SciClone Pharmaceuticals (Holdings)'s (HKG:6600) Upcoming Dividend Will Be Larger Than Last Year's

The board of SciClone Pharmaceuticals (Holdings) Limited (HKG:6600) has announced that it will be paying its dividend of CN¥0.39 on the 28th of June, an increased payment from last year's comparable dividend. This will take the annual payment to 3.6% of the stock price, which is above what most companies in the industry pay.

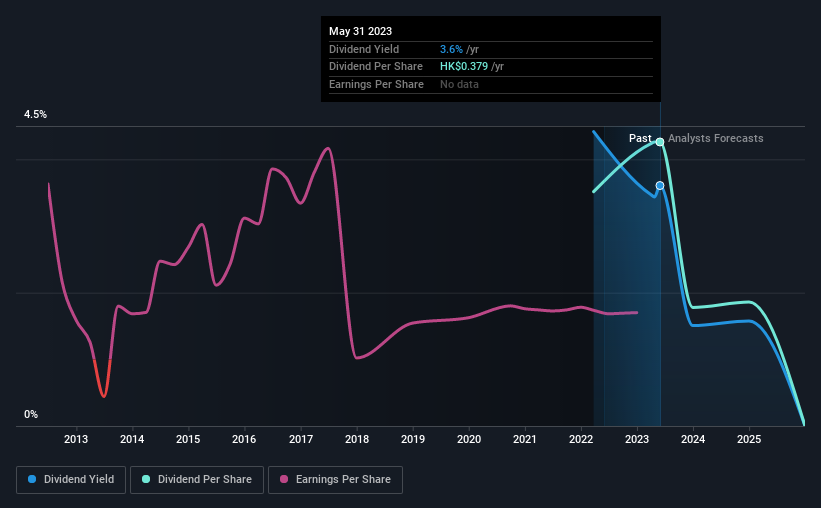

Check out our latest analysis for SciClone Pharmaceuticals (Holdings)

SciClone Pharmaceuticals (Holdings)'s Payment Has Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Before making this announcement, SciClone Pharmaceuticals (Holdings) was easily earning enough to cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

Over the next year, EPS is forecast to fall by 5.6%. Assuming the dividend continues along recent trends, we believe the payout ratio could be 29%, which we are pretty comfortable with and we think is feasible on an earnings basis.

SciClone Pharmaceuticals (Holdings) Doesn't Have A Long Payment History

The company hasn't been paying a dividend for very long at all, so we can't really make a judgement on how stable the dividend has been. This doesn't mean that the company can't pay a good dividend, but just that we want to wait until it can prove itself.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that SciClone Pharmaceuticals (Holdings) has been growing its earnings per share at 109% a year over the past five years. Earnings per share is growing at a solid clip, and the payout ratio is low which we think is an ideal combination in a dividend stock as the company can quite easily raise the dividend in the future.

We Really Like SciClone Pharmaceuticals (Holdings)'s Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The company is generating plenty of cash, and the earnings also quite easily cover the distributions. We should point out that the earnings are expected to fall over the next 12 months, which won't be a problem if this doesn't become a trend, but could cause some turbulence in the next year. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, SciClone Pharmaceuticals (Holdings) has 2 warning signs (and 1 which is a bit concerning) we think you should know about. Is SciClone Pharmaceuticals (Holdings) not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6600

SciClone Pharmaceuticals (Holdings)

A biopharmaceutical company, engages in the development and commercialization of pharmaceutical products in the therapeutic areas of oncology and severe infection in Mainland China and internationally.

Outstanding track record with flawless balance sheet.

Market Insights

Community Narratives