In recent weeks, Asian markets have been navigating a complex landscape marked by global trade tensions and inflationary pressures, which have contributed to fluctuating investor sentiment. Amid these challenges, small-cap stocks in Asia present intriguing opportunities for investors seeking growth potential at attractive valuations. Identifying promising small caps involves looking for companies with strong fundamentals and insider buying activity, which can signal confidence in the company's future prospects even amidst broader economic uncertainties.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.7x | 1.1x | 36.89% | ★★★★★★ |

| Atturra | 27.5x | 1.1x | 39.97% | ★★★★★☆ |

| Dicker Data | 19.3x | 0.7x | -41.10% | ★★★★☆☆ |

| Puregold Price Club | 9.0x | 0.4x | 15.84% | ★★★★☆☆ |

| Hansen Technologies | 285.2x | 2.8x | 27.68% | ★★★★☆☆ |

| Sing Investments & Finance | 7.4x | 3.8x | 35.03% | ★★★★☆☆ |

| Viva Energy Group | NA | 0.1x | 19.20% | ★★★★☆☆ |

| Fenix Resources | 15.7x | 0.8x | 14.79% | ★★★☆☆☆ |

| Integral Diagnostics | 151.6x | 1.7x | 41.91% | ★★★☆☆☆ |

| Manawa Energy | NA | 2.7x | 36.49% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

Dicker Data (ASX:DDR)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Dicker Data is a wholesale distributor specializing in computer peripherals, with a market capitalization of A$1.94 billion.

Operations: The company's revenue primarily stems from wholesale computer peripherals, with a gross profit margin reaching 14.55% as of March 2025. Cost of goods sold (COGS) significantly influences the financials, while operating expenses and non-operating expenses also play vital roles in determining net income.

PE: 19.3x

Dicker Data, a prominent player in the tech distribution sector, recently announced a strategic partnership with CrowdStrike to enhance its cybersecurity offerings across Australia and New Zealand. Despite high debt levels due to reliance on external borrowing, Dicker Data's earnings are projected to grow by 9.38% annually. Insider confidence is evident as they increased their stake between January and March 2025. With A$2.28 billion in revenue for 2024, the company continues to expand its market footprint amidst rising demand for advanced cybersecurity solutions.

- Dive into the specifics of Dicker Data here with our thorough valuation report.

Assess Dicker Data's past performance with our detailed historical performance reports.

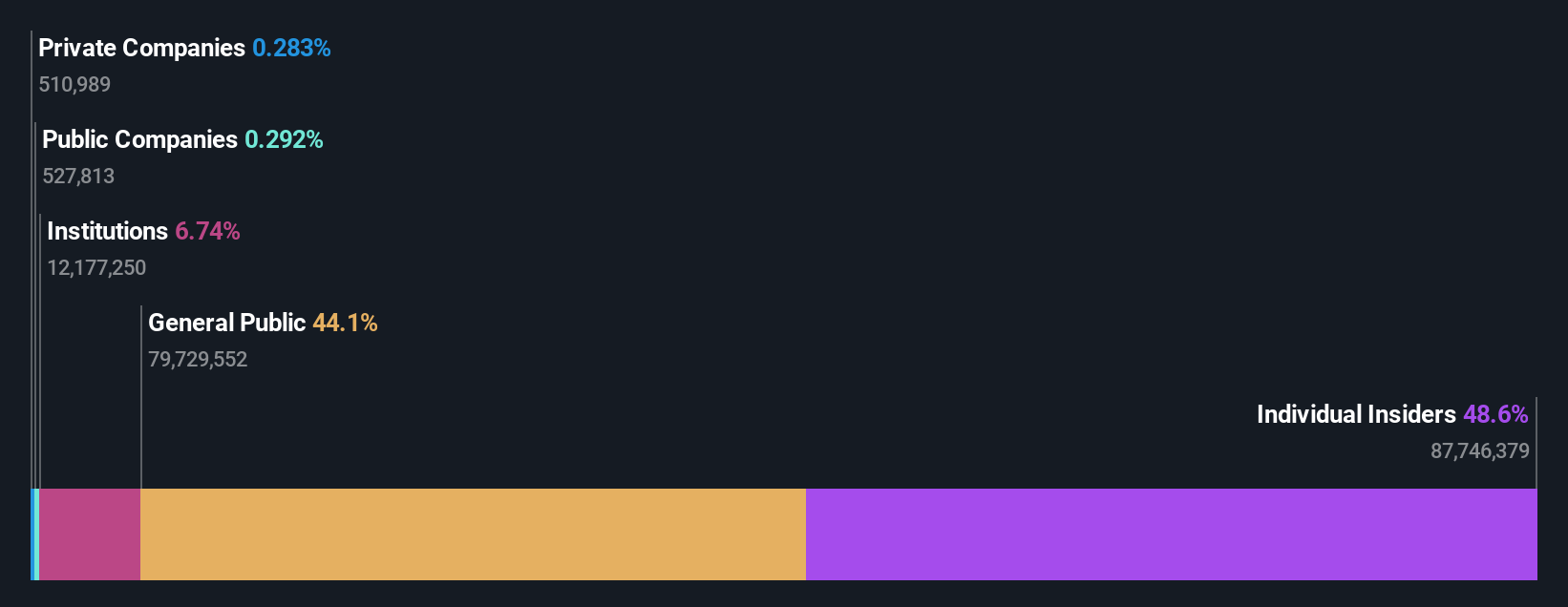

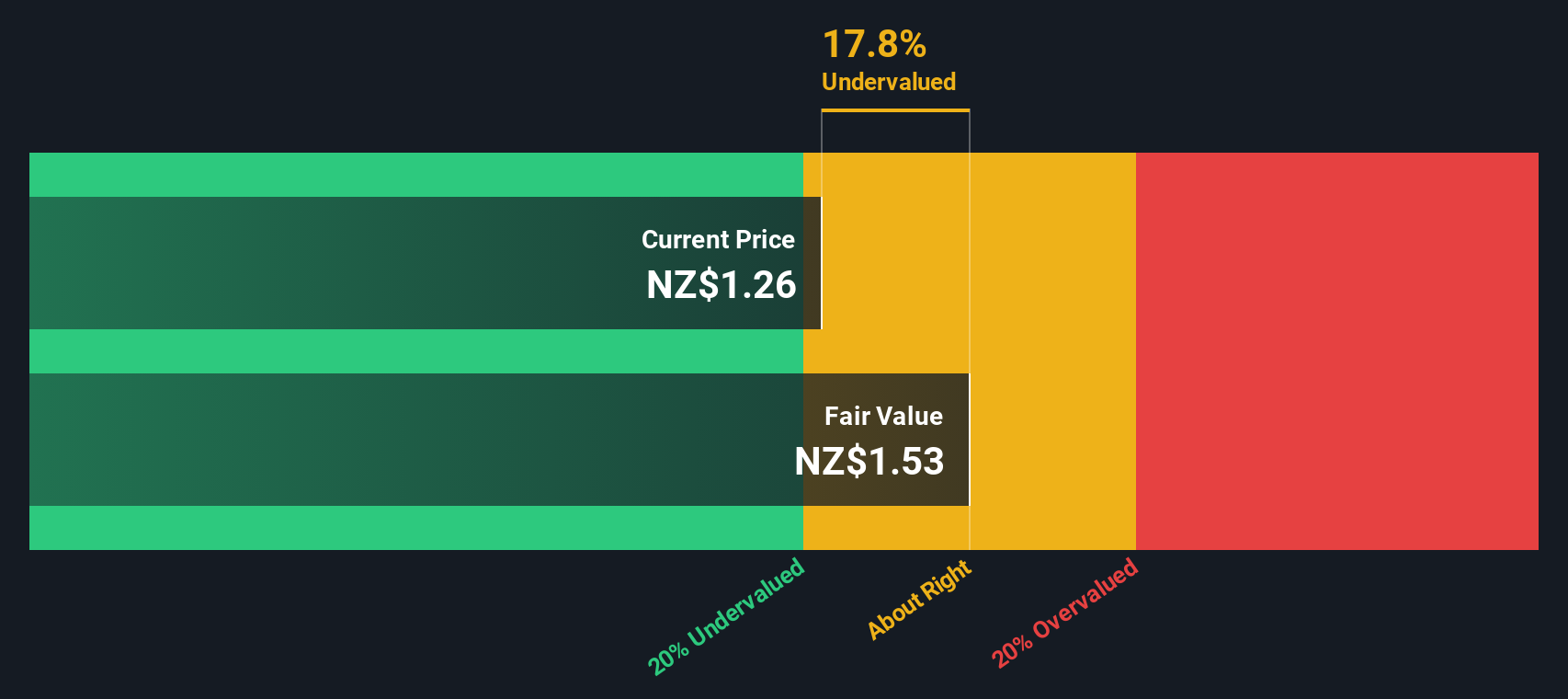

Precinct Properties NZ & Precinct Properties Investments (NZSE:PCT)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Precinct Properties NZ & Precinct Properties Investments is a New Zealand-based real estate company focused on investment properties, flexible space, hotel and hospitality sectors, with a market capitalization of approximately NZ$1.56 billion.

Operations: Precinct Properties generates its revenue primarily from Investment Properties, contributing NZ$215.60 million, followed by Flexible Space and Hotel and Hospitality segments. The company's gross profit margin has shown a decreasing trend over recent periods, dropping to 62.61% as of December 2024. Operating expenses have remained relatively stable in the range of NZ$20-22 million.

PE: -63.0x

Precinct Properties, a smaller player in the Asian market, recently reported half-year sales of NZ$134.4 million, up from NZ$121 million the previous year. However, net income dipped to NZ$9.2 million from NZ$15.3 million. Despite this decline, insider confidence is evident with recent share purchases by insiders indicating potential growth prospects. The company faces challenges with interest payments not fully covered by earnings and relies entirely on external borrowing for funding. Earnings are projected to grow significantly at 64.98% annually, suggesting future value potential amidst current undervaluation concerns.

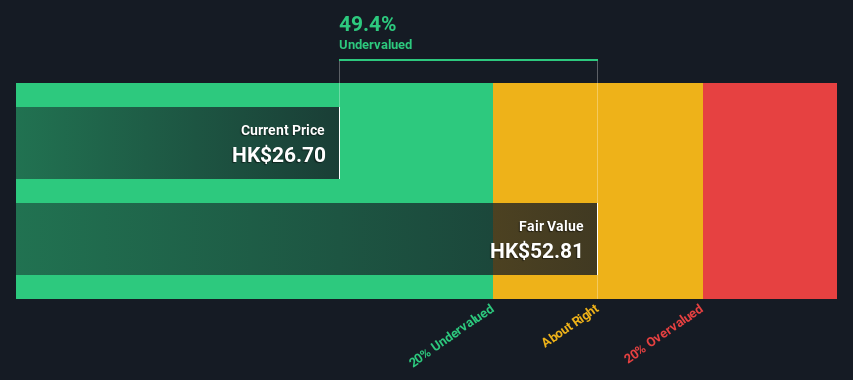

Shanghai Haohai Biological Technology (SEHK:6826)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shanghai Haohai Biological Technology is engaged in the production and sale of biologics, specifically focusing on medical hyaluronic acid, with a market capitalization of CN¥15.30 billion.

Operations: The company's revenue primarily comes from the production and sale of biologics, particularly medical hyaluronic acid. Over time, the gross profit margin has shown a declining trend, reaching 69.10% by September 2024. Operating expenses have been substantial, with sales and marketing being a significant component. The net income margin was recorded at 15.66% in September 2024.

PE: 14.1x

Shanghai Haohai Biological Technology, a smaller company in the Asian market, shows potential for growth with earnings projected to increase by 12% annually. Despite relying on higher-risk external borrowing for funding, insider confidence is evident as CFO Minjie Tang purchased 10,000 shares recently. The company reported modest sales growth to CNY 2.7 billion and net income of CNY 420 million for 2024. Although dividends decreased to RMB 0.6 per share, the firm completed a buyback of nearly half a million shares valued at CNY 30.58 million last year.

Next Steps

- Get an in-depth perspective on all 58 Undervalued Asian Small Caps With Insider Buying by using our screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6826

Shanghai Haohai Biological Technology

Shanghai Haohai Biological Technology Co., Ltd.

Undervalued with excellent balance sheet.

Market Insights

Community Narratives