- Italy

- /

- Diversified Financial

- /

- BIT:BFF

Undervalued Small Caps With Insider Buying Across Regions In January 2025

Reviewed by Simply Wall St

As global markets continue to react to the Trump administration's emerging policies, major indices like the S&P 500 and Russell 2000 have shown robust performance, with large-cap stocks generally outpacing their smaller counterparts. Despite this trend, small-cap stocks remain an area of interest for investors seeking opportunities potentially overlooked by broader market movements. Identifying promising small-cap stocks often involves looking at factors such as insider buying and valuation metrics, especially in a dynamic economic landscape shaped by geopolitical developments and evolving trade policies.

Top 10 Undervalued Small Caps With Insider Buying

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 21.4x | 5.4x | 27.22% | ★★★★★★ |

| Speedy Hire | NA | 0.3x | 36.19% | ★★★★★☆ |

| Gamma Communications | 22.6x | 2.3x | 38.15% | ★★★★☆☆ |

| Paradeep Phosphates | 25.2x | 0.8x | 25.89% | ★★★★☆☆ |

| ABG Sundal Collier Holding | 12.6x | 2.1x | 39.51% | ★★★★☆☆ |

| Logistri Fastighets | 12.7x | 9.0x | 39.99% | ★★★★☆☆ |

| CVS Group | 27.0x | 1.1x | 45.89% | ★★★★☆☆ |

| Mark Dynamics Indonesia | 12.8x | 4.2x | 8.20% | ★★★☆☆☆ |

| Yixin Group | 7.2x | 0.7x | -2615.10% | ★★★☆☆☆ |

| Digital Mediatama Maxima | NA | 1.3x | 13.99% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

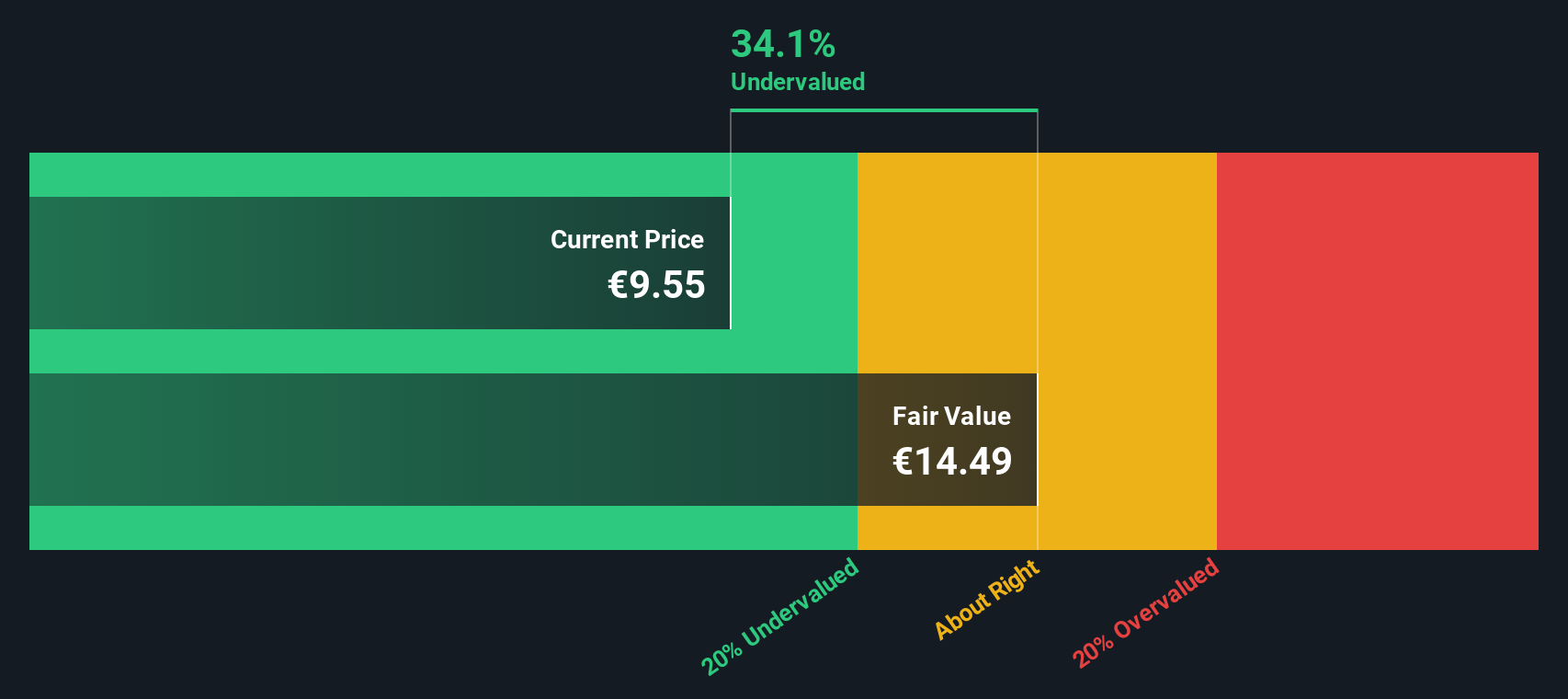

BFF Bank (BIT:BFF)

Simply Wall St Value Rating: ★★★★★☆

Overview: BFF Bank provides financial services primarily in the commercial sector, with a market capitalization of €1.23 billion.

Operations: BFF Bank's revenue primarily stems from its financial services, with commercial operations generating significant income. The company's gross profit margin has varied, notably reaching 92.19% in the most recent period. Operating expenses have shown fluctuations, sometimes reflecting negative values due to adjustments or reversals in accounting entries.

PE: 6.2x

BFF Bank, a small-cap stock, shows insider confidence with recent share purchases. The bank's reliance on external borrowing highlights a higher-risk funding structure, yet earnings are expected to grow by 3.83% annually. For the nine months ending September 2024, BFF reported a net income of €189.9 million, reflecting solid financial performance despite its unique funding challenges. These factors suggest potential for future growth in this niche segment of the market.

- Click to explore a detailed breakdown of our findings in BFF Bank's valuation report.

Assess BFF Bank's past performance with our detailed historical performance reports.

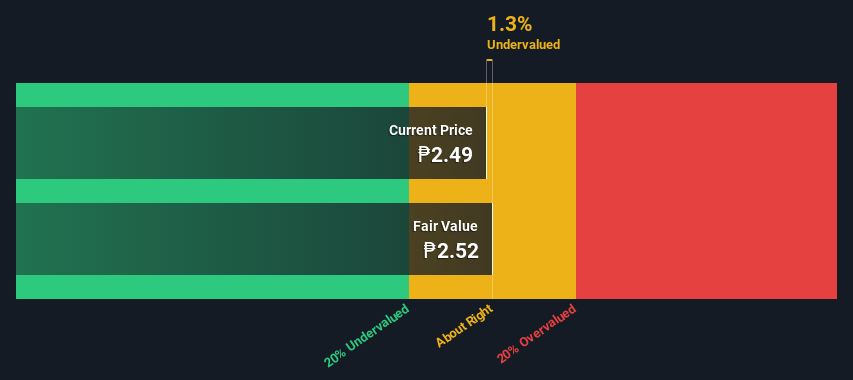

Nickel Asia (PSE:NIKL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Nickel Asia is a diversified company primarily engaged in mining operations, with additional interests in power generation and services, and has a market capitalization of approximately ₱1.11 billion.

Operations: Nickel Asia's revenue is primarily driven by its mining operations, with significant contributions from TMC and RTN segments. The company has experienced fluctuations in its net income margin, peaking at 32.88% in June 2022 before declining to 12.29% by September 2024. Operating expenses have varied over time, impacting overall profitability alongside non-operating expenses and cost of goods sold (COGS).

PE: 11.4x

Nickel Asia, a smaller player in its sector, is drawing attention for potential value due to recent insider confidence. Rolando Cruz acquired 100,000 shares recently, signaling belief in the company's prospects. However, financials show challenges; third-quarter revenue dropped to PHP 7.69 billion from PHP 8.36 billion year-over-year, and net income fell to PHP 1.44 billion from PHP 1.90 billion. Ongoing talks with Sumitomo for selling its stake in Coral Bay Nickel Corp could reshape its strategic direction and financial position moving forward.

- Delve into the full analysis valuation report here for a deeper understanding of Nickel Asia.

Evaluate Nickel Asia's historical performance by accessing our past performance report.

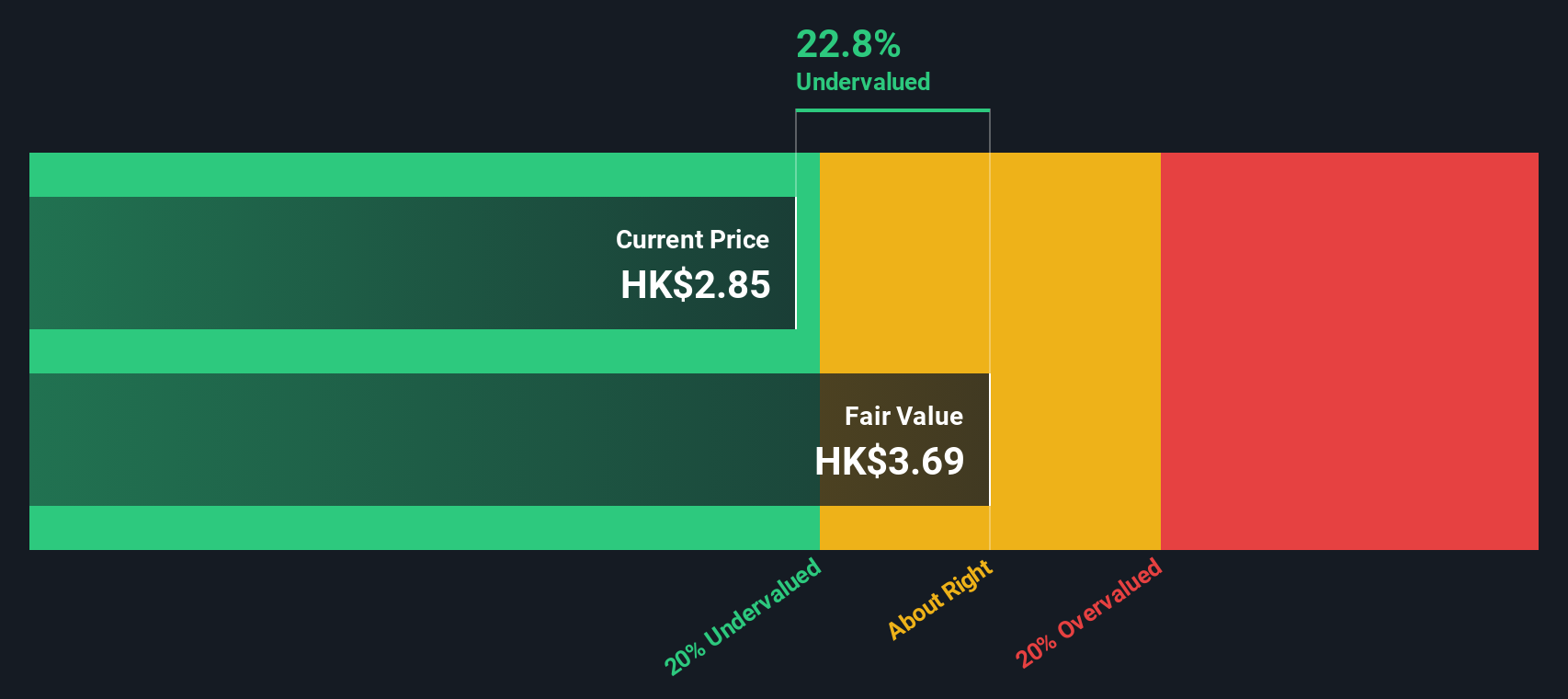

SSY Group (SEHK:2005)

Simply Wall St Value Rating: ★★★★☆☆

Overview: SSY Group is a company engaged in the production and sale of medical materials and intravenous infusion solutions, with a market capitalization of HK$7.5 billion.

Operations: The primary revenue stream comes from Intravenous Infusion Solution and Others, with a smaller contribution from Medical Materials. The gross profit margin has shown variability, most recently recorded at 54.39% as of June 30, 2024. Operating expenses include significant allocations to sales and marketing, followed by general and administrative costs.

PE: 6.8x

SSY Group, a smaller company in the pharmaceutical industry, has recently gained attention for its potential growth. The firm secured multiple drug approvals from China's National Medical Products Administration, including Composite Potassium Hydrogen Phosphate Injection and Vortioxetine Hydrobromide Tablets. This positions them well in the market for treating conditions like hypophosphatemia and depression. Notably, insider confidence is evident as their Chairman & CEO acquired 1.5 million shares worth approximately HK$7.5 million, reflecting belief in future prospects despite reliance on external borrowing for funding.

Key Takeaways

- Access the full spectrum of 185 Undervalued Small Caps With Insider Buying by clicking on this link.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BFF Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:BFF

BFF Bank

Engages in non-recourse factoring and credit management activities towards public administration bodies and private hospitals in Italy, Croatia, the Czech Republic, France, Greece, Poland, Portugal, Slovakia, and Spain.

Undervalued with excellent balance sheet.

Market Insights

Community Narratives