Is Biocytogen Pharmaceuticals (Beijing) (HKG:2315) A Risky Investment?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Biocytogen Pharmaceuticals (Beijing) Co., Ltd. (HKG:2315) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Biocytogen Pharmaceuticals (Beijing)

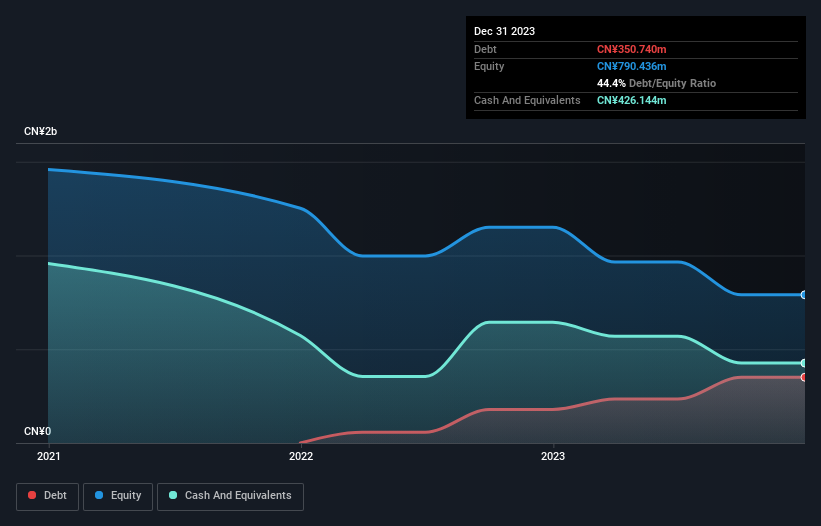

How Much Debt Does Biocytogen Pharmaceuticals (Beijing) Carry?

As you can see below, at the end of December 2023, Biocytogen Pharmaceuticals (Beijing) had CN¥350.7m of debt, up from CN¥178.8m a year ago. Click the image for more detail. But on the other hand it also has CN¥426.1m in cash, leading to a CN¥75.4m net cash position.

How Strong Is Biocytogen Pharmaceuticals (Beijing)'s Balance Sheet?

The latest balance sheet data shows that Biocytogen Pharmaceuticals (Beijing) had liabilities of CN¥577.6m due within a year, and liabilities of CN¥1.08b falling due after that. On the other hand, it had cash of CN¥426.1m and CN¥142.4m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥1.09b.

While this might seem like a lot, it is not so bad since Biocytogen Pharmaceuticals (Beijing) has a market capitalization of CN¥3.54b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. While it does have liabilities worth noting, Biocytogen Pharmaceuticals (Beijing) also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Biocytogen Pharmaceuticals (Beijing)'s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Biocytogen Pharmaceuticals (Beijing) wasn't profitable at an EBIT level, but managed to grow its revenue by 34%, to CN¥717m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Biocytogen Pharmaceuticals (Beijing)?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Biocytogen Pharmaceuticals (Beijing) lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of CN¥77m and booked a CN¥383m accounting loss. But the saving grace is the CN¥75.4m on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. With very solid revenue growth in the last year, Biocytogen Pharmaceuticals (Beijing) may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 1 warning sign we've spotted with Biocytogen Pharmaceuticals (Beijing) .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Biocytogen Pharmaceuticals (Beijing) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2315

Biocytogen Pharmaceuticals (Beijing)

A biotechnology company, engages in the research and development of antibody-based drugs in the People’s Republic of China, the United States, and internationally.

Acceptable track record with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives