- Canada

- /

- Oil and Gas

- /

- TSX:TOU

3 Stocks That Investors May Be Undervaluing By Up To 48.6%

Reviewed by Simply Wall St

Amidst recent fluctuations in global markets, driven by tariff uncertainties and mixed economic data, investors are seeking opportunities that might be overlooked. In this environment, identifying undervalued stocks can offer potential value as these equities may not fully reflect their intrinsic worth due to current market sentiments or broader economic concerns.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Shandong Bailong Chuangyuan Bio-Tech (SHSE:605016) | CN¥16.60 | CN¥33.16 | 49.9% |

| National World (LSE:NWOR) | £0.225 | £0.45 | 49.9% |

| World Fitness Services (TWSE:2762) | NT$89.80 | NT$178.27 | 49.6% |

| Geo Holdings (TSE:2681) | ¥1773.00 | ¥3508.29 | 49.5% |

| TCI (TPEX:8436) | NT$120.00 | NT$239.11 | 49.8% |

| Decisive Dividend (TSXV:DE) | CA$6.05 | CA$12.03 | 49.7% |

| Fine Foods & Pharmaceuticals N.T.M (BIT:FF) | €6.66 | €13.31 | 50% |

| Semiconductor Manufacturing International (SEHK:981) | HK$47.80 | HK$94.77 | 49.6% |

| Coastal Financial (NasdaqGS:CCB) | US$86.45 | US$172.68 | 49.9% |

| Believe (ENXTPA:BLV) | €14.48 | €28.83 | 49.8% |

Let's dive into some prime choices out of the screener.

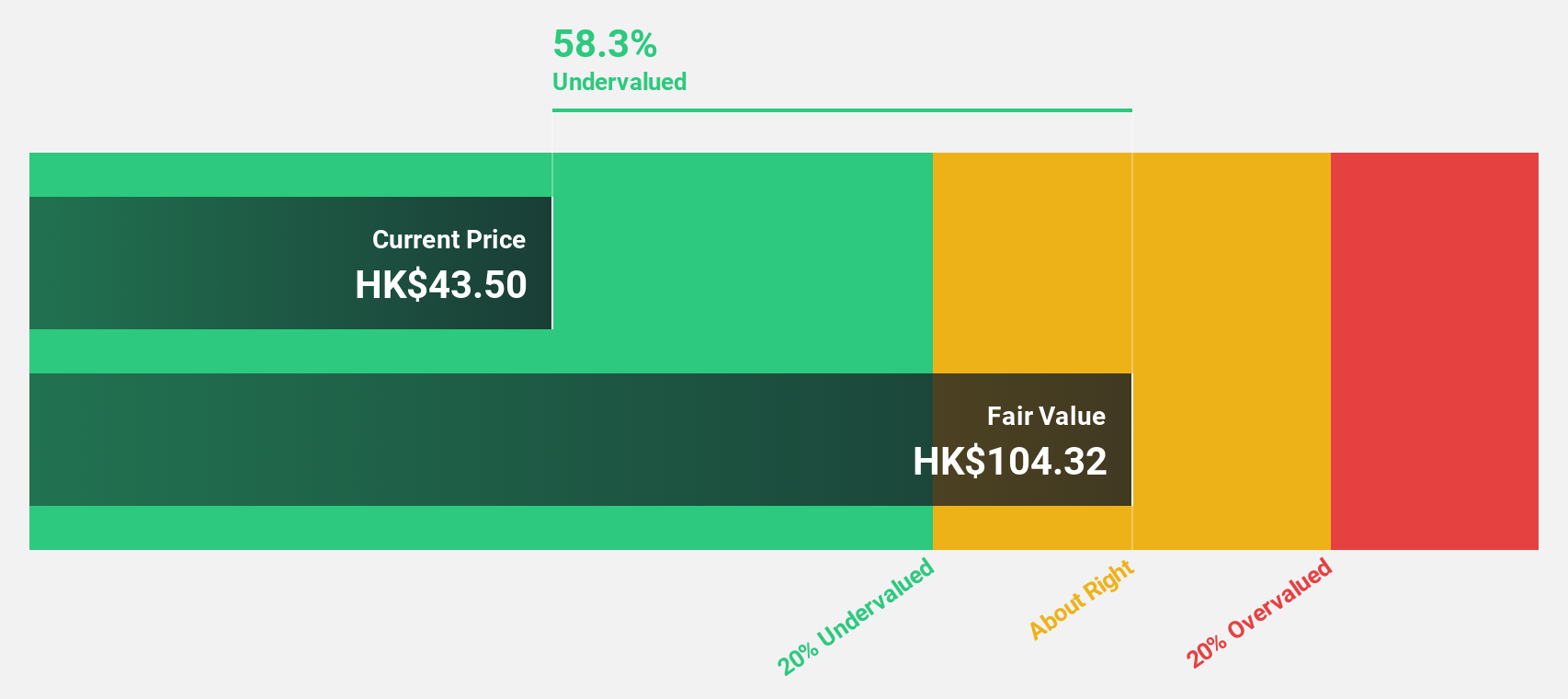

WuXi XDC Cayman (SEHK:2268)

Overview: WuXi XDC Cayman Inc. is an investment holding company that functions as a contract research, development, and manufacturing organization across China, North America, Europe, and other international markets with a market cap of HK$36.43 billion.

Operations: The company generates revenue from its Pharmaceuticals segment, amounting to CN¥2.80 billion.

Estimated Discount To Fair Value: 45.7%

WuXi XDC Cayman is trading at HK$30.4, significantly below its estimated fair value of HK$55.95, suggesting it is undervalued based on discounted cash flow analysis. The company's earnings are projected to grow 26.9% annually, outpacing the Hong Kong market's average growth rate of 11.5%. Recent guidance indicates substantial revenue and profit increases for 2024, with expected net profit growth exceeding last year's by a very large margin, enhancing its investment appeal despite low forecasted return on equity.

- The growth report we've compiled suggests that WuXi XDC Cayman's future prospects could be on the up.

- Click here to discover the nuances of WuXi XDC Cayman with our detailed financial health report.

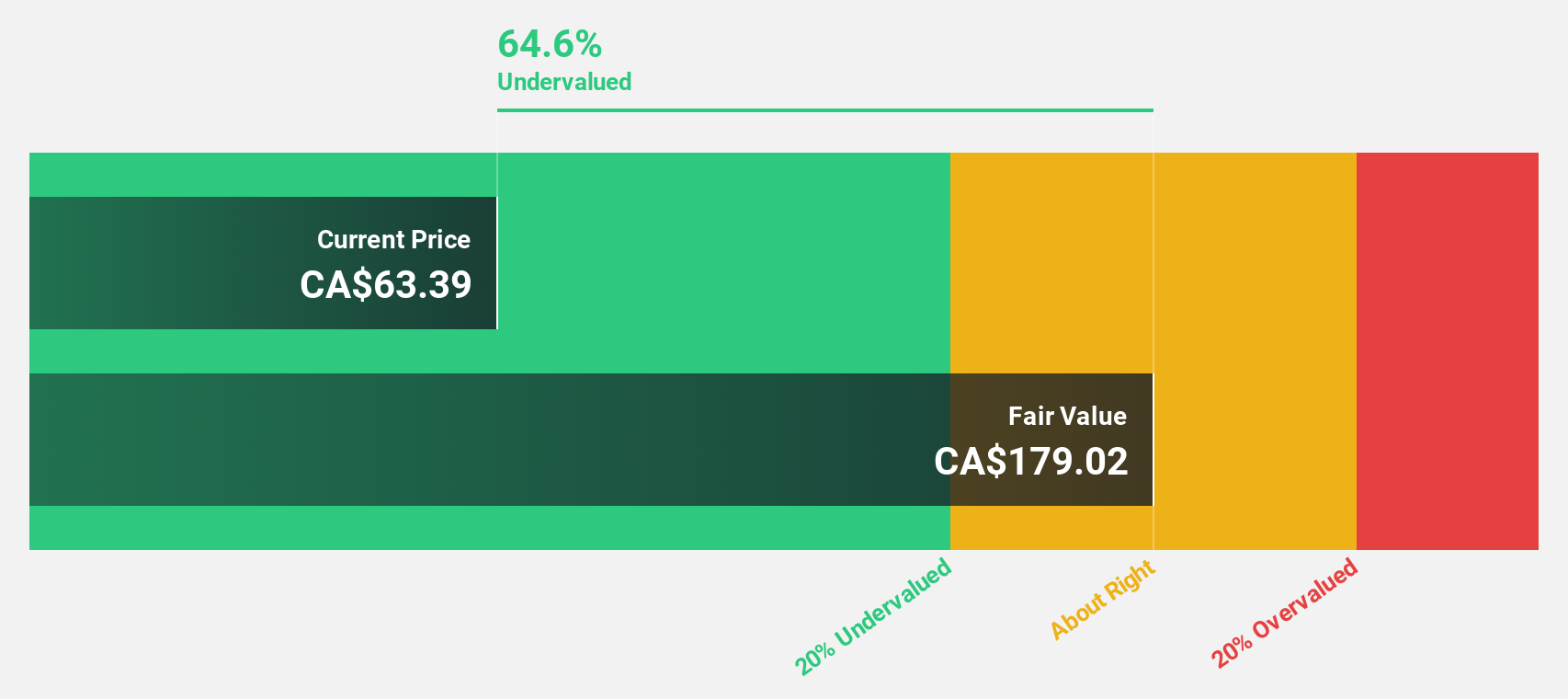

Tourmaline Oil (TSX:TOU)

Overview: Tourmaline Oil Corp. is engaged in the exploration and development of oil and natural gas properties in the Western Canadian Sedimentary Basin, with a market cap of CA$25.15 billion.

Operations: The company's revenue from petroleum and natural gas properties amounts to CA$4.48 billion.

Estimated Discount To Fair Value: 48.6%

Tourmaline Oil, trading at CA$69.25, is significantly undervalued with an estimated fair value of CA$134.84 based on discounted cash flow analysis. Earnings are projected to grow 30.58% annually, surpassing the Canadian market's growth rate of 17.8%. Despite this growth potential and revenue forecast exceeding 20% per year, the dividend yield of 5.63% isn't well covered by free cash flows, and return on equity is expected to remain low at 15.2%.

- Our growth report here indicates Tourmaline Oil may be poised for an improving outlook.

- Get an in-depth perspective on Tourmaline Oil's balance sheet by reading our health report here.

adidas (XTRA:ADS)

Overview: adidas AG, along with its subsidiaries, is engaged in the design, development, production, and marketing of athletic and sports lifestyle products across various regions including Europe, the Middle East, Africa, North America, Greater China, the Asia-Pacific, and Latin America; it has a market cap of approximately €45.94 billion.

Operations: The company's revenue segments, in millions of €, include Greater China (€3.34 billion), Latin America (€2.44 billion), and North America (€4.95 billion).

Estimated Discount To Fair Value: 34.8%

adidas, trading at €257.3, is undervalued by over 20% compared to its estimated fair value of €394.67 based on discounted cash flow analysis. The company recently became profitable and is expected to see earnings grow significantly at 32.3% annually, outpacing the German market's growth rate of 19.3%. While revenue growth is forecasted at a slower pace of 8.3% per year, it still exceeds the German market average of 5.7%.

- In light of our recent growth report, it seems possible that adidas' financial performance will exceed current levels.

- Navigate through the intricacies of adidas with our comprehensive financial health report here.

Next Steps

- Access the full spectrum of 894 Undervalued Stocks Based On Cash Flows by clicking on this link.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tourmaline Oil might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TOU

Tourmaline Oil

Explores for and develops oil and natural gas properties in the Western Canadian Sedimentary Basin.

High growth potential with solid track record.

Market Insights

Community Narratives