Advertisement

These 4 Measures Indicate That China Resources Pharmaceutical Group (HKG:3320) Is Using Debt Reasonably Well

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies China Resources Pharmaceutical Group Limited (HKG:3320) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for China Resources Pharmaceutical Group

How Much Debt Does China Resources Pharmaceutical Group Carry?

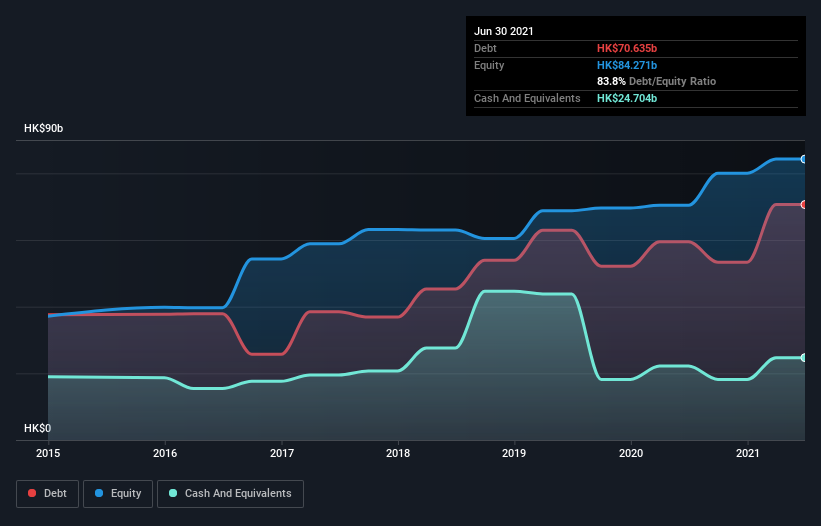

As you can see below, at the end of June 2021, China Resources Pharmaceutical Group had HK$70.6b of debt, up from HK$59.5b a year ago. Click the image for more detail. However, it also had HK$24.7b in cash, and so its net debt is HK$45.9b.

How Strong Is China Resources Pharmaceutical Group's Balance Sheet?

The latest balance sheet data shows that China Resources Pharmaceutical Group had liabilities of HK$140.5b due within a year, and liabilities of HK$9.22b falling due after that. On the other hand, it had cash of HK$24.7b and HK$106.7b worth of receivables due within a year. So it has liabilities totalling HK$18.3b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of HK$24.9b, so it does suggest shareholders should keep an eye on China Resources Pharmaceutical Group's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

China Resources Pharmaceutical Group has a debt to EBITDA ratio of 4.0 and its EBIT covered its interest expense 4.0 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. However, one redeeming factor is that China Resources Pharmaceutical Group grew its EBIT at 19% over the last 12 months, boosting its ability to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if China Resources Pharmaceutical Group can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, China Resources Pharmaceutical Group produced sturdy free cash flow equating to 79% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

On our analysis China Resources Pharmaceutical Group's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. But the other factors we noted above weren't so encouraging. For instance it seems like it has to struggle a bit handle its debt, based on its EBITDA,. When we consider all the elements mentioned above, it seems to us that China Resources Pharmaceutical Group is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with China Resources Pharmaceutical Group (at least 1 which doesn't sit too well with us) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:3320

China Resources Pharmaceutical Group

An investment holding company, engages in the research and development, manufacture, distribution, and retail of pharmaceutical and other healthcare products in Mainland China and internationally.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor