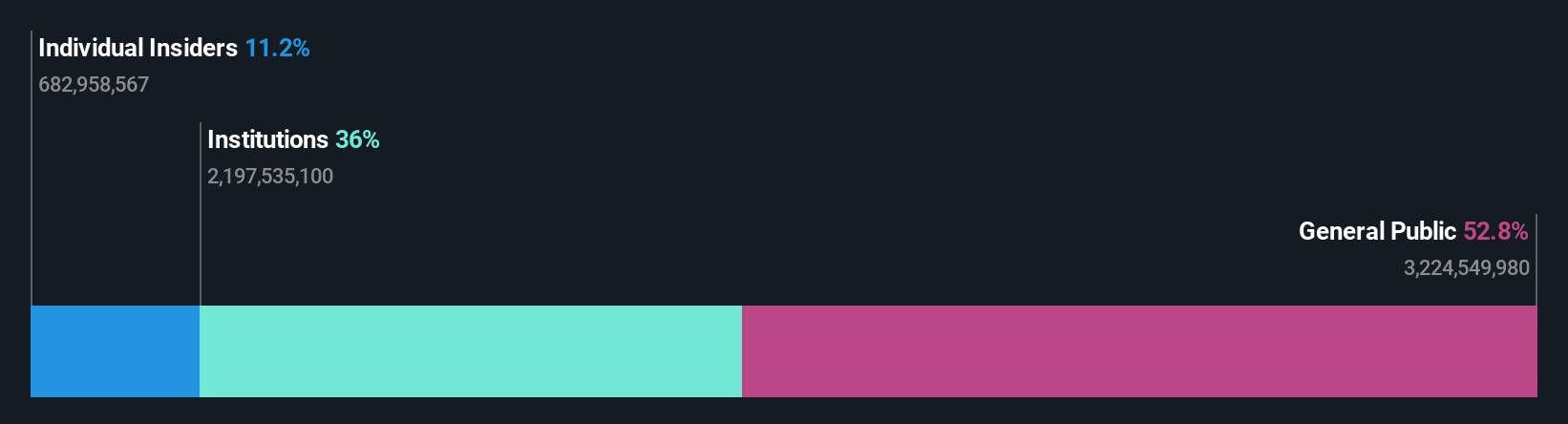

Insider Ownership: 13%

ESR Group, a growth company with high insider ownership in Hong Kong, recently announced a significant leadership change with Mr. Brett Harold Krause stepping in as interim chairman following Mr. Jeffrey Perlman's departure to Warburg Pincus. Despite an expected net loss of US$210 million for H1 2024 due to non-cash asset revaluations and market conditions, ESR's revenue growth is forecasted at 16.4% annually, outpacing the broader Hong Kong market's 7.3%.

- Click here to discover the nuances of ESR Group with our detailed analytical future growth report.

- Our valuation report unveils the possibility ESR Group's shares may be trading at a premium.

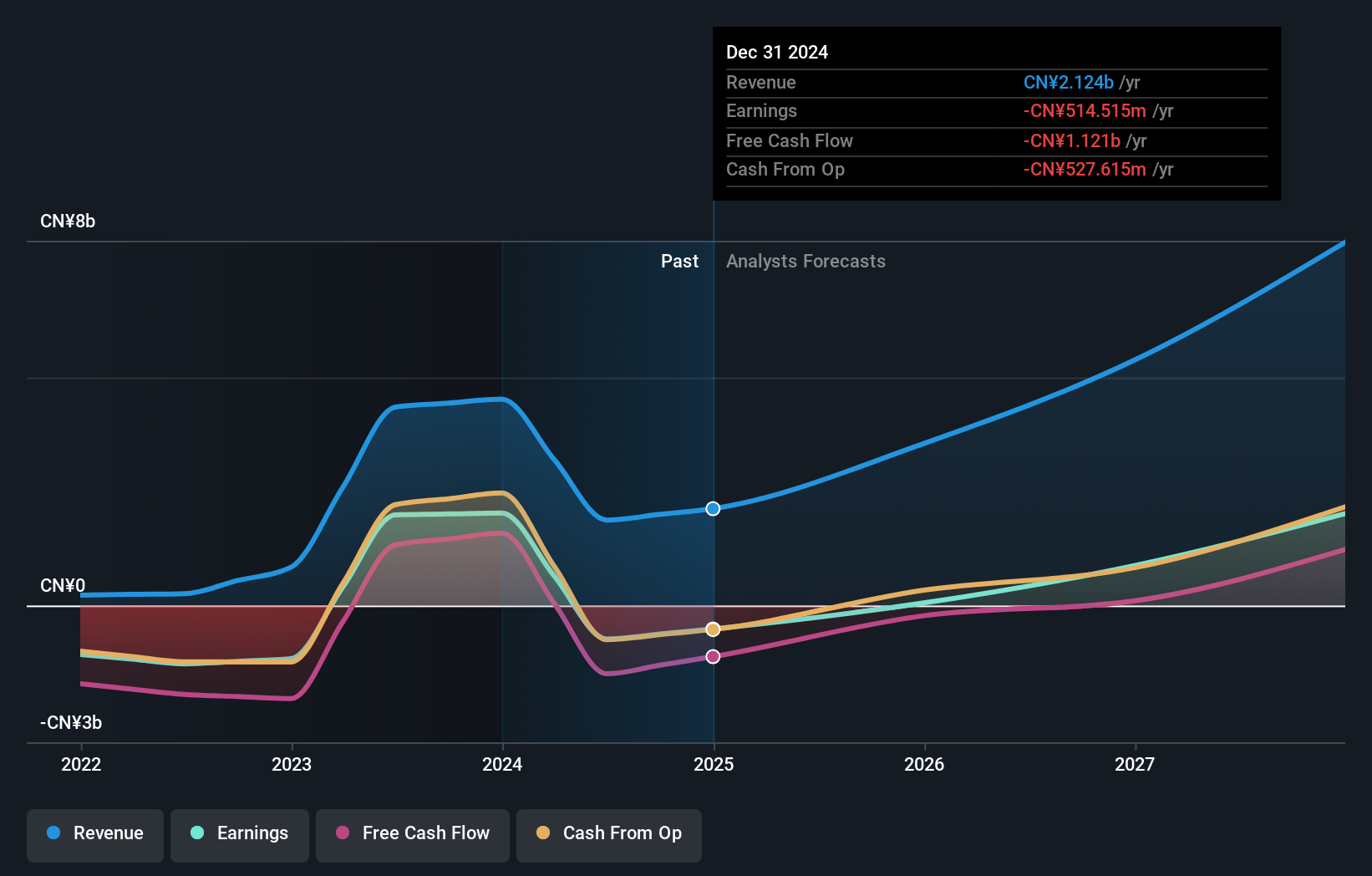

Meituan (SEHK:3690)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Meituan operates as a technology retail company in the People’s Republic of China, with a market cap of approximately HK$724.49 billion.

Operations: The company's revenue segments include CN¥228.13 billion from Core Local Commerce and CN¥77.56 billion from New Initiatives.

Insider Ownership: 11.6%

Meituan's recent earnings report showed substantial growth, with sales reaching CNY 155.53 billion and net income doubling to CNY 16.72 billion for the first half of 2024. The company also announced a share repurchase program worth up to $1 billion, indicating confidence in its future prospects. Despite no substantial insider buying recently, Meituan's earnings are forecasted to grow significantly at 25.8% annually, outpacing the Hong Kong market average of 11.7%.

- Click to explore a detailed breakdown of our findings in Meituan's earnings growth report.

- Our expertly prepared valuation report Meituan implies its share price may be lower than expected.

Akeso (SEHK:9926)

Simply Wall St Growth Rating: ★★★★★★

Overview: Akeso, Inc., a biopharmaceutical company with a market cap of HK$48.31 billion, researches, develops, manufactures, and commercializes antibody drugs.

Operations: Revenue from the research, development, production, and sale of biopharmaceutical products amounts to CN¥1.87 billion.

Insider Ownership: 20.5%

Akeso, a growth company with high insider ownership in Hong Kong, is forecasted to achieve significant revenue growth of 32.7% annually and become profitable within three years. Despite recent dilution and a half-year net loss of CNY 238.59 million, the company's innovative drug pipeline shows promise. Ivonescimab's recent approvals and ongoing clinical trials highlight its potential impact on cancer treatment, positioning Akeso for substantial future growth.

- Delve into the full analysis future growth report here for a deeper understanding of Akeso.

- According our valuation report, there's an indication that Akeso's share price might be on the expensive side.

Next Steps

- Explore the 47 names from our Fast Growing SEHK Companies With High Insider Ownership screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if ESR Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1821

ESR Group

Engages in the logistics real estate development, leasing, and management activities in Hong Kong, China, Japan, South Korea, Australia, New Zealand, Southeast Asia, India, Europe, and internationally.

Reasonable growth potential and slightly overvalued.