Advertisement

Undervalued Small Caps With Insider Activity To Watch In January 2025

Simply Wall St

Reviewed by Simply Wall St

As we enter January 2025, global markets are grappling with a mix of economic signals, including a resilient U.S. labor market and ongoing inflation concerns that have sent small-cap stocks into correction territory, as evidenced by the Russell 2000 Index's recent dip. Amid this backdrop of uncertainty and fluctuating investor sentiment, identifying promising small-cap opportunities requires a keen eye on factors such as value resilience and insider activity, which can provide insights into potential growth despite broader market challenges.

Top 10 Undervalued Small Caps With Insider Buying

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| 4imprint Group | 15.9x | 1.3x | 38.51% | ★★★★★☆ |

| Paradeep Phosphates | 25.5x | 0.8x | 25.33% | ★★★★★☆ |

| Maharashtra Seamless | 10.0x | 1.7x | 36.48% | ★★★★★☆ |

| Speedy Hire | NA | 0.3x | 35.04% | ★★★★★☆ |

| Robert Walters | 34.5x | 0.2x | 30.71% | ★★★★☆☆ |

| ABG Sundal Collier Holding | 12.6x | 2.1x | 39.87% | ★★★★☆☆ |

| Logistri Fastighets | 12.3x | 8.7x | 42.44% | ★★★★☆☆ |

| Digital Mediatama Maxima | NA | 1.2x | 21.10% | ★★★★☆☆ |

| Mark Dynamics Indonesia | 13.0x | 4.2x | 6.86% | ★★★☆☆☆ |

| THG | NA | 0.3x | -519.29% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

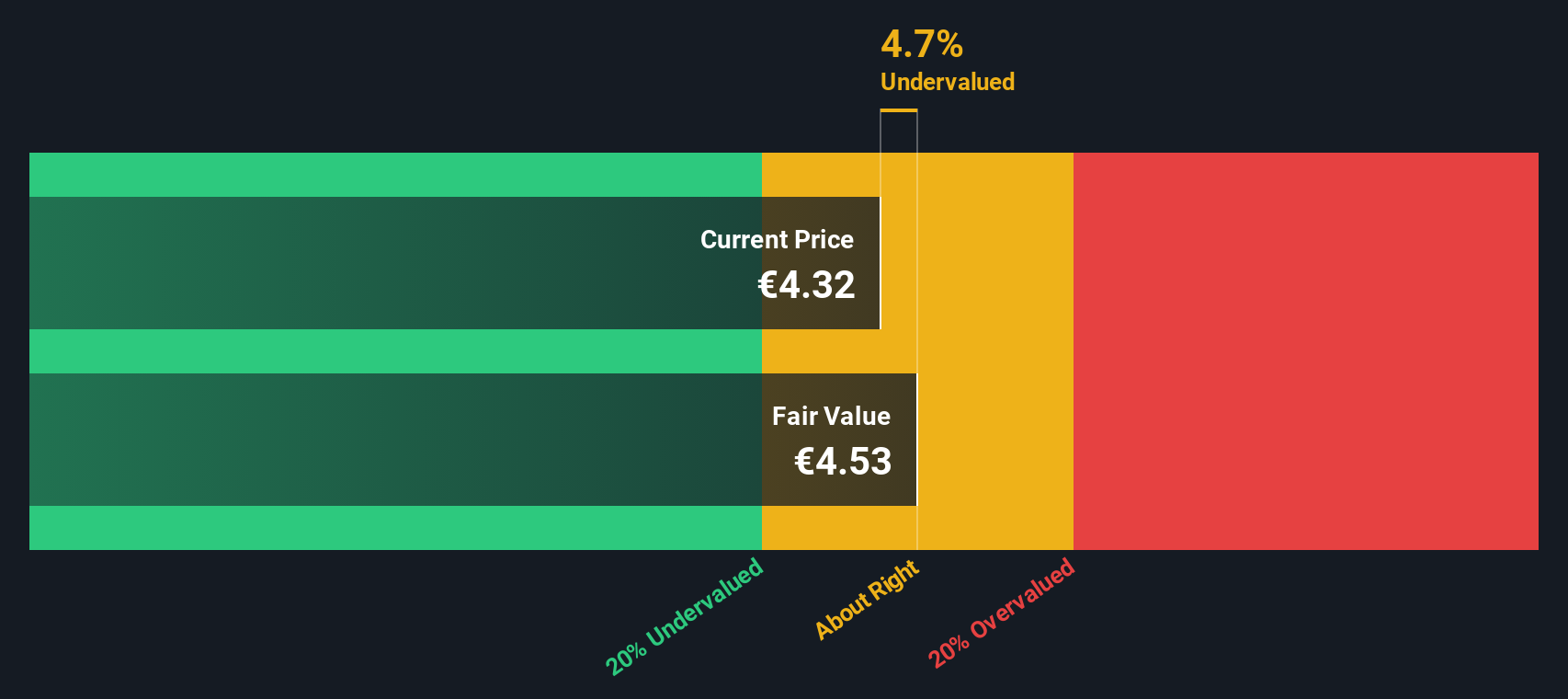

Ariston Holding (BIT:ARIS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Ariston Holding specializes in the production and distribution of thermal comfort solutions, burners, and components, with a market capitalization of €3.89 billion.

Operations: Thermal Comfort is the primary revenue stream, generating €2.67 billion, while Burners and Components contribute €92 million and €81.8 million respectively. The gross profit margin reached 40.52% as of December 2023, reflecting a trend of increasing profitability over recent periods despite fluctuations in net income margin.

PE: 19.5x

Ariston Holding, a company characterized by its smaller market size, has recently seen insider confidence through share purchases by Paolo Merloni, who acquired 173,770 shares for €623,834. Their funding relies entirely on external borrowing rather than customer deposits. Despite a decrease in profit margins from 6.2% to 2%, earnings are projected to grow annually by 49%. This potential growth offers intriguing prospects amidst their high debt levels and current financial challenges.

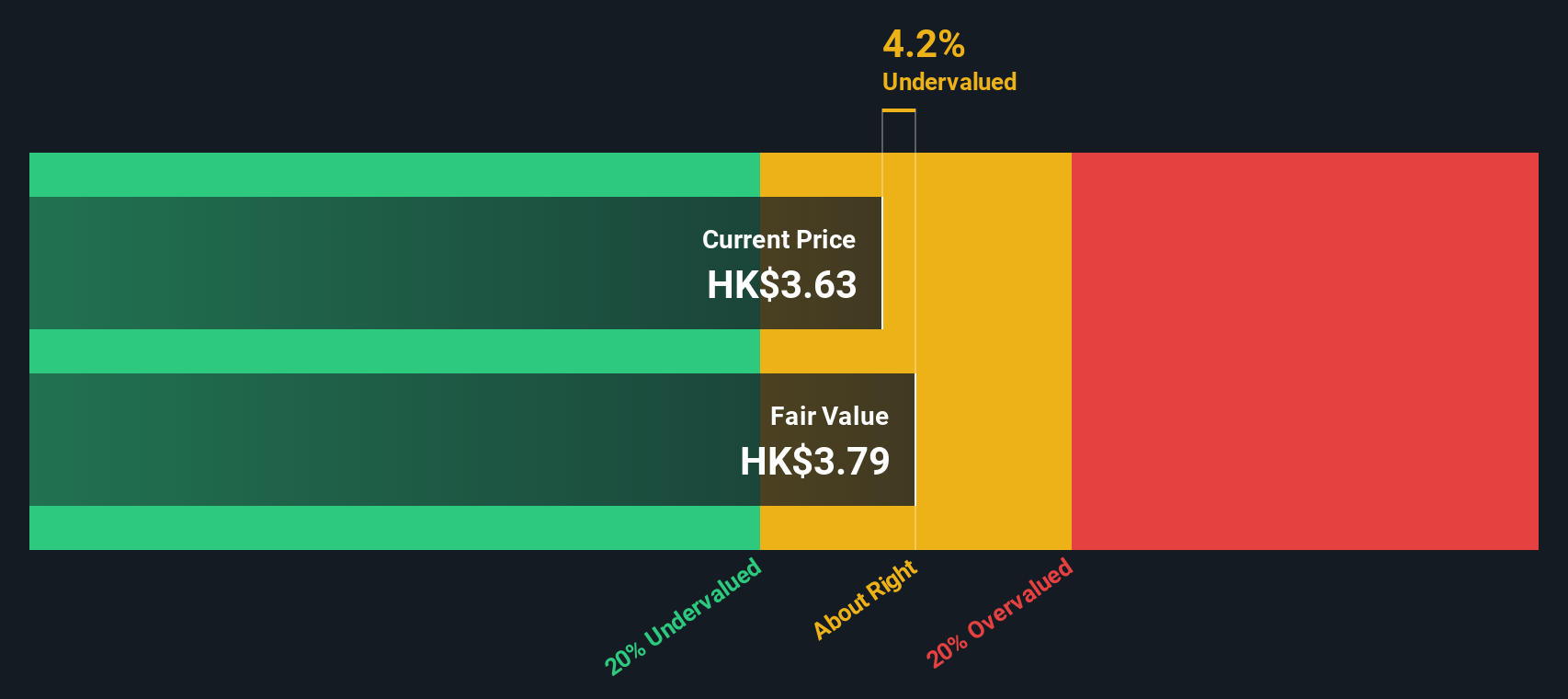

Eagle Nice (International) Holdings (SEHK:2368)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Eagle Nice (International) Holdings is engaged in the manufacturing and trading of sportswear and apparel, with a market capitalization of HK$1.45 billion.

Operations: The company generates revenue primarily from the Chinese Mainland, contributing significantly to its total income. Over recent periods, the net profit margin has shown a declining trend, reaching 4.80% in the latest quarter. The company's cost structure is largely driven by COGS and operating expenses, which have impacted profitability metrics.

PE: 10.9x

Eagle Nice, known for its apparel manufacturing, presents a mixed picture in the small-cap space. Recent insider confidence is evident with Yongbiao Huang purchasing 160,000 shares worth HK$727,936 between January and November 2024. However, profit margins have dipped to 4.8% from last year's 7%, and debt remains uncovered by operating cash flow due to reliance on external borrowing. Despite sales growth to HK$2.98 billion for the half-year ending September 2024, net income fell to HK$183 million from HK$229 million year-over-year.

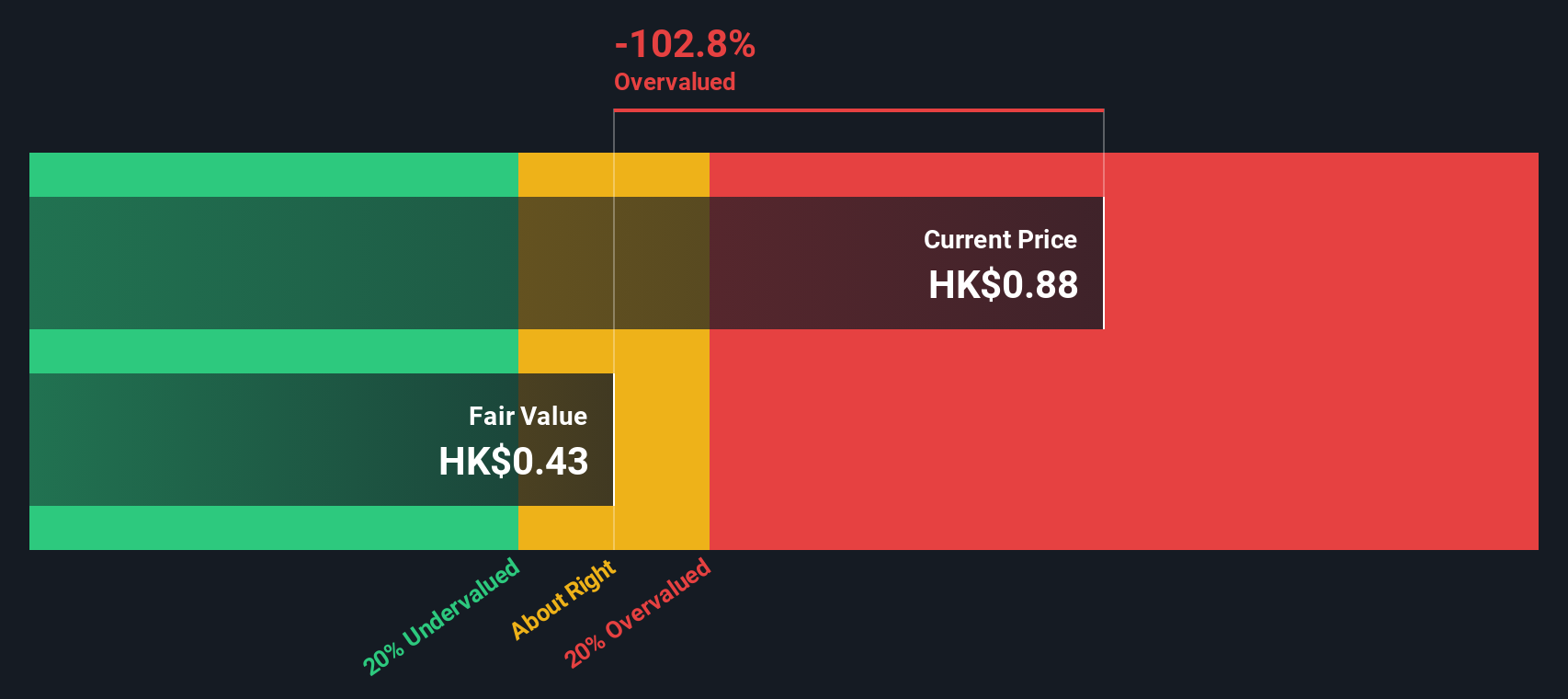

CK Life Sciences Int'l. (Holdings) (SEHK:775)

Simply Wall St Value Rating: ★★★★☆☆

Overview: CK Life Sciences Int'l. (Holdings) operates in agriculture-related sectors and other segments, with a market capitalization of HK$3.36 billion.

Operations: The company primarily generates revenue from its agriculture-related segment. Over the periods, the gross profit margin has shown varying trends, reaching 30.43% in mid-2024. Operating expenses are a significant component of costs, consistently impacting net income margins, which have recently turned negative at -0.35% as of June 2024.

PE: -224.0x

CK Life Sciences, a relatively small player, is catching attention due to insider confidence. Over the past year, their VP and CEO purchased 2.1 million shares valued at approximately HK$969K, marking a staggering 1253% increase in their holdings. Despite earnings declining by 28% annually over five years and reliance on external borrowing for funding, this insider activity suggests potential value recognition within the company. However, interest payments remain poorly covered by earnings.

Turning Ideas Into Actions

- Get an in-depth perspective on all 183 Undervalued Small Caps With Insider Buying by using our screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:775

CK Life Sciences Int'l. (Holdings)

An investment holding company, researches, develops, manufactures, commercializes, and sells health and agriculture-related products in the Asia Pacific and North America.

Low and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor